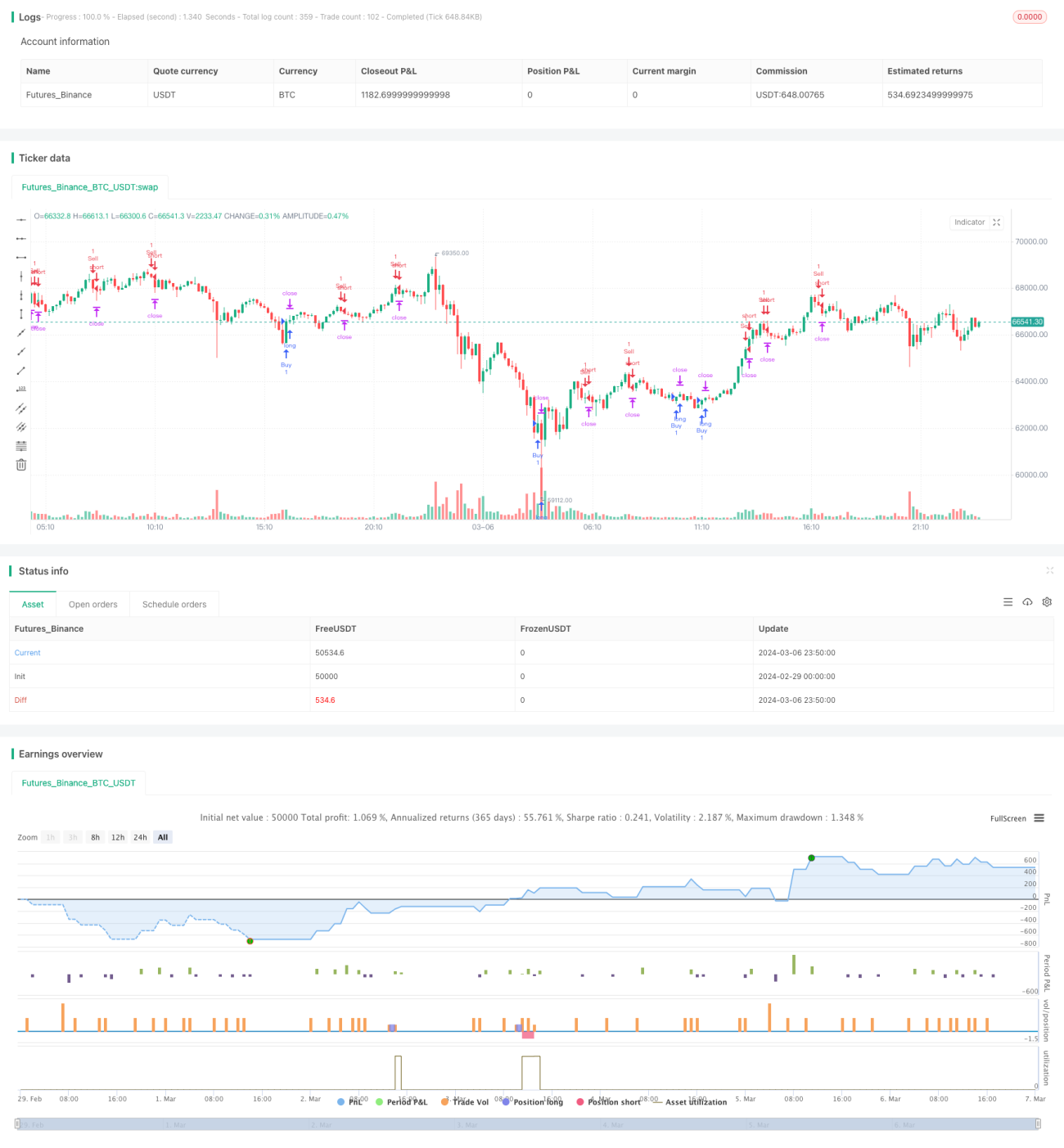

ランダム指標(ストキャスティクス)のクロスに基づく双方向の利確・損切り戦略

1

Follow

1802

Followers

概要

本戦略は、ストキャスティクス・オシレーター(Stochastic Oscillator)のクロスシグナルを利用して、売買のトリガーを発生させます。%Kラインが下から上へ%Dラインをクロスし、かつ%K値が20未満の場合に買いポジションをオープンします。%Kラインが上から下へ%Dラインをクロスし、かつ%K値が80を超える場合に売りポジションをオープンします。同時に、利確(テイクプロフィット)および損切り(ストップロス)の距離を設定してポジションを管理し、損失の拡大を防ぎます。また、ストキャスティクスがオープンシグナルと逆のクロスシグナルを発生した場合、利確・損切りの価格に達していなくても、対応する買いまたは売りのポジションを決済する論理条件も設定されています。

