Estratégia de busca por momentum

Visão Geral

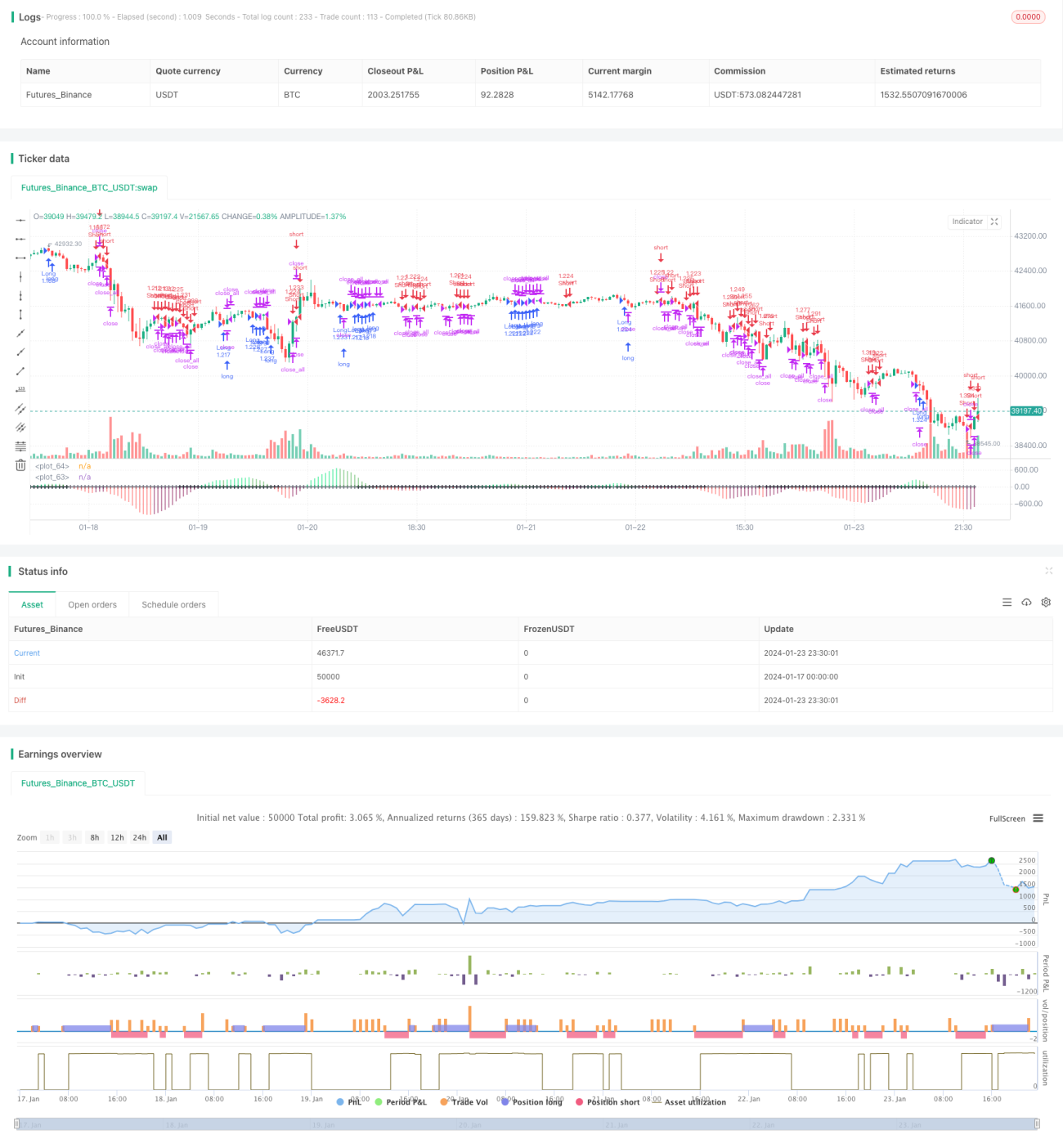

Esta estratégia determina a compressão e liberação do mercado através de múltiplos indicadores, como Bandas de Bollinger, Canal de Keltner e cor dos candles, combinando com a direção da média para julgar a tendência establishment, realizando operações quando a direção da tendência se inverte.

