Estrategia de trading de rango con soporte y resistencia

Resumen

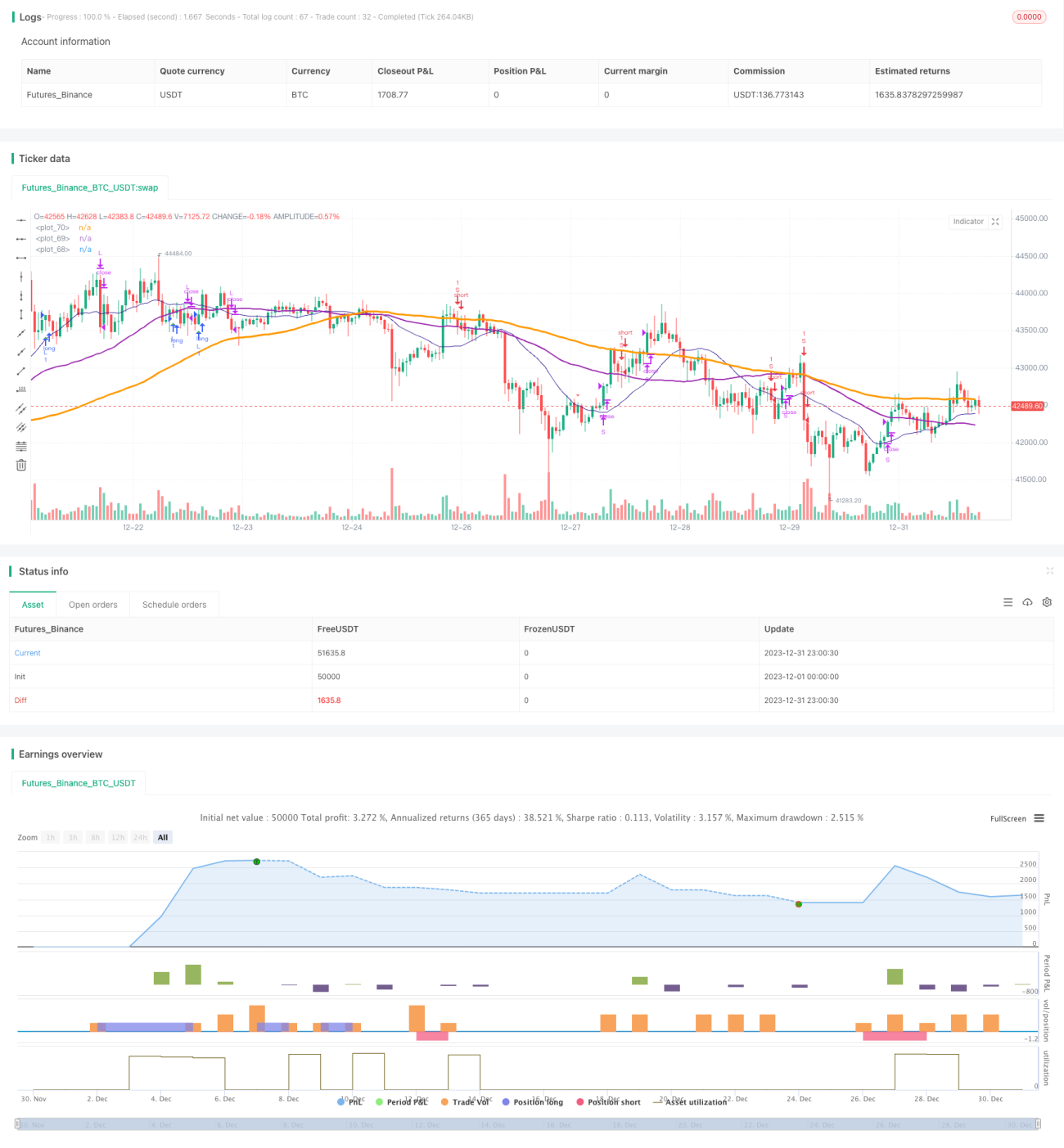

Esta estrategia combina la intersección de los indicadores RSI y estocástico, junto con una estrategia de optimización de deslizamiento al cierre, logrando un control preciso de la lógica de trading y un stop-loss/take-profit exacto. Además, mediante la introducción de optimización de señales, se puede controlar mejor la tendencia, logrando una gestión razonable de los fondos.

Principio de la Estrategia

- El indicador RSI determina zonas de sobrecompra/sobreventa, combinado con el cruce de las líneas K y D del indicador estocástico para generar señales de trading.

- Se introduce el reconocimiento de la formación de velas (fractales) para ayudar a identificar señales de tendencia y evitar operaciones erróneas.

- La media móvil SMA ayuda a determinar la dirección de la tendencia. Cuando la media móvil a corto plazo cruza por encima de la media a largo plazo, es una señal alcista.

- Estrategia de deslizamiento al cierre: se establecen precios de stop-loss y take-profit basados en el rango de fluctuación entre el máximo y el mínimo.

Análisis de Ventajas

- Los parámetros optimizados del RSI permiten una buena identificación de zonas de sobrecompra/sobreventa, evitando operaciones erróneas.

- Los parámetros optimizados del STO (suavizado) filtran el ruido y mejoran la calidad de la señal.

- Se introduce el análisis técnico Heikin-Ashi para identificar cambios en la dirección del cuerpo de las velas, asegurando la precisión de las señales.

- La media móvil SMA ayuda a determinar la tendencia general, evitando operar en contra de la tendencia.

- La combinación con una estrategia de deslizamiento en stop-loss/take-profit permite maximizar las ganancias de cada operación.

Análisis de Riesgos

- En caídas sostenidas del mercado general, los fondos enfrentan un riesgo considerable.

- La frecuencia de trading podría ser excesiva, aumentando los costos de comisión y deslizamiento.

- El indicador RSI puede generar señales falsas, por lo que debe combinarse con otros indicadores para filtrar.

Optimización de la Estrategia

- Ajustar los parámetros del RSI para optimizar la detección de sobrecompra/sobreventa.

- Ajustar los parámetros del STO (suavizado y período) para mejorar la calidad de la señal.

- Ajustar los períodos de las medias móviles para optimizar la identificación de tendencias.

- Introducir más indicadores técnicos para mejorar la precisión de las señales.

- Optimizar la relación stop-loss/take-profit para reducir el riesgo por operación.

Resumen

Esta estrategia integra las ventajas de varios indicadores técnicos principales. Mediante la optimización de parámetros y el perfeccionamiento de las reglas, logra un equilibrio entre la calidad de las señales de trading y el stop-loss/take-profit. Posee cierta universalidad y capacidad de generar ganancias estables. Con una optimización continua, se puede mejorar aún más la tasa de aciertos y la rentabilidad.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)- 1