Triple Supertrend con EMA y ADX

El autor:¿ Qué pasa?, Fecha: 2022-05-08 20:48:42Las etiquetas:El EMAADX

Publicando una estrategia que incluye adx y ema filtro también

Si se aplica un filtro de ADX y EMA, también compruebe si ADX está por encima del nivel seleccionado y el cierre está por encima de EMA Salida: cuando la primera supertendencia se vuelve negativa

opuesto para entradas cortas

Un filtro se da para tomar o evitar la reentrada en el mismo lado. Por ejemplo, después de una salida larga, si la condición de entrada se satisface de nuevo durante mucho tiempo antes de que se active el sencillo corto, se reingresa si se selecciona.

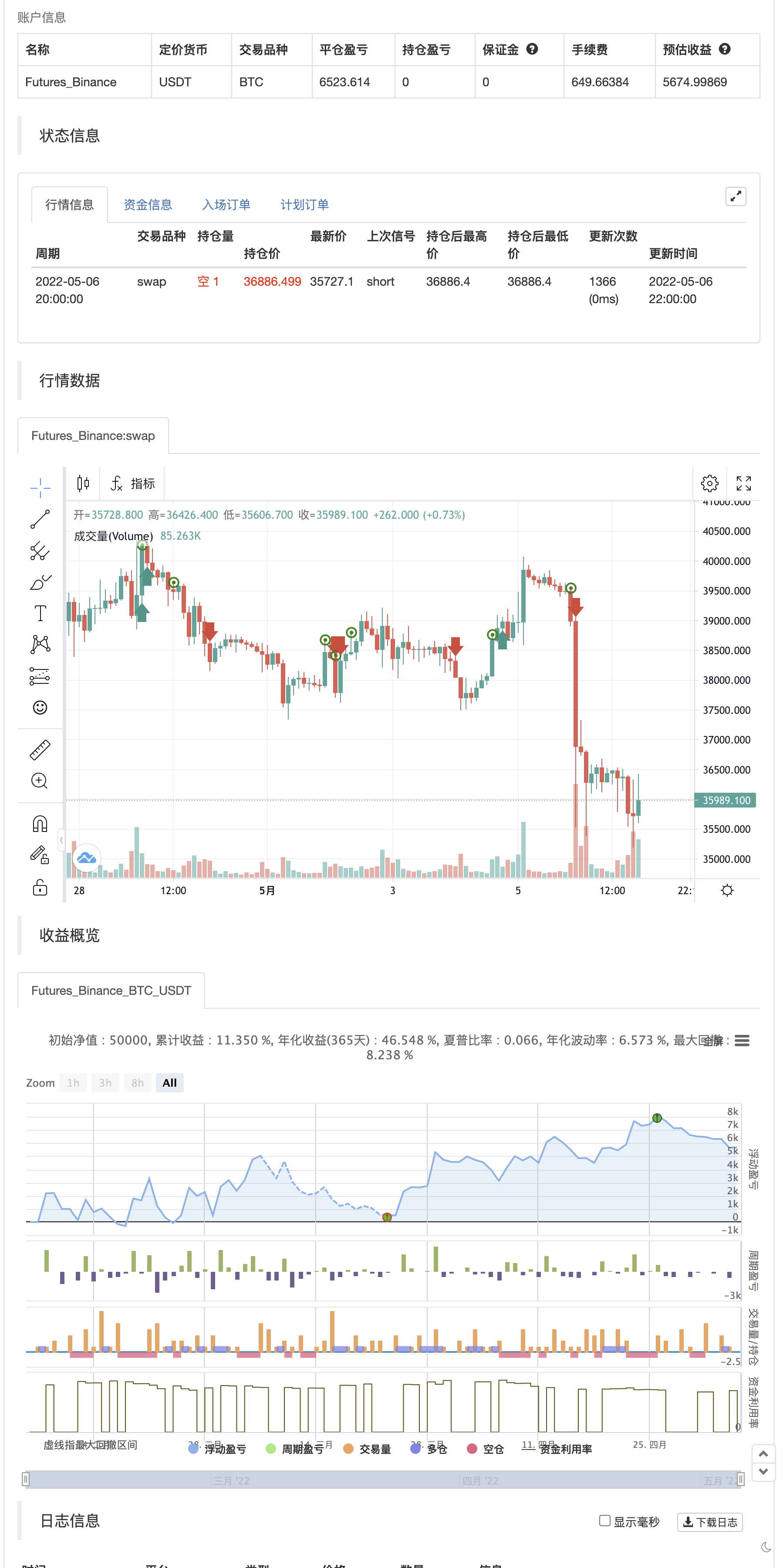

Prueba posterior

/*backtest

start: 2022-02-07 00:00:00

end: 2022-05-07 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// ©kunjandetroja

