Estratégia de Trading de Duas Médias Móveis Baseada em CMO e WMA

Visão Geral

Esta estratégia é um sistema de médias móveis duplas baseado no indicador de momentum de preços Oscilador de Momentum Chandre (CMO) e sua média móvel ponderada (WMA). Ela tenta identificar reversões e continuações de tendência utilizando o cruzamento do CMO com sua WMA.

Princípio da Estratégia

A estratégia primeiro calcula o CMO, que mede as variações de momentum do preço ao longo do dia. Valores positivos indicam momentum de alta, valores negativos indicam momentum de baixa. Em seguida, calcula-se a WMA do CMO. Quando o CMO cruza acima de sua WMA, assume-se uma posição de alta; quando o CMO cruza abaixo de sua WMA, assume-se uma posição de baixa. A estratégia tenta capturar pontos de inflexão na tendência usando o cruzamento do CMO e da WMA.

As principais etapas para calcular o CMO são:

- Calcular a variação diária de preço (xMom)

- Calcular a média móvel simples (SMA) de n períodos da variação de preço, representando o "verdadeiro" momentum de preço (xSMA_mom)

- Calcular a variação líquida de preço de n períodos (xMomLength)

- Normalizar a variação líquida de preço (nRes) dividindo pela SMA

- Calcular a WMA de m períodos da variação líquida de preço normalizada para obter o CMO (xWMACMO)

A vantagem da estratégia é capturar os pontos de reversão das tendências de médio prazo dos preços. O valor absoluto do CMO reflete a força da tendência de preços, enquanto a WMA ajuda a filtrar falsos rompimentos.

Análise de Vantagens

A maior vantagem da estratégia é usar o valor absoluto do indicador CMO para avaliar o sentimento coletivo do mercado, e a filtragem pela WMA para identificar pontos de reversão de tendências de médio prazo. Comparada a estratégias de média móvel única, ela captura melhor as tendências de médio prazo com maior espaço elástico.

O CMO normaliza as variações de preço, mapeando-as para o intervalo -100 a 100, facilitando a avaliação do sentimento do mercado; o valor absoluto representa a força da tendência atual. A WMA fornece uma filtragem adicional ao CMO, evitando muitos sinais falsos.

Análise de Riscos

Os principais riscos potenciais da estratégia incluem:

- Parâmetros inadequados do CMO e da WMA, gerando muitos sinais falsos

- Incapacidade de lidar efetivamente com mercados laterais ou oscilantes, resultando em alta frequência de negociações e custos de slippage

- Incapacidade de identificar tendências reais de longo prazo, podendo incorrer em riscos de perda em posições de longa duração

Os métodos de otimização correspondentes incluem:

- Ajustar os parâmetros do CMO e da WMA para encontrar a combinação ideal

- Adicionar filtros adicionais, como indicadores de volume, para evitar negociações em mercados oscilantes

- Combinar indicadores de prazo mais longo, como a média de 90 dias, para evitar a perda de oportunidades em tendências de longo prazo

Direções de Otimização

As direções de otimização da estratégia concentram-se principalmente na otimização de parâmetros, filtragem de sinais e stop loss:

- Otimização de parâmetros do CMO e da WMA: encontrar a combinação ideal por meio de busca exaustiva

- Combinar indicadores auxiliares como volume e índice de força para filtrar sinais, evitando falsos rompimentos

- Adicionar mecanismo de stop loss dinâmico: sair da posição quando o preço cair abaixo do CMO e da WMA novamente

- Considerar o padrão de falha de rompimento (Breakout Failure) como sinal de entrada, ou seja, quando o CMO e a WMA primeiro rompem um nível chave, mas rapidamente caem abaixo dele

- Combinar indicadores de prazo mais longo para determinar a tendência geral, evitando negociações contrárias à tendência

Resumo

A estratégia geral utiliza o indicador CMO para julgar a força e os pontos de reversão da tendência, combinado com a WMA para filtrar e gerar sinais de negociação, caracterizando-se como um sistema típico de médias móveis duplas. Em comparação com estratégias de média móvel única, possui maior vantagem na captura de tendências elásticas de médio prazo. No entanto, ainda há espaço para otimização nos parâmetros e na filtragem. Controlar adequadamente a frequência de negociações e introduzir stop loss dinâmico podem melhorar ainda mais a estabilidade do sistema.

