ہل سویٹ حکمت عملی

مصنف:چاؤ ژانگ، تاریخ: 2022-05-25 18:48:40ٹیگز:ایچ ایم اےTHMAای ایچ ایم اےای ایم اےڈبلیو ایم اے

آسان بیک ٹیسٹنگ کے لئے ایک حکمت عملی اسکرپٹ میں ہول سویٹ تبدیل اور بیک ٹیسٹنگ کے لئے ایک وقت کی مدت کی وضاحت کرنے کی صلاحیت شامل کر دیا.

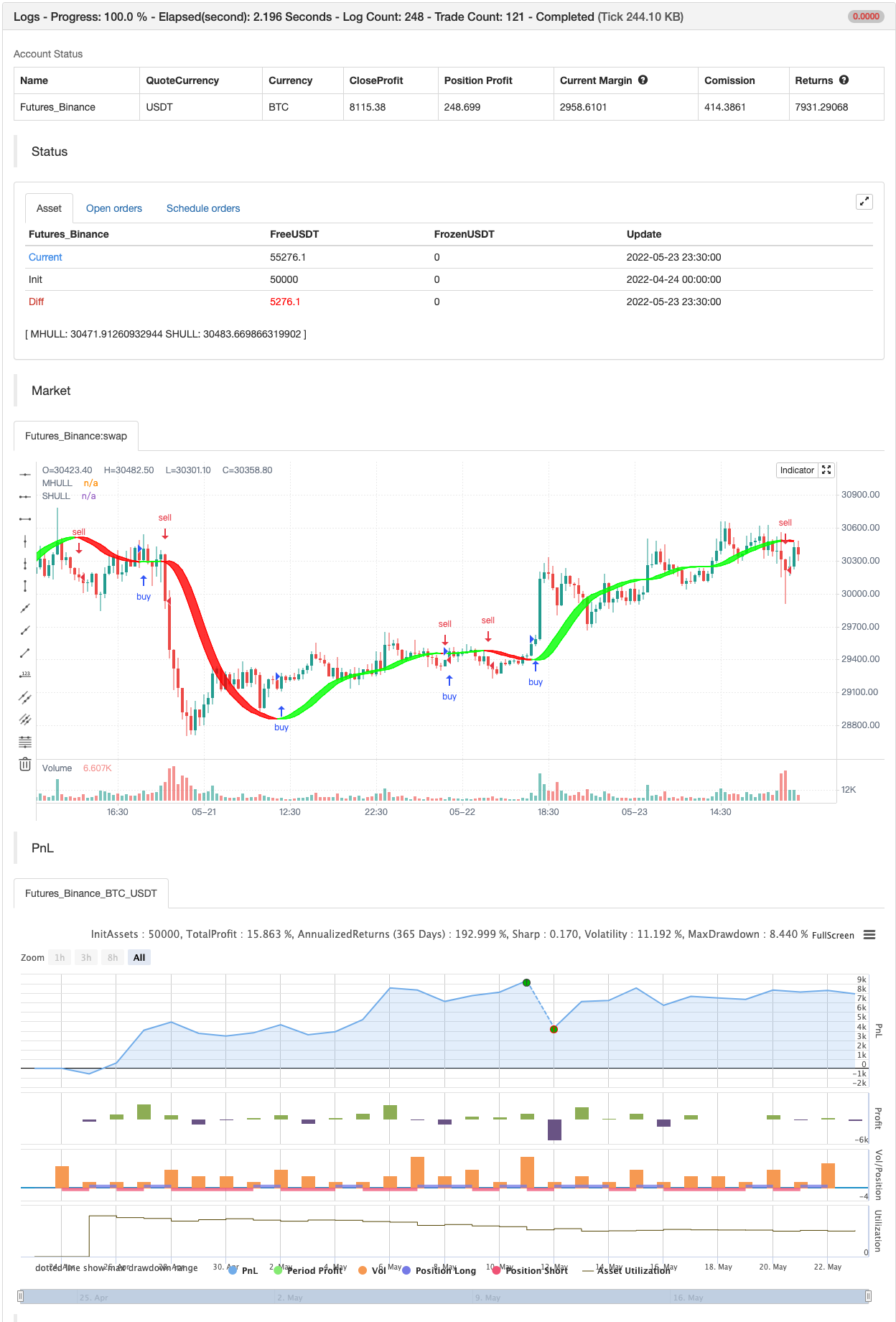

بیک ٹسٹ

/*backtest

start: 2022-04-24 00:00:00

end: 2022-05-23 23:59:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//Basic Hull Ma Pack tinkered by InSilico

//Converted to Strategy by DashTrader

strategy("Hull Suite Strategy", overlay=true, pyramiding=1, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0)

strat_dir_input = input(title="Strategy Direction", defval="long", options=["long", "short", "all"])

// strat_dir_value = strat_dir_input == "long" ? strategy.direction.long : strat_dir_input == "short" ? strategy.direction.short : strategy.direction.all

// strategy.risk.allow_entry_in(strat_dir_value)