//@version=5

strategy('Triple Supertrend with EMA and ADX', overlay=true)

m1 = input.float(1,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 1')

m2 = input.float(2,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 2')

m3 = input.float(3,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 3')

p1 = input.int(10,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 1')

p2 = input.int(15,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 2')

p3 = input.int(20,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 3')

len_EMA = input.int(200,"EMA Len",minval = 5,maxval= 250,step=1)

len_ADX = input.int(14,"ADX Len",minval = 1,maxval= 25,step=1)

len_Di = input.int(14,"Di Len",minval = 1,maxval= 25,step=1)

adx_above = input.float(25,"adx filter",minval = 1,maxval= 50,step=0.5)

var bool long_position = false

adx_filter = input.bool(false, "Add Adx & EMA filter")

renetry = input.bool(true, "Allow Reentry")

f_getColor_Resistance(_dir, _color) =>

_dir == 1 and _dir == _dir[1] ? _color : na

f_getColor_Support(_dir, _color) =>

_dir == -1 and _dir == _dir[1] ? _color : na

[superTrend1, dir1] = ta.supertrend(m1, p1)

[superTrend2, dir2] = ta.supertrend(m2, p2)

[superTrend3, dir3] = ta.supertrend(m3, p3)

EMA = ta.ema(close, len_EMA)

[diplus,diminus,adx] = ta.dmi(len_Di,len_ADX)

// ADX Filter

adxup = adx > adx_above and close > EMA

adxdown = adx > adx_above and close < EMA

sum_dir = dir1 + dir2 + dir3

dir_long = if(adx_filter == false)

sum_dir == -3

else

sum_dir == -3 and adxup

dir_short = if(adx_filter == false)

sum_dir == 3

else

sum_dir == 3 and adxdown

Exit_long = dir1 == 1 and dir1 != dir1[1]

Exit_short = dir1 == -1 and dir1 != dir1[1]

// BuySignal = dir_long and dir_long != dir_long[1]

// SellSignal = dir_short and dir_short != dir_short[1]

// if BuySignal

// label.new(bar_index, low, 'Long', style=label.style_label_up)

// if SellSignal

// label.new(bar_index, high, 'Short', style=label.style_label_down)

longenter = if(renetry == false)

dir_long and long_position == false

else

dir_long

shortenter = if(renetry == false)

dir_short and long_position == true

else

dir_short

if longenter

long_position := true

if shortenter

long_position := false

strategy.entry('BUY', strategy.long, when=longenter)

strategy.entry('SELL', strategy.short, when=shortenter)

strategy.close('BUY', Exit_long)

strategy.close('SELL', Exit_short)

//buy1 = ta.barssince(dir_long)

//sell1 = ta.barssince(dir_short)

//colR1 = f_getColor_Resistance(dir1, color.red)

//colS1 = f_getColor_Support(dir1, color.green)

//colR2 = f_getColor_Resistance(dir2, color.orange)

//colS2 = f_getColor_Support(dir2, color.yellow)

//colR3 = f_getColor_Resistance(dir3, color.blue)

//colS3 = f_getColor_Support(dir3, color.maroon)

//plot(superTrend1, 'R1', colR1, linewidth=2)

//plot(superTrend1, 'S1', colS1, linewidth=2)

//plot(superTrend2, 'R1', colR2, linewidth=2)

//plot(superTrend2, 'S1', colS2, linewidth=2)

//plot(superTrend3, 'R1', colR3, linewidth=2)

//plot(superTrend3, 'S1', colS3, linewidth=2)

// // Intraday only

// var int new_day = na

// var int new_month = na

// var int new_year = na

// var int close_trades_after_time_of_day = na

// if dayofmonth != dayofmonth[1]

// new_day := dayofmonth

// if month != month[1]

// new_month := month

// if year != year[1]

// new_year := year

// close_trades_after_time_of_day := timestamp(new_year,new_month,new_day,15,15)

// strategy.close_all(time > close_trades_after_time_of_day)

Relacionados

- Estrategia de media móvil doble GM-8 y ADX

- VuManChu Cifrado B + Divergencias Estrategia

- Estrategia de cuadrícula de posición variable basada en la tendencia

- El valor de las operaciones de venta de valores de mercado se calculará en función de las operaciones de venta de valores.

- VWMA-ADX Momentum y estrategia larga de Bitcoin basada en tendencias

- Estrategia dinámica de DCA basada en el volumen

- Teoría de las ondas de Elliott 4-9 Detección automática de ondas de impulso Estrategia de negociación

- El valor de las operaciones de mercado se calcula a partir de la media móvil de la EMA/SMA.

- el comercio en marcos de tiempo múltiples

- el valor de las emisiones de gases de efecto invernadero es el valor de las emisiones

Más.

- Estrategia de captura de tendencias de bandas de EMA + leledc + bandas de Bollinger

- Las operaciones de las entidades de crédito se clasifican en el modelo de referencia.

- Estrategia MACD Willy

- RSI - Señales de compra y venta

- Tendencia de Heikin-Ashi

- HA Parcialidad del mercado

- Oscilador suave de la nube de Ichimoku

- Williams %R - Limpiado

- QQE MOD + SSL híbrido + Waddah Attar explosión

- Comprar y vender Strat

- Tom DeMark Mapa de calor secuencial

- jma + dwma por multigranos

- El MACD mágico

- Puntuación Z con señales

- La estrategia de fluctuación fácil de Shinobi en la versión en lengua de Pine

- 3EMA + Boullinger + el eje central

- Baguetas de granos

- La máquina de moler

- Indicador de inversión de K I

- Las velas engullentes