Quantitative Handelsstrategie, die Trend und Seitwärtsbewegungen kombiniert

Überblick

Die Zwei-Trend-Oszillator-Strategie ist eine quantitative Handelsstrategie, die Trend- und Oszillatorelemente kombiniert. Sie nutzt die Kombination zweier Indikatoren, um die Richtung und Stärke eines Trends zu identifizieren und günstige Einstiegszeitpunkte während trendender Oszillationen zu finden.

Strategieprinzip

Die Strategie verwendet hauptsächlich zwei öffentliche Indikatoren: Trend Surfers und Mawreez‘s Trend Oscillator.

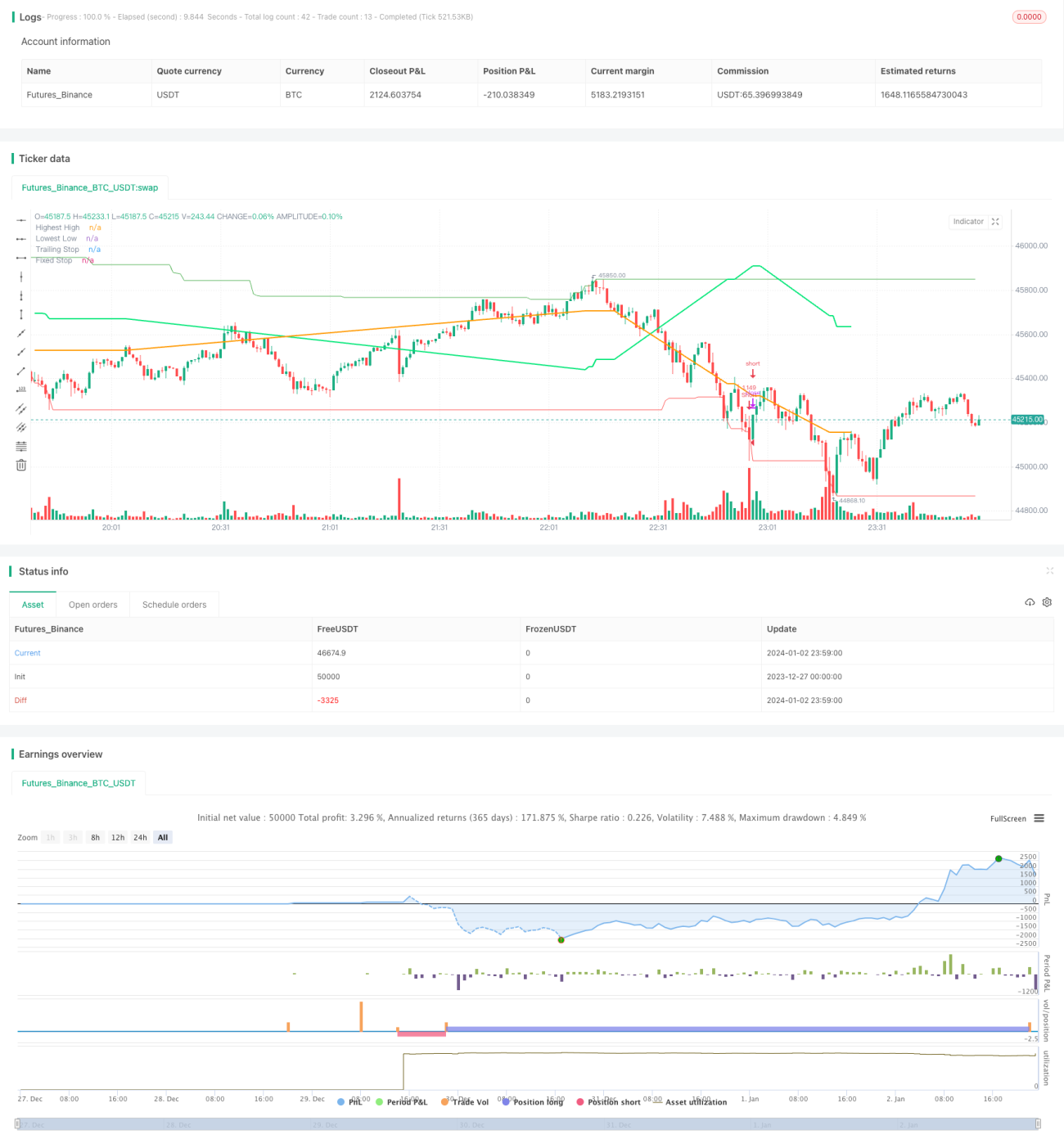

Trend Surfers ist ein Trendfolge-Stopp-Loss-Indikator. Er berechnet die Höchst- und Tiefstkurse über einen bestimmten Zeitraum, um die Preisentwicklung zu beurteilen und empfohlene Stopp-Loss-Positionen zu liefern. Beispielsweise signalisiert ein Durchbruch des Preises über das Höchst der letzten 168 Kerzen ein bullishes Signal; ein Unterschreiten des Tiefs der letzten 168 Kerzen ein bearishes Signal.

Mawreez‘s Trend Oscillator ist ein zweiliniger Oszillator. Er ähnelt dem MACD und nutzt die Differenz der DI-Werte, um Trendrichtung und -stärke zu bestimmen. Liegt die Indikatorlinie über der Nulllinie, gilt dies als bullish, darunter als bearish.

Die Handelsregeln der Strategie lauten:

- Long-Einstieg: Wenn Trend Surfers die obere Linie durchbricht und Mawreez‘s Trend Oscillator bullish signalisiert, wird gekauft.

- Short-Einstieg: Wenn Trend Surfers die untere Linie unterschreitet und Mawreez‘s Trend Oscillator bearish signalisiert, wird verkauft.

Der Stopp-Loss erfolgt durch eine Kombination aus Trendfolge-Stopp und festem Stopp.

Vorteilsanalyse

