Estrategia de momentum y reversión basada en modelo multifactorial

Resumen

La estrategia de reversión de impulso del modelo multifactorial combina un modelo multifactorial con una estrategia de reversión de impulso para lograr rendimientos más estables y mayores. Esta estrategia utiliza la reversión 123 y el indicador de respuesta conjunta como dos señales independientes, y abre posiciones cuando ambas señales coinciden.

Principio de la estrategia

La estrategia de reversión de impulso del modelo multifactorial se compone de dos subestrategias: la estrategia de reversión 123 y la estrategia del indicador de respuesta conjunta.

La estrategia de reversión 123 se basa en que el precio suba o baje durante 2 días consecutivos, combinada con el indicador STOCH para determinar si el mercado está sobrecomprado o sobrevendido y generar señales de trading. Específicamente, cuando el precio sube durante 2 días consecutivos y la línea lenta del STOCH de 9 días está por debajo de 50, se genera una señal alcista; cuando el precio baja durante 2 días consecutivos y la línea rápida del STOCH de 9 días está por encima de 50, se genera una señal bajista.

La estrategia del indicador de respuesta conjunta utiliza la superposición de medias móviles de diferentes períodos e indicadores osciladores para determinar la dirección y la fuerza de la tendencia. Incluye métodos como ponderación lineal y suma sinusoidal para evaluar de manera integral la situación alcista o bajista. Este indicador se clasifica en niveles, devolviendo de 1 a 9 para indicar una fuerte tendencia alcista, y de -1 a -9 para una fuerte tendencia bajista.

Finalmente, la estrategia selecciona abrir una posición larga o corta cuando ambas señales coinciden.

Análisis de ventajas

La estrategia de reversión de impulso del modelo multifactorial combina el factor de reversión y el factor de impulso, lo que permite capturar oportunidades de reversión mientras se sigue la tendencia, evitando falsas rupturas y logrando así una mayor tasa de acierto. Las ventajas específicas son:

-

La estrategia de reversión 123, como fuente de señales de reversión, puede capturar ganancias extraordinarias de las reversiones a corto plazo.

-

El indicador de respuesta conjunta determina la dirección y la fuerza de la tendencia, evitando el riesgo de pérdidas causadas por un margen de reversión demasiado grande.

-

La combinación de ambos complementa sus ventajas y compensa sus deficiencias hasta cierto punto, mejorando la calidad de las señales.

-

En comparación con un modelo único, la combinación de múltiples factores puede mejorar la estabilidad de la estrategia.

Análisis de riesgos

Aunque la estrategia de reversión de impulso del modelo multifactorial tiene ciertas ventajas, todavía presenta los siguientes riesgos:

-

La reversión no se completa y el precio vuelve a caer, lo que provoca pérdidas. Se puede ajustar adecuadamente el stop loss para prevenirlo.

-

Cuando las dos señales no coinciden, no se puede determinar la dirección. Se puede ajustar los parámetros para que tengan una mayor concordancia.

-

El modelo es demasiado complejo, con muchos parámetros, lo que dificulta su ajuste y optimización.

-

Es necesario prestar atención a múltiples submodelos al mismo tiempo, lo que aumenta la dificultad operativa en tiempo real y la presión psicológica. Se puede introducir cierto grado de automatización para aliviar la carga operativa.

Direcciones de optimización

La estrategia de reversión de impulso del modelo multifactorial se puede optimizar en los siguientes aspectos:

-

Ajustar los parámetros de la estrategia de reversión 123 para que las señales de reversión sean más precisas y fiables.

-

Ajustar los parámetros del indicador de respuesta conjunta para que la tendencia juzgada se acerque más a la tendencia real.

-

Introducir algoritmos de aprendizaje automático para optimizar automáticamente las combinaciones de parámetros.

-

Agregar un módulo de gestión de posiciones para que los ajustes de posición sean más cuantitativos y sistemáticos.

-

Agregar un módulo de stop loss para controlar eficazmente las pérdidas individuales mediante el establecimiento previo de un precio de stop loss.

