Zweiseitige ADX-Handelsstrategie

Übersicht

Die Bidirektionale ADX-Handelsstrategie ist eine quantitative Strategie, die den Average Directional Index (ADX) nutzt, um in beide Marktrichtungen zu handeln. Die Strategie berechnet den ADX-Indikator sowie die Differenz zwischen DIPlus und DIMinus, legt einen Schwellenwert zur Bestimmung von Handelssignalen fest und führt Long- und Short-Trades durch, um Gewinne zu erzielen.

Funktionsprinzip der Strategie

- Berechnung der wahren Spannweite (True Range)

- Berechnung der Aufwärtsrichtung (Directional Movement Plus) und der Abwärtsrichtung (Directional Movement Minus)

- Berechnung der geglätteten wahren Spannweite (Smoothed True Range)

- Berechnung der geglätteten Aufwärtsbewegung (Smoothed Directional Movement Plus) und der geglätteten Abwärtsbewegung (Smoothed Directional Movement Minus)

- Berechnung der Indikatoren DIPlus, DIMinus und ADX

- Berechnung der Differenz zwischen DIPlus und ADX sowie zwischen DIMinus und ADX

- Festlegung von Schwellenwerten für die Differenz bei Long- und Short-Trades

- Wenn die Differenz den Schwellenwert übersteigt, wird ein Handelssignal ausgelöst

- Erzeugung von Kauf- und Verkaufsaufträgen

Der Kern dieser Strategie liegt darin, mit Indikatoren wie dem ADX die Trendrichtung und -stärke zu bestimmen, mithilfe der Differenz-Regel einen Schwellenwert festzulegen und automatische Trades durchzuführen.

Vorteile der Strategie

- Durch die Nutzung des ADX zur Bestimmung der Trendrichtung können Markttrends präzise erfasst werden.

- Die Anwendung der Differenz-Regel filtert effektiv falsche Signale heraus.

- Bidirektionaler Handel ermöglicht die vollständige Nutzung von Long- und Short-Chancen.

- Vollautomatischer Handel ohne menschliches Eingreifen.

- Die Logik der Strategie ist klar, leicht verständlich und einfach zu modifizieren.

Risikoanalyse

- Der ADX-Indikator weist eine Verzögerung auf, was dazu führen kann, dass Trendwenden verpasst werden.

- Das Risiko steigt durch den bidirektionalen Handel, Verluste können sich vergrößern.

- Falsche Parametereinstellungen können zu übermäßigem Handel führen.

- Backtest-Daten können nicht den tatsächlichen Markt repräsentieren, das Risiko im Live-Handel bleibt bestehen.

Lösungsansätze:

- Kombination mit anderen Indikatoren zur Bestätigung von Handelssignalen

- Optimierung der Parameter zur Kontrolle der Handelsfrequenz

- Strenge Position-Sizing-Verwaltung der Handelsgrößen

Optimierungsmöglichkeiten

- Optimierung der ADX-Parameter zur Verbesserung der Empfindlichkeit

- Hinzufügen weiterer Indikatoren zur Signalfilterung

- Anwendung von Algorithmen des maschinellen Lernens zur Parameteroptimierung

- Einsatz fortschrittlicher Stop-Loss-Strategien zur Verlustbegrenzung

- Kombination mit Modellvorhersagen für präzisere Handelssignale

Zusammenfassung

Die Bidirektionale ADX-Handelsstrategie ist insgesamt eine sehr praktische quantitative Strategie. Sie nutzt den ADX-Indikator zur Trendbestimmung und erfasst bidirektional Handelschancen. Gleichzeitig stellt die Differenz-Regel die Gültigkeit der Signale sicher. Die Logik der Strategie ist klar und einfach, sie lässt sich leicht modifizieren und optimieren und ist eine bidirektionale Trendfolgestrategie. Durch angemessene Parameteroptimierung, den Einsatz von Stop-Loss-Strategien und Signalfilterung kann die Stabilität und Rentabilität der Strategie weiter gesteigert werden.

