Chiến lược giao dịch bóng

Tổng quan

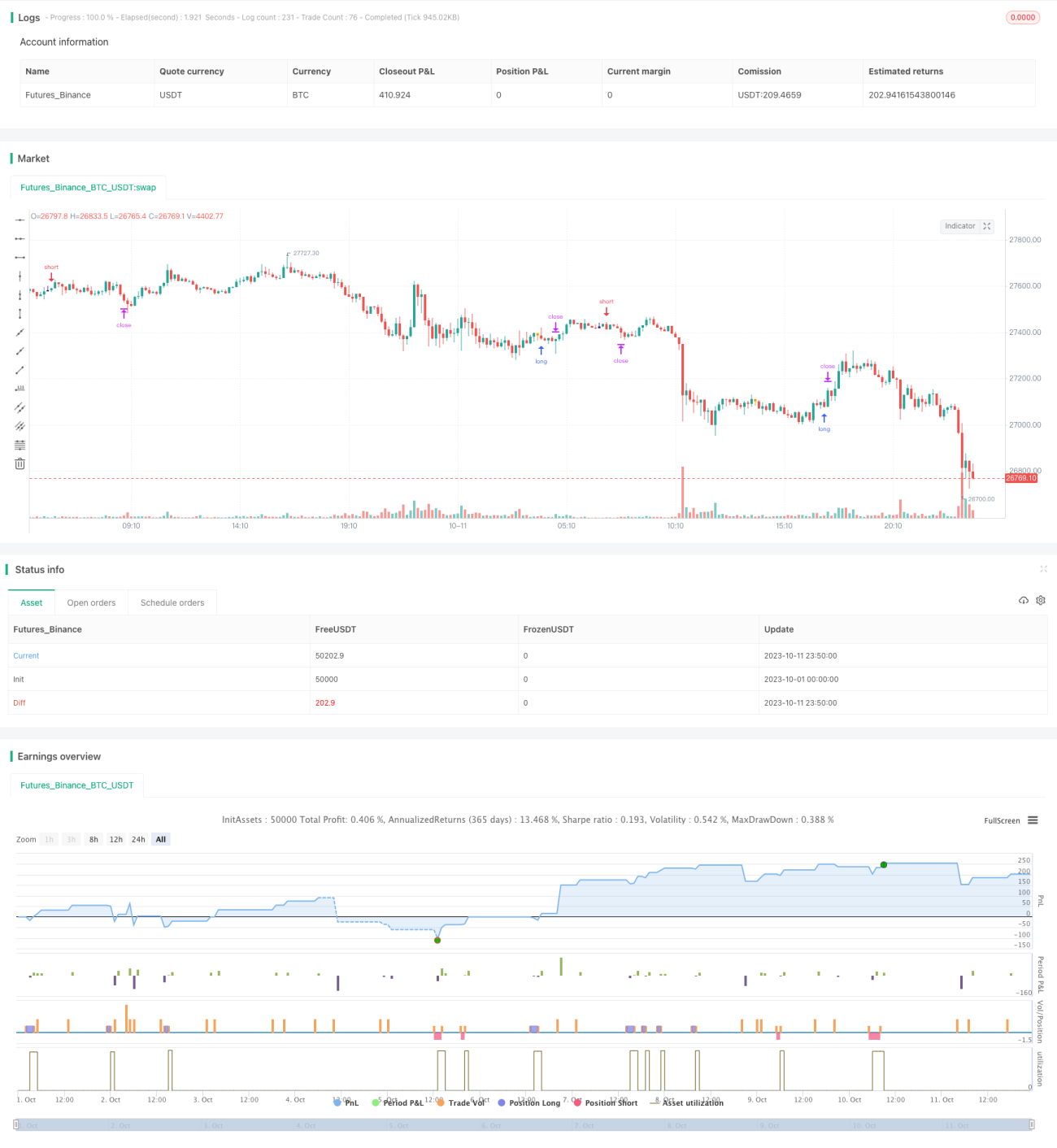

Chiến lược giao dịch bóng (Shadow Trading Strategy) xác định thời điểm thị trường có thể đảo chiều bằng cách nhận diện các nến có bóng dưới dài hoặc bóng trên dài. Khi phát hiện bóng dưới dài, mua lên; khi phát hiện bóng trên dài, bán xuống. Chiến lược này chủ yếu tận dụng quy luật phổ biến về sự đảo chiều của nến có bóng dài để giao dịch.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược giao dịch bóng là nhận diện các nến có bóng trên dài và bóng dưới dài. Chiến lược tính toán kích thước thân nến corpo và kích thước bóng pinnaL, pinnaS. Khi kích thước bóng lớn hơn một bội số nhất định của thân nến, được cho là có cơ hội đảo chiều. Cụ thể, chiến lược bao gồm các bước sau:

