확률적 지표 교차 기반 양방향 이익실현 및 손절매 전략

개요

해당 전략은 스토캐스틱 오실레이터(Stochastic Oscillator)의 교차 신호를 활용하여 매수 및 매도 작업을 트리거합니다. 스토캐스틱 지표에서 %K 라인이 아래에서 위로 %D 라인을 교차하고 %K 값이 20 미만일 때 매수 포지션을 오픈합니다. %K 라인이 위에서 아래로 %D 라인을 교차하고 %K 값이 80 초과일 때 매도 포지션을 오픈합니다. 동시에 전략은 이익 실현(Take Profit) 및 손절매(Stop Loss) 거리를 설정하여 포지션을 관리하고 손실 확대를 방지합니다. 또한 해당 전략은 스토캐스틱 지표에서 오픈 신호와 반대되는 교차 신호가 발생할 경우, 이익 실현 또는 손절매 가격에 도달하지 않았더라도 해당 롱 또는 숏 포지션을 청산하는 논리 조건을 설정합니다.

전략 원리

- 14주기 스토캐스틱 지표의 %K 값과 %D 값을 계산하고, 단순 이동 평균을 사용하여 평활화합니다.

- %K 라인과 %D 라인의 교차 여부를 판단합니다.

- %K 라인이 아래에서 위로 %D 라인을 교차하고 %K 값이 20 미만일 때 매수 신호가 발생하여 롱 포지션을 오픈합니다.

- %K 라인이 위에서 아래로 %D 라인을 교차하고 %K 값이 80 초과일 때 매도 신호가 발생하여 숏 포지션을 오픈합니다.

- 이익 실현 및 손절매 거리(Ticks 단위)를 설정하여 오픈된 포지션을 관리합니다.

- 롱 포지션의 경우, 이익 실현 가격은 오픈 가격보다 TP만큼 위에, 손절매 가격은 오픈 가격보다 SL만큼 아래에 설정됩니다.

- 숏 포지션의 경우, 이익 실현 가격은 오픈 가격보다 TP만큼 아래에, 손절매 가격은 오픈 가격보다 SL만큼 위에 설정됩니다.

- 가격이 이익 실현 또는 손절매 가격에 도달하면 해당 포지션을 청산합니다.

- 논리 조건에 의한 포지션 청산을 설정합니다.

- %K 라인이 위에서 아래로 %D 라인을 교차하고 %K 값이 80 이하일 때 모든 롱 포지션을 청산합니다.

- %K 라인이 아래에서 위로 %D 라인을 교차하고 %K 값이 20 이상일 때 모든 숏 포지션을 청산합니다.

장점 분석

- 해당 전략은 주요 거래 신호 지표로 스토캐스틱 오실레이터를 사용합니다. 스토캐스틱 오실레이터는 퀀트 트레이딩에서 널리 사용되며, 시장의 과매수/과매도 상태를 효과적으로 포착할 수 있습니다.

- 전략은 이익 실현 및 손절매와 논리 조건에 의한 포지션 청산을 동시에 설정하여, 일정 수준에서 리스크를 통제하고 손실 확대를 방지할 수 있습니다.

- 전략의 논리가 명확하고 이해 및 구현이 쉬워 초보자가 학습하고 사용하기에 적합합니다.

리스크 분석

- 스토캐스틱 오실레이터는 횡보장에서 많은 오류 신호를 발생시킬 수 있어 거래 빈도가 지나치게 높아지고 거래 비용이 증가할 수 있습니다.

- 해당 전략은 포지션을 동적으로 조정하지 않으므로, 시장이 급변할 때 고정된 이익 실현 및 손절매 거리가 리스크를 효과적으로 제어하지 못할 수 있습니다.

- 전략 내 파라미터(예: 스토캐스틱 주기, 이익 실현/손절매 거리 등)가 고정되어 있어 다양한 시장 상황에 최적화되지 않았으며, 이는 전략의 적응성에 영향을 미칠 수 있습니다.

최적화 방향

- 다른 기술적 지표나 시장 심리 지표를 도입하여 스토캐스틱 오실레이터와 함께 사용함으로써 거래 신호의 신뢰도를 높이고 오류 신호를 줄일 수 있습니다.

- 포지션 관리를 최적화하여 시장 변동성에 따라 이익 실현 및 손절매 거리를 동적으로 조정하거나, 켈리 공식과 같은 고급 자금 관리 방법을 도입할 수 있습니다.

- 유전 알고리즘, 그리드 서치 등의 최적화 방법을 사용하여 전략 파라미터를 최적화하고 다양한 시장 상황에 적응하는 최적의 파라미터 조합을 찾을 수 있습니다.

- 거래 시간대, 거래 종목의 변동성 등의 필터 조건을 추가하여 불리한 시장 환경에서의 거래를 줄이는 것을 고려할 수 있습니다.

