Quantitative Handelsstrategie basierend auf dynamischen gleitenden Durchschnitten mehrerer Basiswerte

Überblick

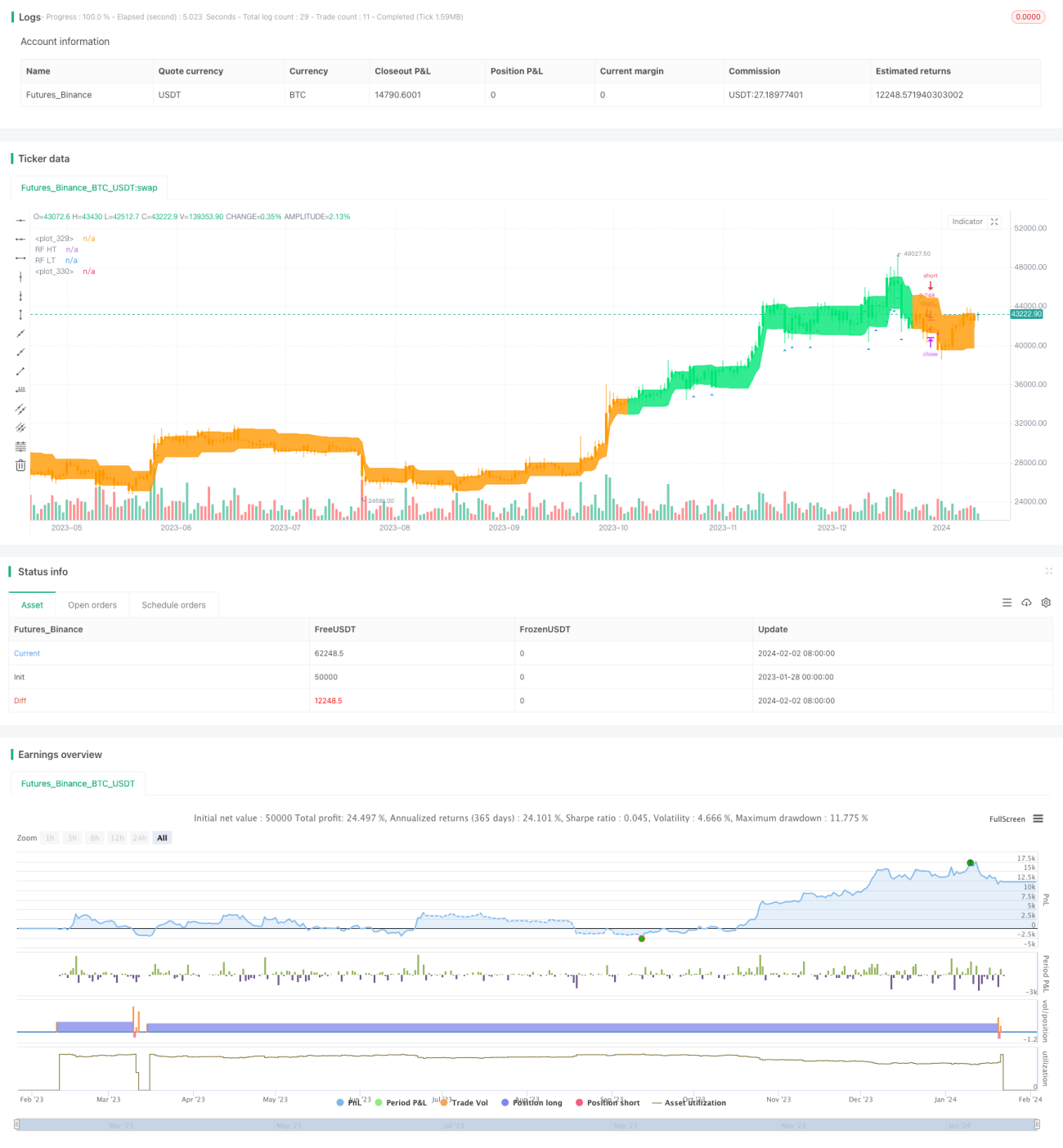

Diese Strategie nutzt die kombinierten Signale mehrerer technischer Indikatoren, um den dynamischen Handel mit Vermögenswerten wie Aktien und Kryptowährungen zu ermöglichen. Die Strategie kann automatisch Markttrends erkennen und diesen folgen. Gleichzeitig ist ein Stop-Loss-Mechanismus integriert, um Risiken zu kontrollieren.

Funktionsweise der Strategie

Die Strategie verwendet mehrere Indikatoren wie gleitende Durchschnitte, den Relative Strength Index (RSI), die Average True Range (ATR) und den Directional Movement Index (ADX). Durch die Kombination dieser Indikatoren werden Handelssignale generiert.

Im Einzelnen erzeugt die Strategie zunächst mit einem doppelten gleitenden Durchschnittssystem Kaufsignale (Goldenes Kreuz) und Verkaufssignale (Todeskreuz). Die schnelle Linie hat eine Länge von 10, die langsame Linie von 50. Wenn die schnelle Linie die langsame Linie von unten nach oben durchbricht, entsteht ein Kaufsignal; durchbricht sie von oben nach unten, ein Verkaufssignal. Dieses doppelte gleitende Durchschnittssystem kann Wendepunkte mittel- bis langfristiger Trends zuverlässig erkennen.

Aufbauend auf den gleitenden Durchschnitten wird der RSI-Indikator eingesetzt, um die Trends zu bestätigen und Fehldurchbrüche zu vermeiden. Der RSI misst die Marktstärke anhand der Differenz zwischen schnellen und langsamen Linien, der Längenparameter beträgt 14. Wenn der RSI die 30er-Marke von unten überschreitet, entsteht ein Kaufsignal; unterschreitet er die 70er-Marke von oben, ein Verkaufssignal.