//////////////////////////////////////////////////////////////////////

// Testing Start dates

testStartYear = input(2016, "Backtest Start Year")

testStartMonth = input(1, "Backtest Start Month")

testStartDay = input(1, "Backtest Start Day")

testPeriodStart = timestamp(testStartYear,testStartMonth,testStartDay,0,0)

//Stop date if you want to use a specific range of dates

testStopYear = input(2030, "Backtest Stop Year")

testStopMonth = input(12, "Backtest Stop Month")

testStopDay = input(30, "Backtest Stop Day")

testPeriodStop = timestamp(testStopYear,testStopMonth,testStopDay,0,0)

testPeriod() => true

// Component Code Stop

//////////////////////////////////////////////////////////////////////

//INPUT

src = input(close, title="Source")

modeSwitch = input("Hma", title="Hull Variation", options=["Hma", "Thma", "Ehma"])

length = input(55, title="Length(180-200 for floating S/R , 55 for swing entry)")

switchColor = input(true, "Color Hull according to trend?")

candleCol = input(false,title="Color candles based on Hull's Trend?")

visualSwitch = input(true, title="Show as a Band?")

thicknesSwitch = input(1, title="Line Thickness")

transpSwitch = input(40, title="Band Transparency",step=5)

//FUNCTIONS

//HMA

HMA(_src, _length) => wma(2 * wma(_src, _length / 2) - wma(_src, _length), round(sqrt(_length)))

//EHMA

EHMA(_src, _length) => ema(2 * ema(_src, _length / 2) - ema(_src, _length), round(sqrt(_length)))

//THMA

THMA(_src, _length) => wma(wma(_src,_length / 3) * 3 - wma(_src, _length / 2) - wma(_src, _length), _length)

//SWITCH

Mode(modeSwitch, src, len) =>

modeSwitch == "Hma" ? HMA(src, len) :

modeSwitch == "Ehma" ? EHMA(src, len) :

modeSwitch == "Thma" ? THMA(src, len/2) : na

//OUT

HULL = Mode(modeSwitch, src, length)

MHULL = HULL[0]

SHULL = HULL[2]

//COLOR

hullColor = switchColor ? (HULL > HULL[2] ? #00ff00 : #ff0000) : #ff9800

//PLOT

///< Frame

Fi1 = plot(MHULL, title="MHULL", color=hullColor, linewidth=thicknesSwitch, transp=50)

Fi2 = plot(visualSwitch ? SHULL : na, title="SHULL", color=hullColor, linewidth=thicknesSwitch, transp=50)

///< Ending Filler

fill(Fi1, Fi2, title="Band Filler", color=hullColor, transp=transpSwitch)

///BARCOLOR

barcolor(color = candleCol ? (switchColor ? hullColor : na) : na)

if HULL[0] > HULL[2] and testPeriod()

strategy.entry("buy", strategy.long)

if HULL[0] < HULL[2] and testPeriod()

strategy.entry("sell", strategy.short)

متعلقہ

- ریڈ کے مومنٹم بارز

- رفتار پر مبنی زگ زگ

- وی ڈبلیو ایم اے-اے ڈی ایکس مومنٹم اور ٹرینڈ پر مبنی بٹ کوائن لانگ حکمت عملی

- ہل منتقل اوسط سوئنگ ٹریڈر

- کم سکینر حکمت عملی کریپٹو

- ولیمز %R - ہموار

- HALFTREND + HEMA + SMA (غلط سگنل کی حکمت عملی)

- توانائی کی سلاخوں کے ساتھ ریڈ کے ڈبل ویڈر

- چلتی اوسط کراس الرٹ، ملٹی ٹائم فریم (MTF)

- ریڈ کے حجم تیز رفتار سمت توانائی کا تناسب

مزید

- سوئنگ ٹریڈ سگنل

- شیف رجحان سائیکل

- 72s: ایڈجسٹ ہول چلتی اوسط +

- خرید/فروخت کے ساتھ EMA ADX RSI کا اسکیلپنگ

- حجم کا فرق

- سپر ٹرینڈ ڈیلی 2.0 BF

- ہل منتقل اوسط سوئنگ ٹریڈر

- FTSMA - رجحان آپ کا دوست ہے

- رینج فلٹر خریدیں اور فروخت کریں

- ایس ایس ایل چینل

- پیرابولک SAR خریدیں اور فروخت کریں

- پییوٹ پر مبنی ٹریلنگ زیادہ سے زیادہ اور کم سے کم

- نِک رِپاک ٹریلنگ ریورس (NRTR)

- ZigZag PA حکمت عملی V4.1

- دن کے اندر خرید/فروخت

- ٹوٹا ہوا فریکٹل: کسی کا ٹوٹا ہوا خواب آپ کا منافع ہے!

- منافع بڑھانے والا PMax

- ناقص فتح کی حکمت عملی

- اسٹوکاسٹک + آر ایس آئی، ڈبل حکمت عملی

- سوئنگ ہول/آر ایس آئی/ای ایم اے حکمت عملی