Triple Supertrend với EMA và ADX

Tác giả:ChaoZhang, Ngày: 2022-05-08 20:48:42Tags:EMAADX

Công bố một chiến lược bao gồm cả bộ lọc adx và ema

Nhập: cả ba Supertrend trở thành tích cực. Nếu một bộ lọc của ADX và EMA được áp dụng, cũng kiểm tra xem ADX là trên mức chọn và đóng là trên EMA Exit: khi siêu xu hướng đầu tiên trở nên âm

đối diện cho các mục ngắn

Một Filter được cung cấp để lấy hoặc tránh nhập lại trên cùng một bên. Ví dụ: Sau khi thoát ra lâu, nếu điều kiện nhập lại được thỏa mãn lâu trước khi đơn ngắn được kích hoạt, nó sẽ nhập lại nếu được chọn.

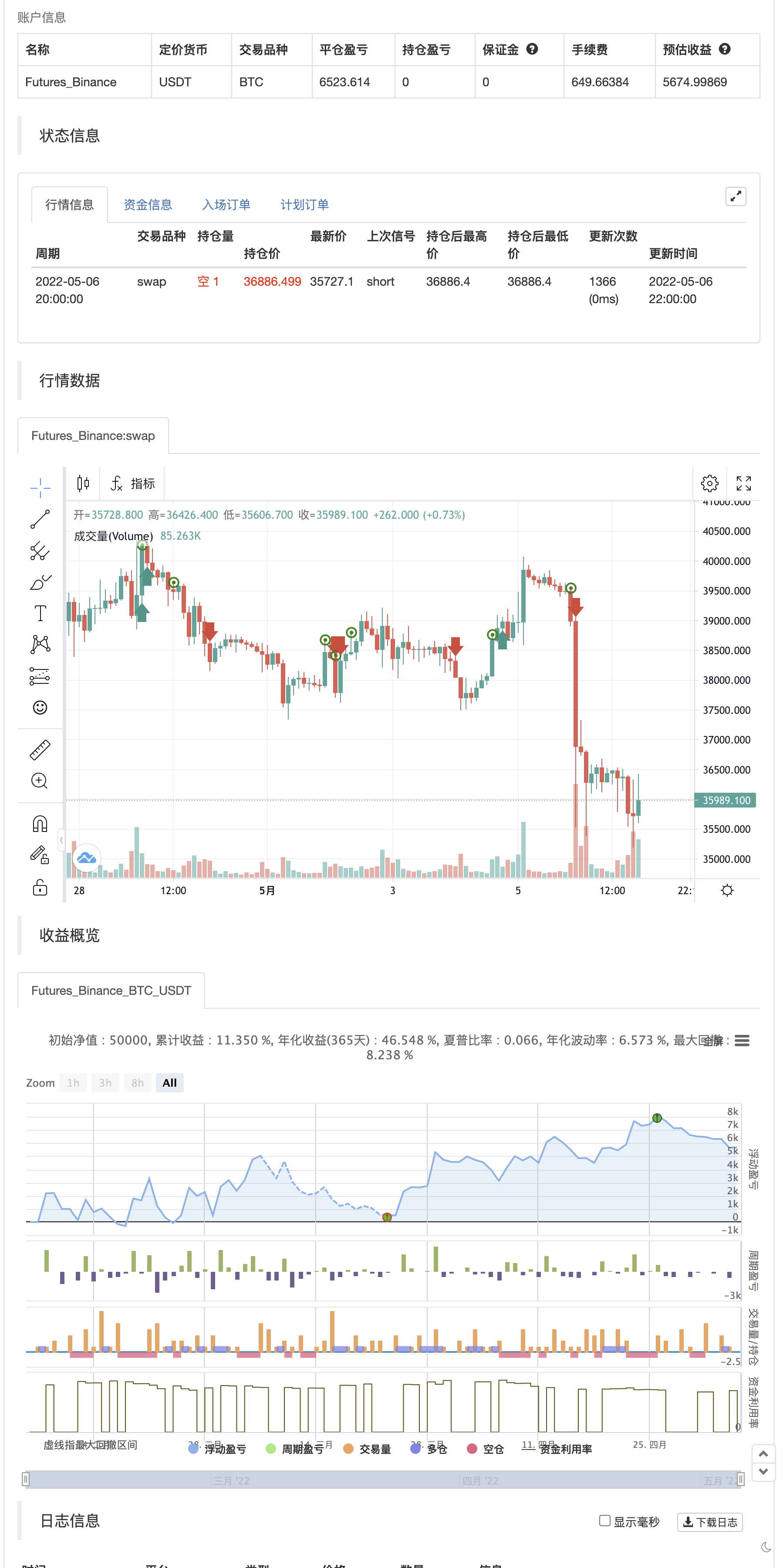

backtest

/*backtest

start: 2022-02-07 00:00:00

end: 2022-05-07 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// ©kunjandetroja