Die Strategie vereint Trend- und Oszillatorindikatoren. Sie kann sowohl Trends erfassen als auch günstige Einstiegspreise in Seitwärtsbewegungen finden. Die Vorteile sind:

- Doppelte Indikatorfilterung – vermeidet effektiv Fehlausbrüche.

- Kombination von Trend und Oszillation – ermöglicht günstige Positionierungen in Konsolidierungszonen (z. B. Akkumulation auf niedrigem Niveau oder leichter Einstieg auf hohem Niveau).

- Mehrere Stopp-Loss-Methoden – bieten gute Risikokontrolle.

Risikoanalyse

Die Strategie birgt auch einige Risiken:

- Die doppelte Indikatorkombination kann zu verpassten Signalen führen.

- Trend- und Oszillatorindikatoren können widersprüchliche Signale liefern.

- Ein fester Stopp-Loss kann zu früh auslösen.

Um diese Risiken zu mindern, können folgende Maßnahmen ergriffen werden:

- Aufweichung der Indikatorparameter – Senkung der Filterrate.

- Erweiterung der Trendregeln – Vermeidung von Indikatorkonflikten.

- Dynamische Anpassung des Stopp-Loss-Niveaus.

Optimierungsmöglichkeiten

Die Strategie bietet weiteres Optimierungspotenzial:

- Testen verschiedener Parameter- und Periodenkombinationen zur Ermittlung optimaler Einstellungen.

- Integration zusätzlicher Hilfsindikatoren wie Volatilität, Handelsvolumen usw.

- Einsatz maschinellen Lernens zur dynamischen Optimierung von Indikatoren und Parametern.

Zusammenfassung

Die Zwei-Trend-Oszillator-Strategie vereint die Stärken von Trendfolge- und Oszillatoren. Sie erkennt sowohl Trendrichtungen als auch Seitwärtschancen. Durch Optimierung von Parametern und Regeln kann ihre Profitabilität weiter gesteigert werden. Die Strategie besitzt ein vielversprechendes Entwicklungspotenzial.

- 1