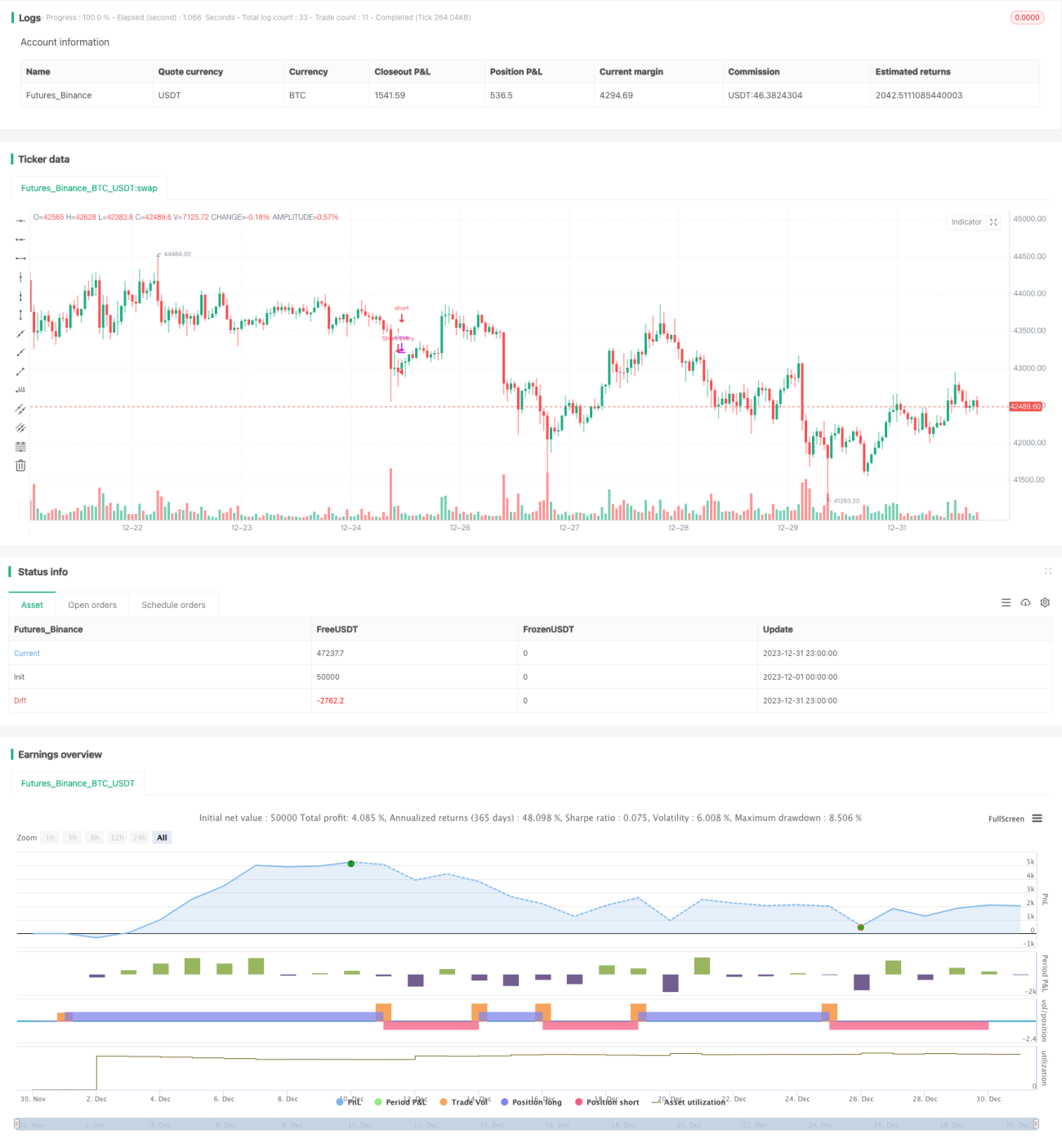

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1