Estrategia de trading cuantitativo que combina tendencia y oscilación

Resumen

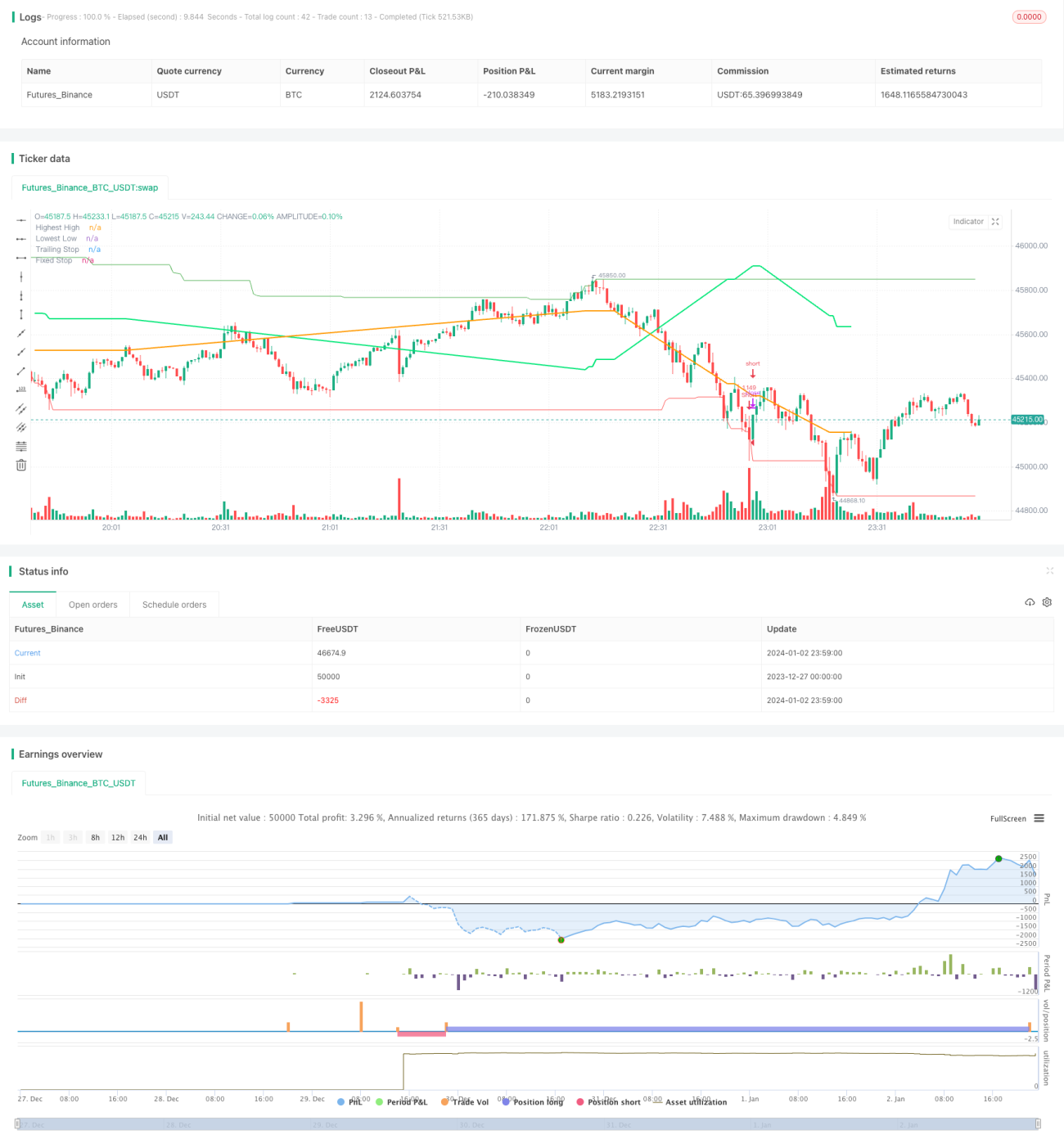

La estrategia de doble tendencia con oscilador es una estrategia de trading cuantitativo que combina tendencia y oscilación. Utiliza la combinación de dos indicadores para identificar la dirección y la fuerza de la tendencia, y busca mejores momentos de entrada durante las oscilaciones de la tendencia.

Principio de la estrategia

Esta estrategia utiliza principalmente dos indicadores públicos: Trend Surfers y Mawreez's Trend Oscillator.

Trend Surfers es un indicador de trailing stop de tendencia. Calcula los precios máximos y mínimos durante un período determinado para determinar la dirección del precio y proporcionar niveles de stop sugeridos. Por ejemplo, cuando el precio supera el máximo de las últimas 168 velas, es una señal alcista; cuando el precio cae por debajo del mínimo de las últimas 168 velas, es una señal bajista.

Mawreez's Trend Oscillator es un indicador oscilador de dos líneas. Similar al MACD, utiliza la diferencia de DI para determinar la dirección y la fuerza de la tendencia. Cuando la curva del indicador está por encima de la línea cero, es alcista; por debajo, es bajista.

Las reglas de trading de la estrategia son:

- Entrada larga: cuando Trend Surfers supera la línea máxima y el indicador Mawreez's Trend Oscillator es alcista.

- Entrada corta: cuando Trend Surfers cae por debajo de la línea mínima y el indicador Mawreez's Trend Oscillator es bajista.

El stop loss se compone de un trailing stop de tendencia más un stop loss fijo.

Análisis de ventajas

Esta estrategia combina indicadores de tendencia y oscilación, lo que permite capturar tendencias y también encontrar mejores precios de entrada en oscilaciones. Sus ventajas son:

- Doble filtro de indicadores, que evita eficazmente las falsas rupturas.

- Al combinar tendencia y oscilación, es fácil aprovechar las zonas de acumulación en rangos de oscilación para posiciones largas o aligerar posiciones en techos.

- Múltiples métodos de stop loss permiten un buen control del riesgo.

Análisis de riesgos

La estrategia también presenta algunos riesgos:

- La combinación de dos indicadores puede generar omisiones de señales.

- Los indicadores de tendencia y oscilación pueden emitir señales conflictivas.

- El stop loss fijo puede activarse prematuramente.

Para mitigar estos riesgos, se pueden adoptar las siguientes medidas:

- Ajustar los parámetros de los indicadores para hacerlos más flexibles y reducir la tasa de filtrado.

- Agregar reglas de confirmación de tendencia para evitar conflictos entre indicadores.

- Ajustar dinámicamente los niveles de stop loss.

Direcciones de optimización

La estrategia tiene margen para una mayor optimización:

- Probar diferentes combinaciones de parámetros y períodos para encontrar los valores óptimos.

- Agregar reglas auxiliares como volatilidad, volumen de operaciones, etc.

- Utilizar técnicas de aprendizaje automático para optimizar dinámicamente los indicadores y parámetros.

Conclusión

La estrategia de doble tendencia con oscilador aprovecha las ventajas de los indicadores de seguimiento de tendencia y oscilación, permitiendo identificar la dirección de la tendencia y aprovechar las oportunidades de oscilación. Mediante la optimización de parámetros y reglas, se puede mejorar aún más su rentabilidad. Esta estrategia tiene buenas perspectivas de desarrollo.

- 1