- Tính kích thước thân nến

corpo, tức là giá trị tuyệt đối của chênh lệch giữa giá mở cửa và giá đóng cửa. - Tính bóng trên

pinnaL, tức là giá trị tuyệt đối của chênh lệch giữa giá cao nhất và giá đóng cửa. - Tính bóng dưới

pinnaS, tức là giá trị tuyệt đối của chênh lệch giữa giá thấp nhất và giá đóng cửa. - Kiểm tra xem bóng trên có lớn hơn một bội số của thân nến hay không, thông qua

pinnaL > (corpo*size), trong đósizelà tham số có thể điều chỉnh. - Kiểm tra xem bóng dưới có lớn hơn một bội số của thân nến hay không, thông qua

pinnaS > (corpo*size). - Nếu điều kiện trên đúng, tại thời điểm đóng cửa của nến có bóng, thực hiện bán xuống (bóng trên dài) hoặc mua lên (bóng dưới dài).

Ngoài ra, chiến lược còn kiểm tra biên độ dao động dim của nến có lớn hơn giá trị tối thiểu min hay không, để lọc bỏ các nến có biến động quá nhỏ. Sau khi vào lệnh, thiết lập cắt lỗ và chốt lời để thoát lệnh.

Phân tích ưu điểm chiến lược

- Tận dụng quy luật đảo chiều của nến có bóng dài, đây là một tín hiệu giao dịch tương đối đáng tin cậy.

- Logic chiến lược đơn giản, rõ ràng, tham số thiết lập trực quan, dễ nắm bắt.

- Có thể kiểm soát tần suất vào lệnh bằng cách điều chỉnh tham số, linh hoạt quản lý rủi ro giao dịch.

- Có thể tối ưu hóa thêm bằng cách kết hợp với xu hướng, hỗ trợ/kháng cự và các yếu tố khác.

Rủi ro và giải pháp

- Có tồn tại xác suất đảo chiều bóng dài thất bại, không đảo chiều, có thể giảm rủi ro bằng cách điều chỉnh tham số.

- Cần kết hợp với phán đoán xu hướng, tránh giao dịch ngược xu hướng.

- Cần tối ưu tham số cho từng sản phẩm cụ thể, các sản phẩm khác nhau có thể có tham số khác nhau.

- Có thể kết hợp các chỉ báo khác để lọc cơ hội vào lệnh, giảm tỷ lệ lợi nhuận để đổi lấy tỷ lệ thắng cao hơn.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số theo từng sản phẩm khác nhau, nâng cao độ ổn định của chiến lược.

- Kết hợp các chỉ báo như đường trung bình động để phán đoán xu hướng, tránh giao dịch ngược xu hướng.

- Thêm phán đoán phá vỡ đỉnh hoặc đáy trước đó, nâng cao hiệu quả của chiến lược.

- Tối ưu và điều chỉnh vị trí cắt lỗ/chốt lời, giảm thiểu rủi ro thua lỗ tối đa trong khi vẫn giữ lợi nhuận.

- Tối ưu hóa quản lý vị thế, có thể đặt vị thế khác nhau cho các sản phẩm khác nhau.

Tổng kết

Chiến lược giao dịch bóng là một chiến lược giao dịch ngắn hạn tương đối đơn giản và thực tế. Nó tạo tín hiệu giao dịch dựa trên quy luật đảo chiều phổ biến của nến có bóng dài. Chiến lược có logic đơn giản, dễ thực hiện, có thể điều chỉnh và tối ưu hóa theo sự khác biệt giữa các sản phẩm. Đồng thời, chiến lược giao dịch bóng cũng tồn tại những rủi ro nhất định, cần kết hợp với xu hướng và các yếu tố khác để lọc lọc, giảm xác suất giao dịch sai. Nếu được sử dụng đúng cách, chiến lược giao dịch bóng có thể trở thành một phần hiệu quả trong hệ thống giao dịch định lượng.

- 1