Conclusión

La estrategia de reversión de impulso del modelo multifactorial utiliza de manera integral el factor de reversión y el factor de impulso. Sobre la base de garantizar una alta calidad de las señales, logra una mayor tasa de acierto mediante la superposición de múltiples factores. Esta estrategia tiene la doble ventaja de capturar oportunidades de reversión y seguir la tendencia, y es una estrategia cuantitativa eficiente y estable. En el futuro, se puede optimizar continuamente desde aspectos como el ajuste de parámetros y el control de riesgos para mejorar aún más la relación riesgo-rendimiento de la estrategia.

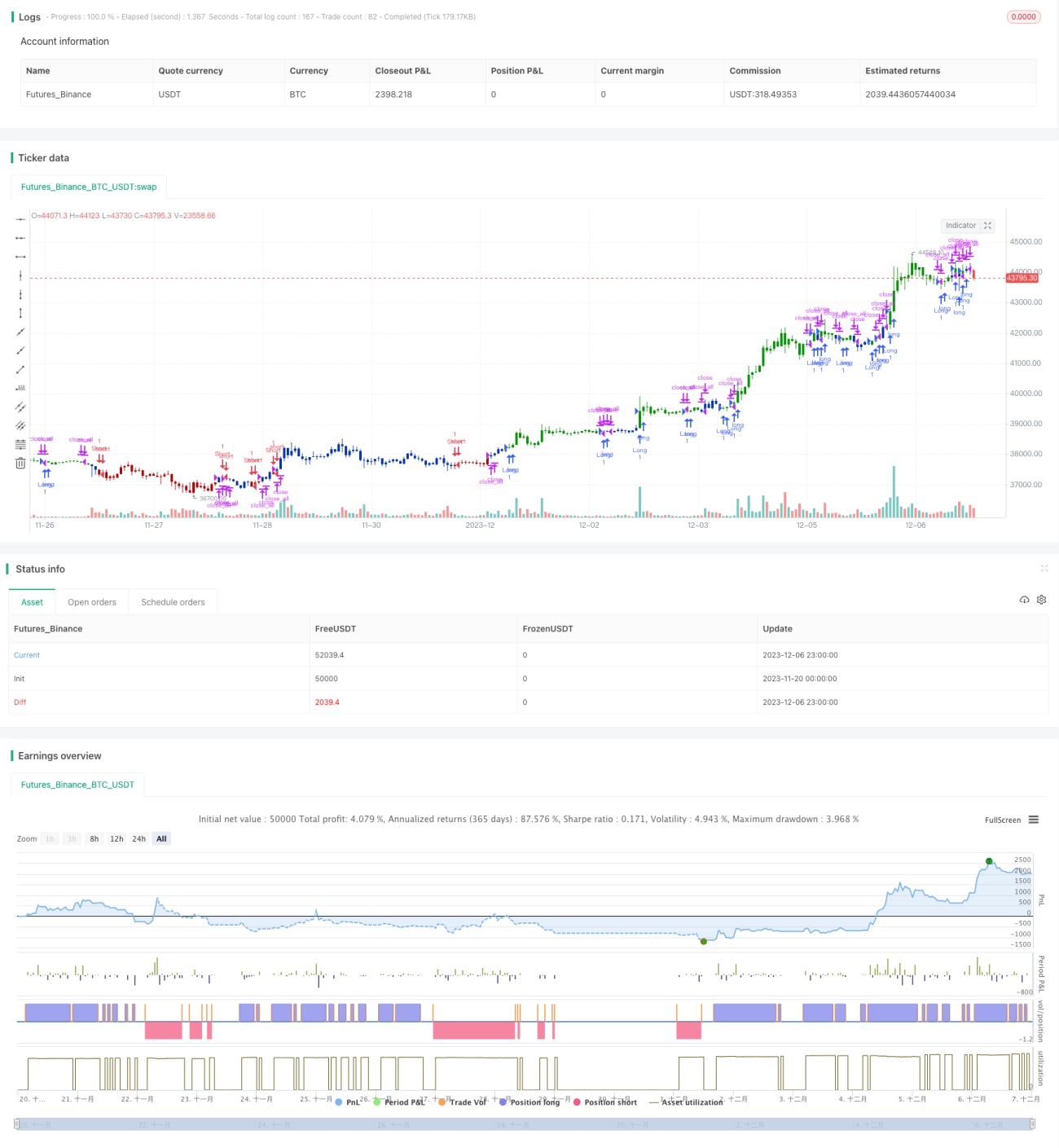

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 11/11/2019

// This is combo strategies for get a cumulative signal. - 1