Estrategia de Combinación de Medias Móviles con Doble Inversión de Tendencia

Resumen

Esta estrategia es una combinación de doble inversión de tendencia con medias móviles. Combina la estrategia de inversión 123 y la estrategia de medias móviles de Bill Williams, utilizando las señales de ambas estrategias para obtener señales de trading más precisas.

Principio de la estrategia

La estrategia consta de dos partes:

-

Estrategia de inversión 123: Cuando el precio de cierre es superior al del día anterior durante dos días consecutivos y la línea K lenta de 9 períodos está por debajo de 50, se abre una posición larga. Cuando el precio de cierre es inferior al del día anterior durante dos días consecutivos y la línea K rápida de 9 períodos está por encima de 50, se abre una posición corta.

-

Estrategia de medias móviles de Bill Williams: Calcula las medias móviles del precio medio a 13, 8 y 5 períodos. Cuando la media móvil de corto plazo cruza por encima de la media de medio y largo plazo, se abre una posición larga. Cuando la media móvil de corto plazo cruza por debajo de la media de medio y largo plazo, se abre una posición corta.

Finalmente, si las señales de ambas estrategias son consistentes, se genera una señal de trading real; si no lo son, no se opera.

Análisis de ventajas

Esta estrategia combina dos juicios de tendencia, lo que puede reducir las señales falsas y mejorar la precisión de las señales. Además, la inclusión de medias móviles ayuda a filtrar parte del ruido.

Análisis de riesgos

La estrategia presenta los siguientes riesgos:

- El doble filtrado de señales puede llevar a perder buenas oportunidades de trading.

- Una configuración inadecuada de las medias móviles puede malinterpretar la tendencia del mercado.

- La estrategia de inversión en sí misma conlleva riesgo de pérdidas.

Se puede reducir el riesgo ajustando los parámetros de las medias móviles u optimizando la lógica de entrada y salida.

Direcciones de optimización

La estrategia se puede optimizar en los siguientes aspectos:

- Probar diferentes combinaciones de medias móviles para encontrar los parámetros óptimos.

- Agregar una estrategia de stop loss para evitar grandes pérdidas.

- Combinar indicadores de volumen para identificar la calidad de las señales.

- Utilizar métodos de aprendizaje automático para optimizar los parámetros automáticamente.

Conclusión

Esta estrategia integra un doble juicio de tendencia con indicadores de medias móviles, lo que permite filtrar eficazmente las señales de ruido y mejorar la precisión en la toma de decisiones de trading. Sin embargo, también conlleva ciertos riesgos, por lo que es necesario realizar pruebas continuas y optimizar la lógica de entrada y salida para lograr ganancias estables en el trading en vivo.

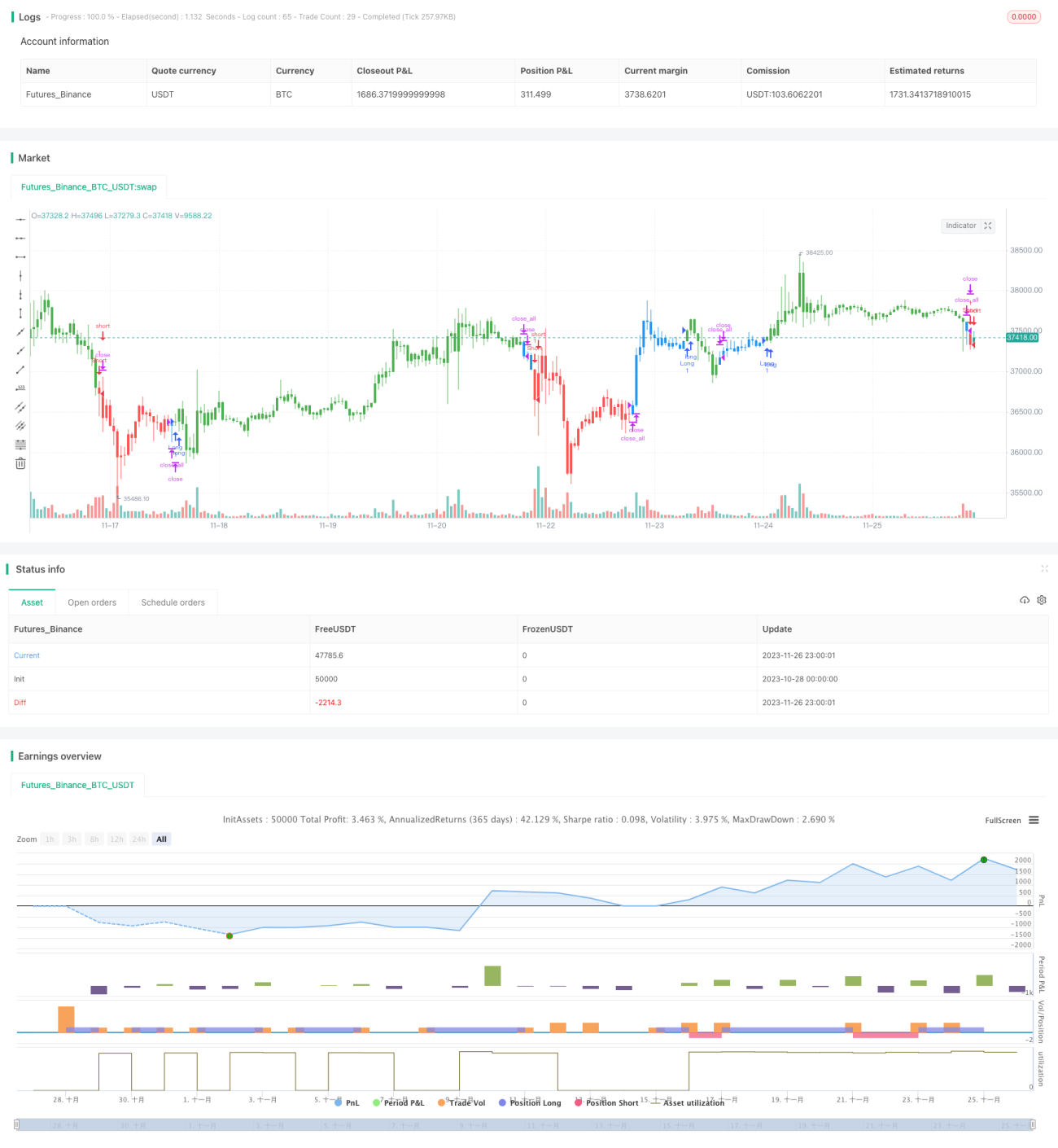

/*backtest

start: 2023-10-28 00:00:00

end: 2023-11-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/06/2019

// This is combo strategies for get - 1