TrippleMACD移動平均線クロスと相対力指数を組み合わせた高頻度仮想通貨取引戦略

概要

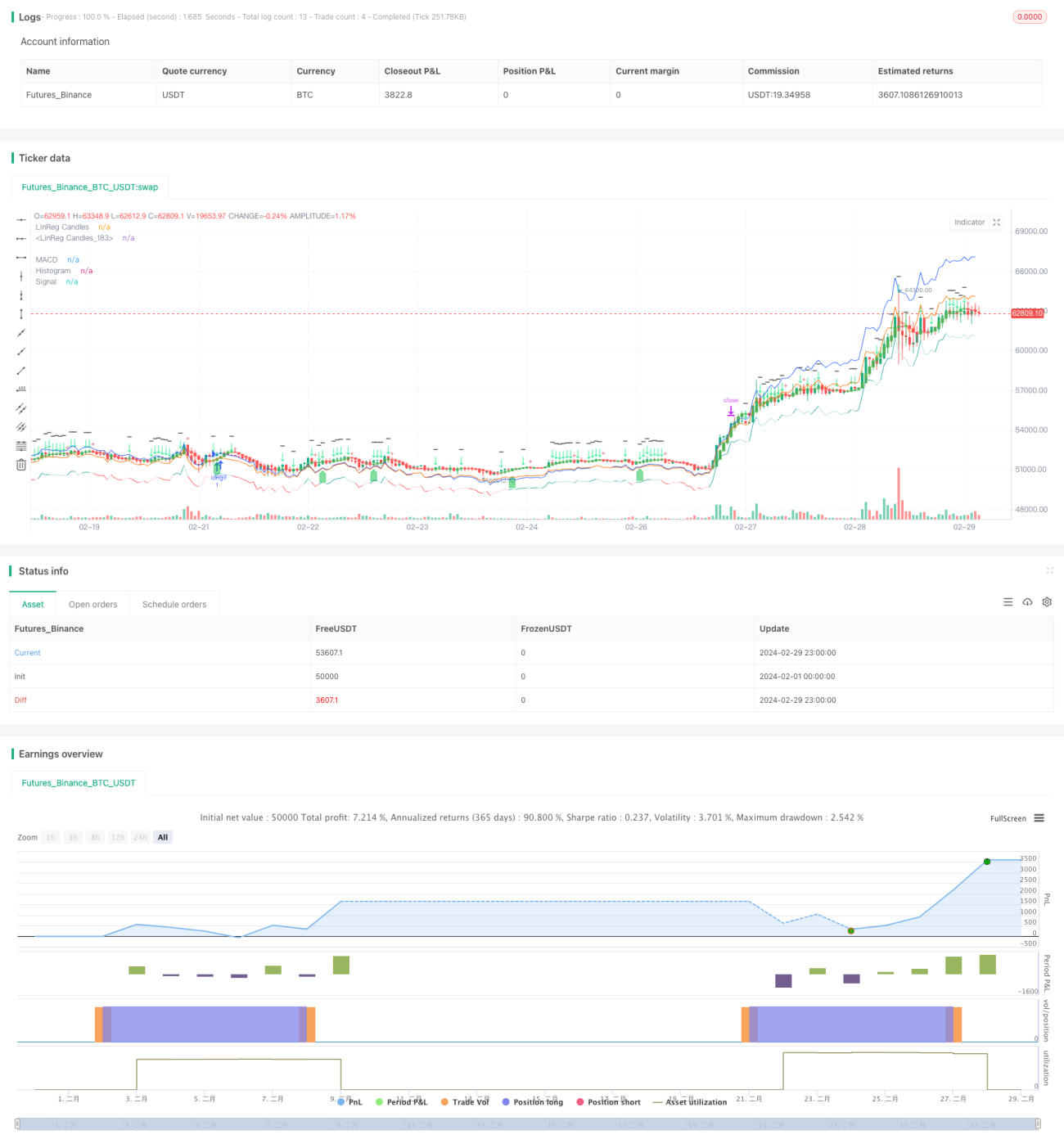

本稿では、TrippleMACD移動平均線クロスオーバーと相対力指数(RSI)を組み合わせた高頻度暗号通貨取引戦略について説明します。この戦略は、3組の異なるパラメータを持つMACDインジケーターを使用し、それらのシグナル線を平均化するとともに、RSIインジケーターを組み合わせて最適な買いと売りのタイミングを決定します。この戦略は1分足の時間枠での自動取引向けに設計されており、ロング取引のみを考慮します。また、線形回帰を利用して市場のレンジ相場を識別し、揉み合い相場での取引を回避します。

