Estrategia cuantitativa de seguimiento de tendencia basada en SAR

Resumen

La estrategia de la Brecha Especulativa es una estrategia de trading cuantitativo que sigue la tendencia. Utiliza la curva suavizada de SAR como señal principal de trading, complementada con múltiples filtros como EMA, Momentum de Squeeze y Oscilador de Volatilidad. Al configurar los parámetros del SAR, identifica los puntos de reversión de la tendencia, logrando un seguimiento de tendencia de bajo riesgo. Esta estrategia es muy adecuada para inversiones a medio y largo plazo.

Principio de la Estrategia

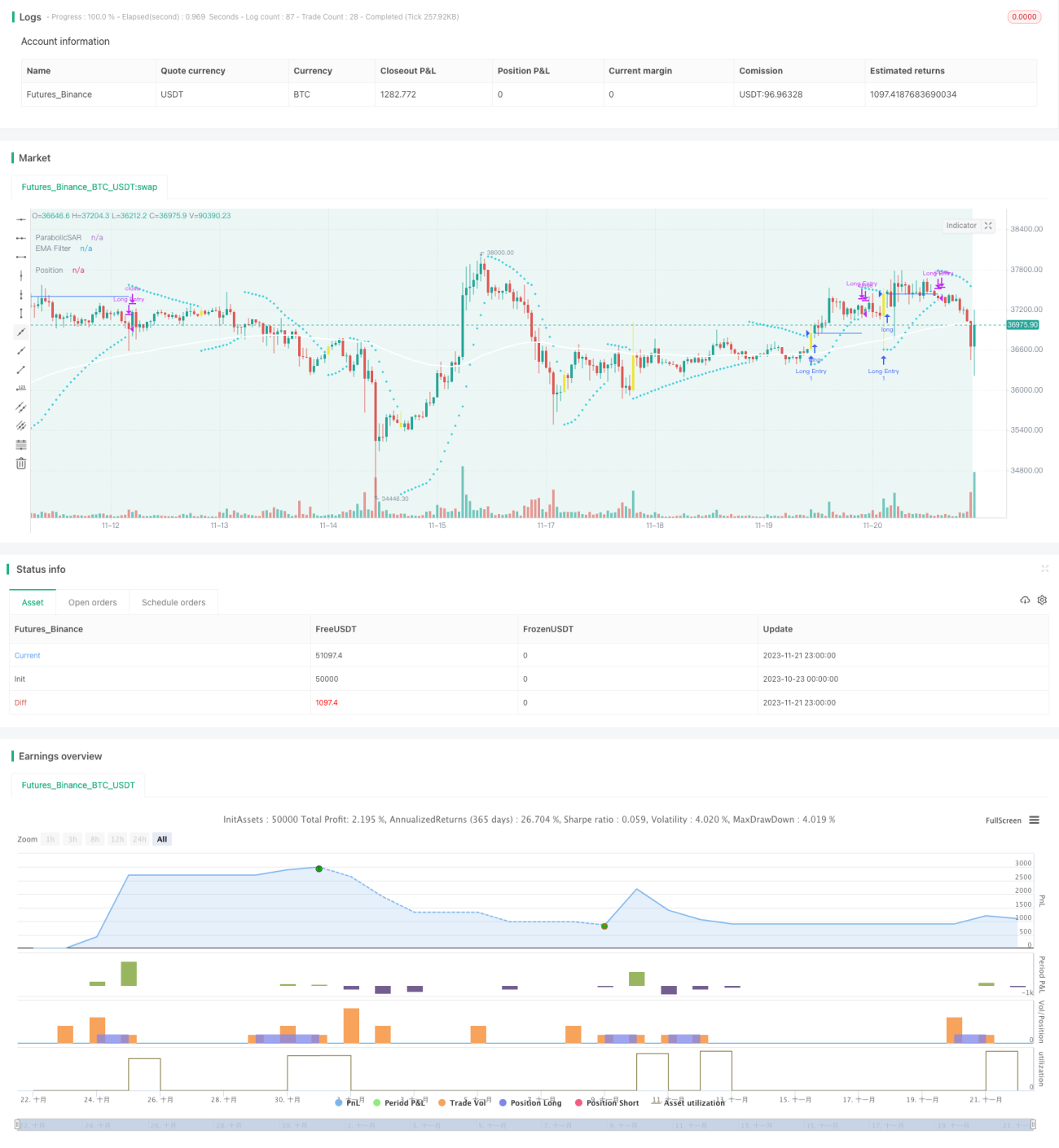

La estrategia utiliza el SAR parabólico como indicador principal de señal de trading. El SAR puede determinar eficazmente los puntos de reversión de la tendencia del precio. Cuando el signo del SAR cambia, significa que la tendencia ha girado. Esta estrategia generalmente emite señales de compra o venta cuando el SAR se invierte.

Además, la estrategia también ofrece la opción de ruptura del SAR. Es decir, antes de que el SAR se haya invertido por completo, si el precio ya ha superado el último valor del SAR, se genera una señal. Esto puede mejorar aún más la sensibilidad de la estrategia.

Para filtrar señales falsas, la estrategia incorpora tres filtros auxiliares: EMA, Momentum de Squeeze y Oscilador de Volatilidad. Se pueden usar individualmente o en combinación para confirmar la tendencia del precio y la fiabilidad de las señales de trading.

Finalmente, la estrategia ofrece tres métodos de stop loss y take profit: stop loss fijo, take profit fijo y stop loss basado en la relación riesgo-recompensa. Esto permite que la estrategia se adapte de manera flexible a las características de diferentes tipos de instrumentos de trading.

Análisis de Ventajas

-

El SAR puede determinar con precisión las reversiones de la tendencia del precio y capturar rápidamente las nuevas tendencias, siendo adecuado para el seguimiento de tendencias a medio y largo plazo.

-

La configuración de múltiples filtros reduce la probabilidad de falsas rupturas y mejora la fiabilidad de las señales.

-

Configuración simple y flexible, con parámetros personalizables para adaptarse a diferentes instrumentos de trading.