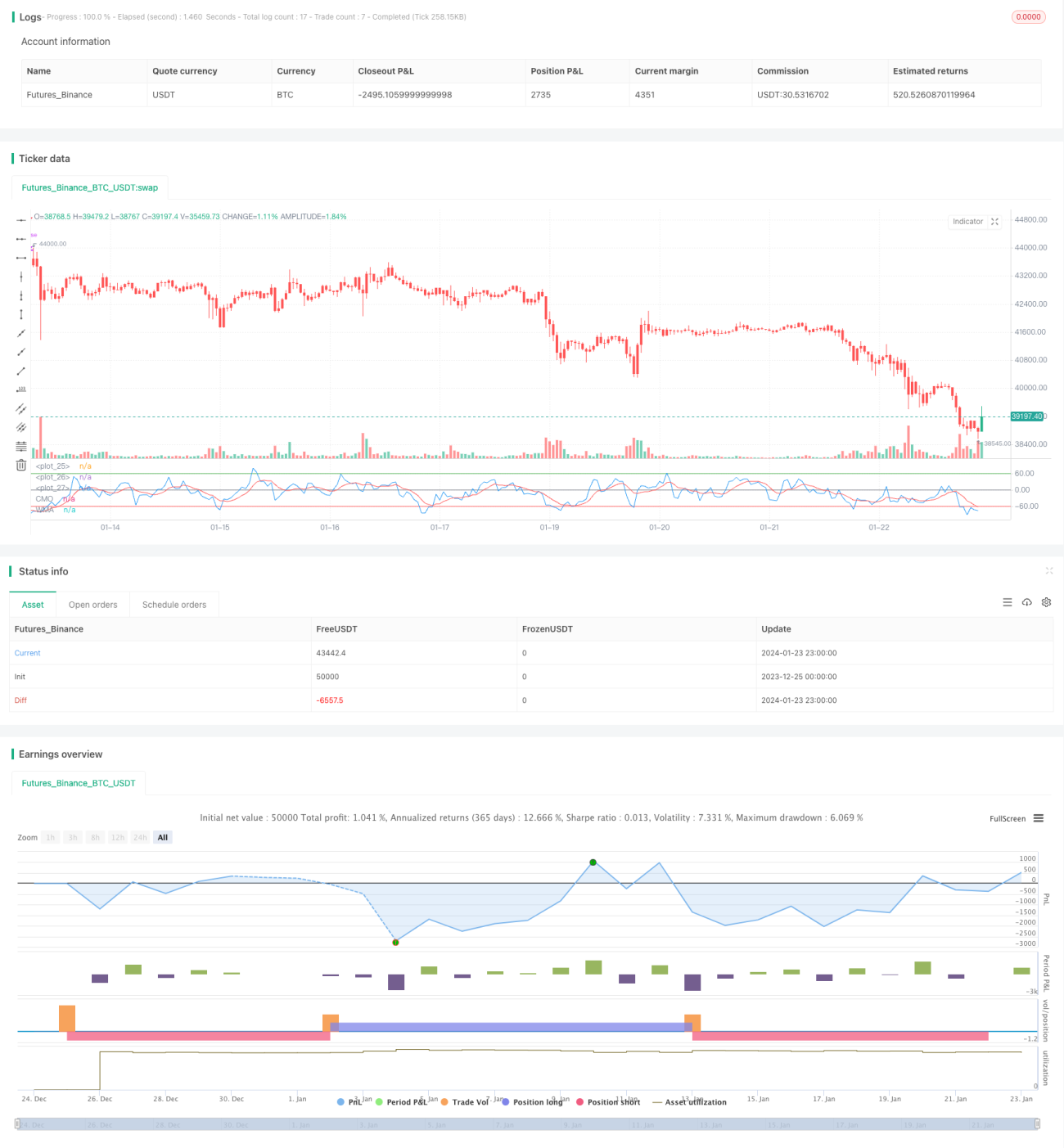

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/10/2018

// This indicator plots Chandre Momentum Oscillator and its WMA on the - 1