戦略の原理

- 14期間のストキャスティクス%K値と%D値を計算し、単純移動平均を用いて平滑化します。

- %Kラインと%Dラインのクロスを判定します。

- %Kラインが下から上へ%Dラインをクロスし、かつ%K値が20未満の場合、買いシグナルが発生し、買いポジションをオープンします。

- %Kラインが上から下へ%Dラインをクロスし、かつ%K値が80を超える場合、売りシグナルが発生し、売りポジションをオープンします。

- 利確距離と損切り距離(Ticks単位)を設定し、オープンポジションを管理します。

- 買いポジションの場合、利確価格はオープン価格の上方TP Ticks、損切り価格はオープン価格の下方SL Ticksに設定します。

- 売りポジションの場合、利確価格はオープン価格の下方TP Ticks、損切り価格はオープン価格の上方SL Ticksに設定します。

- 価格が利確または損切りの価格に達した場合、該当ポジションを決済します。

- 論理条件による決済を設定します。

- %Kラインが上から下へ%Dラインをクロスし、かつ%K値が80以下の場合、すべての買いポジションを決済します。

- %Kラインが下から上へ%Dラインをクロスし、かつ%K値が20以上の場合、すべての売りポジションを決済します。

優位性分析

- 本戦略はストキャスティクスを主な取引シグナル指標として使用しています。ストキャスティクスは定量取引で広く利用されており、市場の買われすぎ・売られすぎの状態を適切に捉えることができます。

- 戦略は利確・損切りと論理条件による決済を同時に設定しており、リスクをある程度コントロールし、損失の拡大を防ぎます。

- 戦略のロジックは明確で理解しやすく、実装も容易であり、初心者が学び、使用するのに適しています。

リスク分析

- ストキャスティクスはレンジ相場で多くの誤ったシグナルを発する可能性があり、取引頻度が高くなり、取引コストが増加します。

- 本戦略はポジションの動的調整を行っていないため、市場が激しく変動する場合、固定の利確・損切り距離ではリスクを効果的にコントロールできない可能性があります。

- 戦略のパラメータ(ストキャスティクスの期間、利確・損切り距離など)は固定されており、異なる市場状況に最適化されていないため、戦略の適応性に影響を与える可能性があります。

最適化の方向性

- 他のテクニカル指標や市場センチメント指標を導入し、ストキャスティクスと組み合わせて使用することで、取引シグナルの信頼性を高め、誤ったシグナルを減らすことを検討できます。

- ポジション管理を最適化し、市場のボラティリティに応じて利確・損切り距離を動的に調整するか、ケリーの公式などのより高度な資金管理手法を採用します。

- 遺伝的アルゴリズムやグリッドサーチなどの最適化手法を使用して、戦略パラメータを最適化し、さまざまな市場状況に適応する最適なパラメータの組み合わせを見つけます。

- 取引時間帯や取引銘柄のボラティリティなどのフィルター条件を追加し、不利な市場環境での取引を減らすことを検討します。

まとめ

ストキャスティクスのクロスに基づく双方向利確・損切り戦略は、シンプルで理解しやすい定量取引戦略です。ストキャスティクスのクロスシグナルで売買をトリガーし、利確・損切りおよび論理条件による決済でリスクを管理します。本戦略の優位性はロジックが明確で、初心者が学び使用するのに適している点です。しかし、ストキャスティクスがレンジ相場で多くの誤ったシグナルを発する可能性がある、固定のポジション管理方法が異なる市場状況に適応できないなど、いくつかのリスクも存在します。戦略のパフォーマンスをさらに向上させるためには、他の指標の導入、ポジション管理の最適化、パラメータの最適化、フィルター条件の追加などの改善を検討できます。全体として、本戦略は基本的な定量取引戦略のテンプレートとして利用でき、継続的な最適化と改善により、実戦で良好な結果を期待できます。

Source

Pine

/*backtest

start: 2024-02-29 00:00:00

end: 2024-03-07 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("How to force strategies fire exit alerts not reversals", initial_capital = 1000, slippage=1, commission_type = strategy.commission.cash_per_contract, commission_value = 0.0001, overlay=true)

// disclaimer: this content is purely educational, especially please don't pay attention to backtest results on any timeframe/ticker

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1