-

Ofrece múltiples métodos de take profit y stop loss, permitiendo buscar un equilibrio entre riesgo y recompensa.

-

Se puede conectar directamente a robots de trading para lograr una automatización completa.

Análisis de Riesgos

-

En mercados sin tendencia, pueden aparecer más señales falsas y operaciones ineficaces.

-

Una configuración inadecuada de los parámetros del SAR también puede afectar la precisión en la identificación de señales.

-

Como estrategia de seguimiento de tendencia, en mercados con fuertes oscilaciones laterales es fácil alcanzar el nivel de stop loss.

Para mitigar los riesgos anteriores, se pueden ajustar adecuadamente los parámetros del SAR o los parámetros de los filtros para reducir la probabilidad de operaciones ineficaces. También se puede ampliar adecuadamente el límite de stop loss para soportar mayores fluctuaciones del mercado.

Direcciones de Optimización

-

Optimización de parámetros del SAR. Se pueden optimizar los parámetros de paso y aceleración del SAR mediante datos históricos de backtesting para obtener una estrategia de trading más estable y eficiente.

-

Incorporación de indicadores de juicio de tendencia. Agregar indicadores auxiliares como MACD o DMI para mejorar la capacidad de identificación de tendencias.

-

Optimización de la relación riesgo-recompensa. Ajustar los porcentajes fijos de take profit y stop loss, así como el coeficiente de la relación riesgo-recompensa, para asumir un riesgo mayor adecuadamente y obtener mayores rendimientos.

-

Adición de instrumentos Forex. Actualmente, la estrategia solo admite trading de criptomonedas; se puede ampliar para admitir instrumentos de Forex, materias primas y mercados de valores.

Conclusión

La Brecha Especulativa es una estrategia cuantitativa muy práctica para seguir tendencias. Responde con sensibilidad, las señales son fiables, y mediante la gestión de stop loss y take profit se pueden obtener ganancias estables a largo plazo. La optimización adecuada de parámetros y reglas puede mejorar aún más la eficiencia de la estrategia. Es una estrategia cuantitativa eficiente que merece ser utilizada a largo plazo.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1