요약

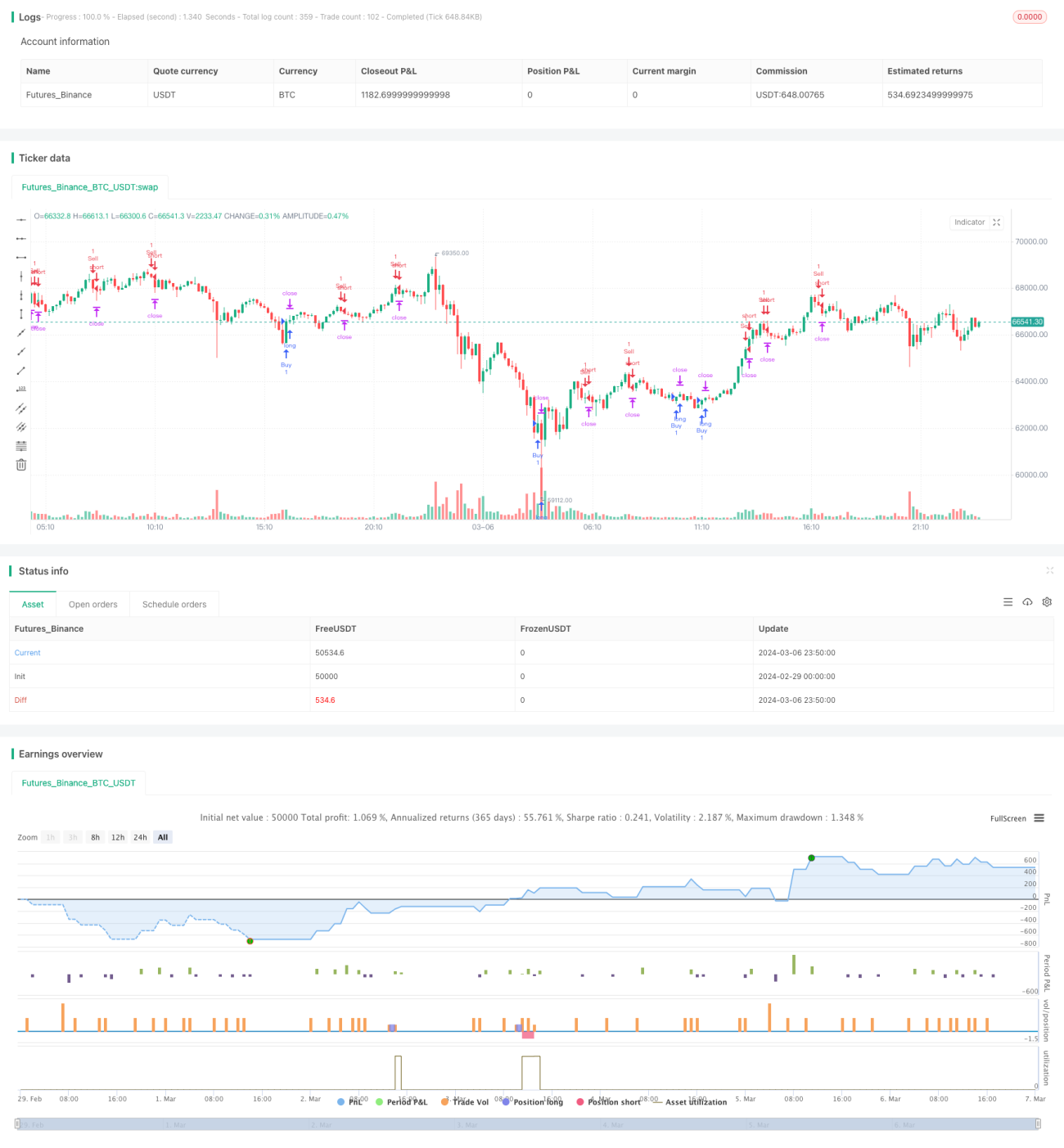

스토캐스틱 오실레이터 교차 기반 양방향 이익 실현 및 손절매 전략은 이해하기 쉬운 퀀트 트레이딩 전략입니다. 스토캐스틱 오실레이터의 교차 신호를 활용하여 매수 및 매도 작업을 트리거하고, 이익 실현 및 손절매와 논리 조건에 의한 포지션 청산을 설정하여 리스크를 관리합니다. 이 전략은 논리가 명확하여 초보자가 학습하고 사용하기에 적합하다는 장점이 있습니다. 그러나 스토캐스틱 오실레이터가 횡보장에서 많은 오류 신호를 발생시킬 수 있고, 고정된 포지션 관리 방식이 다양한 시장 상황에 적응하지 못할 수 있는 등의 리스크도 존재합니다. 전략의 성과를 더욱 향상시키기 위해서는 다른 지표 도입, 포지션 관리 최적화, 파라미터 최적화 및 필터 조건 추가 등의 개선을 고려할 수 있습니다. 전반적으로 이 전략은 기본적인 퀀트 트레이딩 전략 템플릿으로 활용될 수 있으며, 지속적인 최적화와 개선을 통해 실제 거래에서 좋은 성과를 거둘 수 있을 것으로 기대됩니다.

/*backtest

start: 2024-02-29 00:00:00

end: 2024-03-07 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("How to force strategies fire exit alerts not reversals", initial_capital = 1000, slippage=1, commission_type = strategy.commission.cash_per_contract, commission_value = 0.0001, overlay=true)

// disclaimer: this content is purely educational, especially please don't pay attention to backtest results on any timeframe/ticker

- 1