戦略の原理

この戦略の核心は、3組の異なるパラメータを持つMACDインジケーターを使用して、異なる時間スケールでのトレンドシグナルを捉えることです。これら3組のMACDインジケーターのシグナル線を平均化することで、ノイズを効果的に平滑化し、より信頼性の高い取引シグナルを提供できます。同時に、RSIインジケーターはロングトレンドの強さを確認するために使用されます。すべての3組のMACDインジケーターがロングシグナルを示し、かつRSIインジケーターもロングトレンドの強さを確認した場合のみ、この戦略は買いシグナルを発します。

さらに、この戦略は線形回帰を利用して市場のレンジ相場を識別します。ローソク足の上ヒゲと下ヒゲと実体の比率を計算することで、現在の市場がレンジ相場にあるかどうかを判断します。上ヒゲと下ヒゲの長さが実体の長さの2倍以上の場合、市場はレンジ相場にあるとみなし、この戦略は取引を回避します。

優位性の分析

-

複数時間スケール分析:3組の異なるパラメータを持つMACDインジケーターを使用することで、異なる時間スケールでのトレンドシグナルを捉えることができ、取引の正確性と信頼性が向上します。

-

シグナルの平滑化:3組のMACDインジケーターのシグナル線を平均化することで、ノイズを効果的に平滑化し、単一のインジケーターが生じる可能性のある誤ったシグナルを回避します。

-

トレンド確認:RSIインジケーターを組み合わせてロングトレンドの強さを確認することで、取引シグナルの信頼性をさらに高めます。

-

レンジ相場の識別:線形回帰を利用して市場のレンジ相場を識別することで、揉み合い相場での取引を回避し、戦略のリスクを低減します。

-

自動取引:この戦略は1分足の時間枠での自動取引向けに設計されており、市場の変化に迅速に対応して取引を実行できるため、取引効率が向上します。

リスク分析

-

パラメータ最適化:この戦略は複数のパラメータ(3組のMACDインジケーターの短期・長期移動平均周期、RSIインジケーターの周期など)に関わります。これらのパラメータの選択は戦略のパフォーマンスに大きな影響を与え、最適化が不十分な場合、戦略の性能が低下する可能性があります。

-

過学習リスク:この戦略は特定の過去データでは良好に機能するかもしれませんが、実際の運用では市場の変化に適応できず、戦略が機能しなくなる可能性があります。

-

ブラックスワンイベント:この戦略は主にテクニカル指標に基づいており、重大なファンダメンタルズイベントに対して反応が不十分な場合があり、極端な市場環境ではパフォーマンスが低下する可能性があります。

最適化の方向性

-

動的パラメータ調整:市場状況の変化に応じて、戦略内の各パラメータ(MACDインジケーターの短期・長期移動平均周期、RSIインジケーターの周期など)を動的に調整し、異なる市場環境に適応させます。

-

追加のインジケーター導入:既存のMACDとRSIに加えて、ボリンジャーバンドや移動平均線などの他のテクニカル指標を追加し、取引シグナルの正確性と信頼性をさらに向上させることを検討します。

-

リスク管理の最適化:動的ストップロスやポジション管理など、より完全なリスク管理手法を戦略に組み込み、戦略全体のリスクを低減します。

-

機械学習による最適化:ニューラルネットワークやサポートベクターマシンなどの機械学習アルゴリズムを利用して、戦略のパラメータと取引ルールを最適化し、戦略の適応性とロバスト性を向上させます。

まとめ

本稿では、TrippleMACD移動平均線クロスオーバーとRSIインジケーターを組み合わせた高頻度暗号通貨取引戦略について説明しました。この戦略は、3組の異なるパラメータを持つMACDインジケーターとRSIインジケーターを使用して信頼性の高い取引シグナルを生成し、同時に線形回帰を利用して市場のレンジ相場を識別し、揉み合い相場での取引を回避します。この戦略の優位性は、複数時間スケール分析、シグナルの平滑化、トレンド確認、レンジ相場の識別、自動取引などにありますが、パラメータ最適化、過学習、ブラックスワンイベントなどのリスクも存在します。将来は、動的パラメータ調整、追加のインジケーター導入、リスク管理の最適化、機械学習による最適化などを通じてこの戦略を改善し、その適応性とロバスト性を高め、暗号通貨市場の変化により良く対応することができます。

/*backtest

start: 2024-02-01 00:00:00

end: 2024-02-29 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//indicator("Triplle",shorttitle="Triplle MACD", overlay=true, scale = scale.none)

//indicator("Triplle","TrippleMACD",true)

strategy(title="TrippleMACD", shorttitle="TrippleMACD + RSI strategy", format=format.price, precision=4, overlay=true)- 1