//@version=5

strategy('Triple Supertrend with EMA and ADX', overlay=true)

m1 = input.float(1,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 1')

m2 = input.float(2,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 2')

m3 = input.float(3,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 3')

p1 = input.int(10,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 1')

p2 = input.int(15,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 2')

p3 = input.int(20,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 3')

len_EMA = input.int(200,"EMA Len",minval = 5,maxval= 250,step=1)

len_ADX = input.int(14,"ADX Len",minval = 1,maxval= 25,step=1)

len_Di = input.int(14,"Di Len",minval = 1,maxval= 25,step=1)

adx_above = input.float(25,"adx filter",minval = 1,maxval= 50,step=0.5)

var bool long_position = false

adx_filter = input.bool(false, "Add Adx & EMA filter")

renetry = input.bool(true, "Allow Reentry")

f_getColor_Resistance(_dir, _color) =>

_dir == 1 and _dir == _dir[1] ? _color : na

f_getColor_Support(_dir, _color) =>

_dir == -1 and _dir == _dir[1] ? _color : na

[superTrend1, dir1] = ta.supertrend(m1, p1)

[superTrend2, dir2] = ta.supertrend(m2, p2)

[superTrend3, dir3] = ta.supertrend(m3, p3)

EMA = ta.ema(close, len_EMA)

[diplus,diminus,adx] = ta.dmi(len_Di,len_ADX)

// ADX Filter

adxup = adx > adx_above and close > EMA

adxdown = adx > adx_above and close < EMA

sum_dir = dir1 + dir2 + dir3

dir_long = if(adx_filter == false)

sum_dir == -3

else

sum_dir == -3 and adxup

dir_short = if(adx_filter == false)

sum_dir == 3

else

sum_dir == 3 and adxdown

Exit_long = dir1 == 1 and dir1 != dir1[1]

Exit_short = dir1 == -1 and dir1 != dir1[1]

// BuySignal = dir_long and dir_long != dir_long[1]

// SellSignal = dir_short and dir_short != dir_short[1]

// if BuySignal

// label.new(bar_index, low, 'Long', style=label.style_label_up)

// if SellSignal

// label.new(bar_index, high, 'Short', style=label.style_label_down)

longenter = if(renetry == false)

dir_long and long_position == false

else

dir_long

shortenter = if(renetry == false)

dir_short and long_position == true

else

dir_short

if longenter

long_position := true

if shortenter

long_position := false

strategy.entry('BUY', strategy.long, when=longenter)

strategy.entry('SELL', strategy.short, when=shortenter)

strategy.close('BUY', Exit_long)

strategy.close('SELL', Exit_short)

//buy1 = ta.barssince(dir_long)

//sell1 = ta.barssince(dir_short)

//colR1 = f_getColor_Resistance(dir1, color.red)

//colS1 = f_getColor_Support(dir1, color.green)

//colR2 = f_getColor_Resistance(dir2, color.orange)

//colS2 = f_getColor_Support(dir2, color.yellow)

//colR3 = f_getColor_Resistance(dir3, color.blue)

//colS3 = f_getColor_Support(dir3, color.maroon)

//plot(superTrend1, 'R1', colR1, linewidth=2)

//plot(superTrend1, 'S1', colS1, linewidth=2)

//plot(superTrend2, 'R1', colR2, linewidth=2)

//plot(superTrend2, 'S1', colS2, linewidth=2)

//plot(superTrend3, 'R1', colR3, linewidth=2)

//plot(superTrend3, 'S1', colS3, linewidth=2)

// // Intraday only

// var int new_day = na

// var int new_month = na

// var int new_year = na

// var int close_trades_after_time_of_day = na

// if dayofmonth != dayofmonth[1]

// new_day := dayofmonth

// if month != month[1]

// new_month := month

// if year != year[1]

// new_year := year

// close_trades_after_time_of_day := timestamp(new_year,new_month,new_day,15,15)

// strategy.close_all(time > close_trades_after_time_of_day)

Có liên quan

- GM-8 & ADX Chiến lược trung bình di chuyển kép

- VuManChu Cipher B + Divergences chiến lược

- Chiến lược lưới vị trí biến động theo xu hướng

- Scalping EMA ADX RSI với Buy/Sell

- VWMA-ADX Momentum và Chiến lược dài Bitcoin dựa trên xu hướng

- Chiến lược DCA động dựa trên khối lượng

- Lý thuyết sóng Elliott 4-9 Sóng xung phát hiện tự động Chiến lược giao dịch

- stoch supertrd atr 200ma

- Hệ thống CM Sling Shot

- Đòn búa đảo ngược - Tùy chọn mở rộng

Thêm nữa

- EMA bands + leledc + bollinger bands

- RSI MTF Ob+Os

- Chiến lược MACD Willy

- RSI - Bán tín hiệu mua

- Xu hướng Heikin-Ashi

- HA Xấu đảo thị trường

- Ichimoku Cloud Smooth Oscillator

- Williams %R - Đơn giản hóa

- QQE MOD + SSL Hybrid + Waddah Attar vụ nổ

- Mua/Bán Strat

- Bản đồ nhiệt theo trình tự Tom DeMark

- jma + dwma bằng nhiều hạt

- MACD MAGIC

- Điểm số Z với tín hiệu

- Phương pháp biến động dễ dàng của Ngôn ngữ Pine

- 3EMA + Boullinger + PIVOT

- Baguette bằng nhiều hạt

- Máy xay

- Chỉ số đảo ngược của K I

- Nến tràn ngập