Princípio da Estratégia

-

Calcular as Bandas de Bollinger. A banda média das Bandas de Bollinger é a média móvel simples do preço de fechamento de N dias; a banda superior é a banda média + M vezes o True Range de N dias do Canal de Keltner; a banda inferior é a banda média - M vezes o True Range de N dias do Canal de Keltner.

-

Calcular o Canal de Keltner. A banda média do Canal de Keltner é a média móvel simples do preço de fechamento de N dias; a banda superior é a banda média + M vezes o True Range de N dias; a banda inferior é a banda média - M vezes o True Range de N dias.

-

Determinar compressão e liberação. Quando a banda superior das Bandas de Bollinger está abaixo da banda superior do Canal de Keltner e a banda inferior das Bandas de Bollinger está acima da banda inferior do Canal de Keltner, é compressão. Quando a banda superior das Bandas de Bollinger está acima da banda superior do Canal de Keltner e a banda inferior das Bandas de Bollinger está abaixo da banda inferior do Canal de Keltner, é liberação.

-

Calcular a tendência establishment. Utilizando a média do preço de fechamento de N dias e o preço máximo/mínimo de N dias como entrada, calcula-se a regressão linear de N dias. Se o valor for maior que 0, indica tendência establishment de alta; se menor que 0, tendência establishment de baixa.

-

Sinais de negociação. Quando a tendência establishment é de alta, candle curto de alta e liberação são sinais de compra; quando a tendência establishment é de baixa, candle curto de baixa e compressão são sinais de venda.

Vantagens da Estratégia

-

Julgamento com múltiplos indicadores, aumentando a precisão dos sinais. Combinação de Bandas de Bollinger, Canal de Keltner e candles para avaliar o movimento do mercado, evitando sinais falsos.

-

Determinação da tendência establishment, operando conforme a tendência. Utiliza o establishment para julgar a tendência principal, evitando operações contrárias à tendência.

-

Stop Loss automático, controlando o risco. Quando o preço toca a linha de stop loss, a posição é encerrada automaticamente para limitar perdas.

Riscos da Estratégia

-

Parâmetros inadequados das Bandas de Bollinger e do Canal de Keltner podem levar a julgamentos incorretos de compressão e liberação.

-

O julgamento da tendência establishment pode ser atrasado, perdendo pontos de reversão da tendência.

-

Eventos repentinos podem causar movimentos extremos de preço, impossibilitando o stop loss, resultando em grandes perdas.

Métodos de otimização: ajustar os parâmetros das Bandas de Bollinger e do Canal de Keltner; utilizar indicadores auxiliares como ADX; atualizar o período da média establishment para reduzir atrasos; adicionar uma margem de segurança à linha de stop loss.

Direções de Otimização da Estratégia

-

Integrar mais indicadores técnicos para melhorar a precisão dos sinais de entrada, como KDJ, MACD, etc.

-

Otimizar o período da média establishment para capturar novas tendências mais rapidamente.

-

Adicionar indicadores de volume para evitar falsos rompimentos, como OBV (On-Balance Volume), Accumulation/Distribution, etc.

-

Julgamento em múltiplos períodos de tempo, distinguindo sinais de longo e curto prazo, para evitar ser “enrolado”.

-

Otimização de parâmetros com IA, buscando enumeração e combinações ótimas para reduzir overfitting.

Resumo

A principal ideia desta estratégia é: usar as Bandas de Bollinger para determinar a compressão e liberação do mercado; auxiliar com a tendência establishment para identificar a direção principal; operar na direção contrária ao establishment nos pontos de reversão entre compressão e liberação. As vantagens são sinais mais precisos, stop loss e evitação de sinais falsos. As direções de otimização incluem: combinação de múltiplos indicadores, otimização dos parâmetros de julgamento de tendência, adição de indicadores de volume, julgamento em múltiplos períodos de tempo, busca por parâmetros ótimos com IA, etc. No geral, esta estratégia baseia-se na auto-similaridade e nos ciclos de funcionamento do mercado, descrevendo as mudanças no ritmo do mercado por meio de indicadores, operando nos pontos críticos em que o mercado passa do acúmulo de energia para a liberação de energia, sendo uma estratégia típica de timing.

- 1