Darüber hinaus nutzt die Strategie den ATR-Indikator, um den Stop-Loss automatisch anzupassen. Der ATR spiegelt die Marktvolatilität wider. Bei zunehmender Volatilität wird der Stop-Loss weiter gesetzt, um die Wahrscheinlichkeit eines vorzeitigen Auslösens zu verringern.

Schließlich wird der ADX-Indikator verwendet, um die Trendstärke zu bewerten. Der ADX leitet die Trendstärke aus der Differenz zwischen dem positiven Richtungsindikator DI+ und dem negativen Richtungsindikator DI- ab. Wenn der ADX die 20er-Marke überschreitet, wird ein Trend als etabliert betrachtet, und erst dann werden tatsächliche Handelssignale generiert.

Durch die Kombination mehrerer Indikatoren wird die Strategie beim Auslösen von Handelssignalen vorsichtiger und vermeidet Fehlsignale im Markt, was zu einer höheren Erfolgsquote führt.

Vorteile der Strategie

Die Strategie bietet folgende Vorteile:

-

Kombination mehrerer Indikatoren zur umfassenden Marktbewertung: Durch die Kombination von gleitenden Durchschnitten, RSI, ATR, ADX und anderen Indikatoren wird die Entscheidungsgenauigkeit verbessert und Fehlurteile aufgrund eines einzelnen Indikators vermieden.

-

Automatische Stop-Loss-Anpassung zur Risikokontrolle: Der Stop-Loss wird an die Marktvolatilität angepasst, um die Wahrscheinlichkeit eines Auslösens zu verringern und das Handelsrisiko effektiv zu kontrollieren.

-

Bewertung der Trendstärke zur Reduzierung von Gegentrendgeschäften: Durch die Bewertung der Trendstärke mit dem ADX, bevor tatsächlich gehandelt wird, können Verluste durch Geschäfte gegen den Trend reduziert werden.

-

Großer Optimierungsspielraum: Parameter wie Längen der gleitenden Durchschnitte, RSI-Länge, ATR-Zeitraum und ADX-Zeitraum können je nach Markt angepasst und optimiert werden, was eine hohe Anpassungsfähigkeit ergibt.

-

Schutz langfristiger Gewinne: Das System aus schnellen und langsamen gleitenden Durchschnitten erkennt langfristige Trends, und mit RSI und anderen Indikatoren werden kurzfristige Störungen reduziert. So können Positionen im Trend langfristig gehalten werden, was höhere Renditen ermöglicht.

Risiken und Gegenmaßnahmen

Die Strategie birgt ebenfalls einige Risiken:

-

Risiko der Parameteroptimierung: Die Vielzahl an Parametern erschwert die Optimierung; ungeeignete Parameterkombinationen können die Strategieleistung verschlechtern. Dieses Risiko kann durch ausreichendes Backtesting und Parameteranpassungen gemindert werden.

-

Risiko des Indikatorversagens: Technische Indikatoren sind nur in bestimmten Marktzuständen geeignet. In außergewöhnlichen Marktsituationen können alle verwendeten Indikatoren gleichzeitig versagen. Das Risiko solcher Black-Swan-Ereignisse ist zu beachten.

-

Risiko von Verlusten bei Leerverkäufen: Die Strategie erlaubt Leerverkäufe. Leerverkäufe bergen das Risiko unbegrenzter Verluste. Dieses Risiko kann durch das Setzen von Stop-Loss verringert werden.

-

Trendwenderisiko: Bei Trendwenden können die Indikatorsignale nicht schnell genug reagieren, was zu Gegentrendverlusten führen kann. Eine Verkürzung einiger Indikatorparameter kann die Sensitivität erhöhen.

Optimierungsmöglichkeiten

Die Strategie bietet noch weiteren Optimierungsspielraum:

-

Adaptive Indikatorgewichte: Durch Analyse der Korrelation zwischen verschiedenen Indikatoren und Marktzuständen könnten dynamisch angepasste Gewichte die Entscheidungsqualität in verschiedenen Marktphasen verbessern.

-

Integration von Deep-Learning-Modellen: Die Verwendung von Deep Learning oder anderen Modellen zur Vorhersage von Preisbewegungen könnte die Entscheidungsregeln ergänzen und die Genauigkeit erhöhen.

-

Automatische Parameteranpassung: Ein auf historischen Daten basierendes automatisches Optimierungsmodul könnte die Indikatorparameter dynamisch anpassen, sodass sich die Strategie besser an Marktveränderungen anpasst.

-

Einbeziehung variabler Zyklen: Die Einbeziehung von Methoden wie der Elliott-Wellen-Theorie könnte die Analyse langfristiger Trends unterstützen und die Wahrscheinlichkeit von Gewinnmitnahmen in Positionen erhöhen.

Zusammenfassung

Diese Strategie kombiniert mehrere Indikatoren wie gleitende Durchschnitte, RSI, ATR und ADX zu einem umfassenden Entscheidungsregelwerk. Sie erkennt sowohl langfristige Trends durch das gleitende Durchschnittssystem als auch kurzfristige Störungen durch RSI und andere kurzfristige Indikatoren. Gleichzeitig bietet die Strategie großes Optimierungspotenzial, um weitere Leistungssteigerungen zu erzielen. Insgesamt verbessert die Strategie durch die Kombination von Indikatoren die Entscheidungsqualität und kontrolliert Risiken – sie ist eine vertiefte Untersuchung und Anwendung wert.

- 1