Bollinger-Bänder + RSI + ADX + ATR Umkehrhandelsstrategie

1

Follow

1802

Followers

Überblick

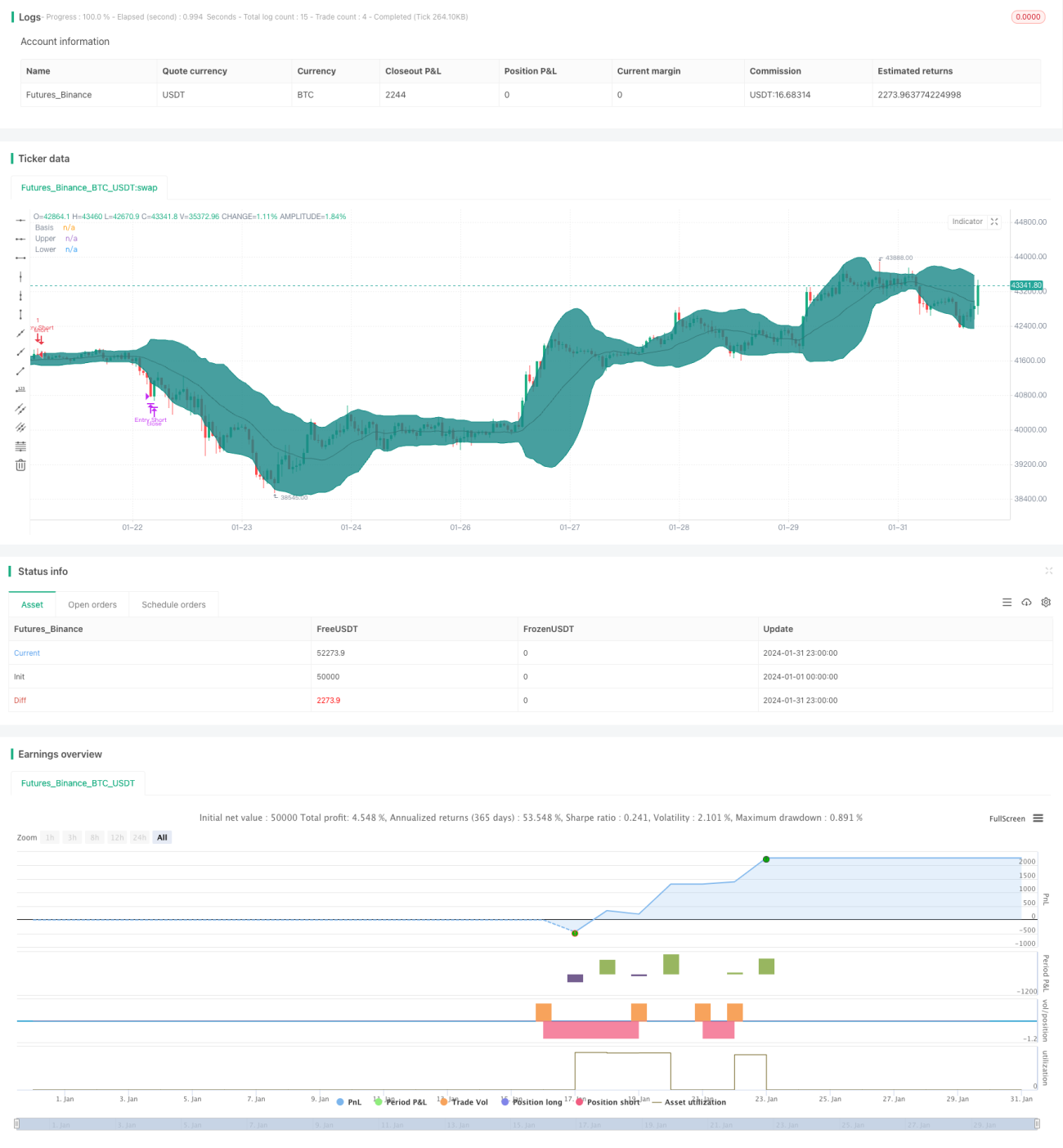

Diese Strategie kombiniert mehrere technische Indikatoren. Wenn das Bollinger-Band ein Signal für eine Preisumkehr ausgibt, werden RSI, ADX und ATR genutzt, um die Marktstruktur zu beurteilen und Umkehrhandelsmöglichkeiten mit hoher Wahrscheinlichkeit zu identifizieren.

Strategieprinzip

- Verwendung eines 20-Perioden-Bollinger-Bands. Wenn der Preis das obere oder untere Band erreicht, wird auf eine Umkehrkerze gewartet, um ein Kauf- oder Verkaufssignal zu generieren.

- Der RSI-Indikator bewertet, ob sich der Markt in einer Seitwärtsphase befindet. Ein RSI über 60 deutet auf einen bullischen Bereich hin, unter 40 auf einen bärischen Bereich.

- Ein ADX unter 20 zeigt einen Seitwärtsmarkt an, über 20 einen trendenden Markt.

- ATR-basierter Stop-Loss und Trailing-Stop.

- Signalfilterung durch einen EMA (Exponentiell gleitender Durchschnitt).

Vorteile der Strategie

- Kombination mehrerer Indikatoren führt zu Handelssignalen mit hoher Wahrscheinlichkeit.

- Anpassbare Parameter für unterschiedliche Marktbedingungen.

- Strenge Stop-Loss-Regeln zur effektiven Risikokontrolle.

Risikoanalyse der Strategie

- Falsche Parametereinstellungen können zu übermäßigem Handel führen.

- Die Wahrscheinlichkeit fehlgeschlagener Umkehrungen besteht weiterhin.

- Der Trailing-Stop könnte in bestimmten Märkten unwirksam sein.

Optimierungsmöglichkeiten

- Testen weiterer Indikatorkombinationen, um geeignetere Parameterkonfigurationen zu finden.

- Nach einem Fehlschlag des Ausbruchs rechtzeitig die Möglichkeit einer fortgesetzten Umkehr erkennen.

- Verschiedene Stop-Loss-Methoden testen, um den Stop intelligenter zu gestalten.

Zusammenfassung

Diese Strategie nutzt das Bollinger-Band als grundlegendes Handelssignal, während mehrere Hilfsindikatoren ein Filter mit hoher Wahrscheinlichkeit bilden. Die Stop-Loss-Regeln sind ebenfalls recht vollständig. Durch Parameteroptimierung und Indikatoranpassung kann die Strategieleistung weiter verbessert werden. Insgesamt bietet diese Strategie ein zuverlässiges System für Umkehrgeschäfte.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1