Estrategia de trading ADX bidireccional

Resumen

La estrategia de trading bidireccional con ADX es una estrategia cuantitativa que utiliza el indicador de Índice de Movimiento Direccional Promedio (ADX) para realizar operaciones en ambas direcciones. Esta estrategia calcula la diferencia entre el indicador ADX y los indicadores DIPlus y DIMinus, establece un umbral para determinar si se genera una señal de trading, y realiza operaciones largas y cortas para obtener ganancias.

Principio de la Estrategia

- Calcular el Rango Verdadero (True Range)

- Calcular el Movimiento Direccional Positivo (Directional Movement Plus) y el Movimiento Direccional Negativo (Directional Movement Minus)

- Calcular el Rango Verdadero Suavizado (Smoothed True Range)

- Calcular el Movimiento Direccional Positivo Suavizado (Smoothed Directional Movement Plus) y el Movimiento Direccional Negativo Suavizado (Smoothed Directional Movement Minus)

- Calcular los indicadores DIPlus, DIMinus y ADX

- Calcular la diferencia entre DIPlus y ADX, y entre DIMinus y ADX

- Establecer umbrales de diferencia para operaciones largas y cortas

- Cuando la diferencia supera el umbral, se determina que se genera una señal de trading

- Generar órdenes de compra y venta

El núcleo de esta estrategia reside en utilizar indicadores de movimiento direccional como el ADX para determinar la dirección y fuerza de la tendencia, combinados con la regla de determinación de diferencias para establecer umbrales y realizar trading automático.

Análisis de Ventajas

- Utilizar el ADX para determinar la dirección de la tendencia permite capturar con precisión las tendencias del mercado.

- Aplicar la regla de determinación de diferencias filtra eficazmente las señales falsas.

- El trading bidireccional permite aprovechar plenamente las oportunidades tanto en largo como en corto.

- Trading totalmente automatizado sin intervención manual.

- La lógica de la estrategia es clara, fácil de entender y modificar.

Análisis de Riesgos

- El indicador ADX tiene un rezago, lo que podría hacer que se pierdan puntos de inflexión de la tendencia.

- El trading bidireccional aumenta el riesgo, y las pérdidas podrían ampliarse.

- Parámetros mal configurados pueden provocar un exceso de operaciones.

- Los datos de backtesting no pueden representar el mercado real, por lo que el riesgo en operaciones en vivo sigue existiendo.

Soluciones:

- Combinar con otros indicadores para confirmar las señales de trading.

- Optimizar parámetros para controlar la frecuencia de las operaciones.

- Gestionar estrictamente el tamaño de las posiciones (Position Sizing) para controlar los lotes de trading.

Direcciones de Optimización

- Optimizar los parámetros del ADX para mejorar su sensibilidad.

- Agregar otros indicadores para filtrar señales.

- Aplicar algoritmos de aprendizaje automático para optimizar los parámetros.

- Utilizar estrategias avanzadas de stop-loss para controlar el riesgo de pérdidas.

- Combinar predicciones de modelos para obtener señales de trading más precisas.

Resumen

La estrategia de trading bidireccional con ADX es, en general, una estrategia cuantitativa muy práctica. Utiliza el indicador ADX para determinar la tendencia y capturar oportunidades de trading en ambas direcciones. Al mismo tiempo, aplica la determinación de diferencias para garantizar la validez de las señales. La lógica de la estrategia es clara y simple, fácil de modificar y optimizar, siendo una estrategia de seguimiento de tendencias bidireccional. Mediante una optimización razonable de parámetros, la aplicación de estrategias de stop-loss y el filtrado de señales, se puede mejorar aún más la estabilidad y rentabilidad de la estrategia.

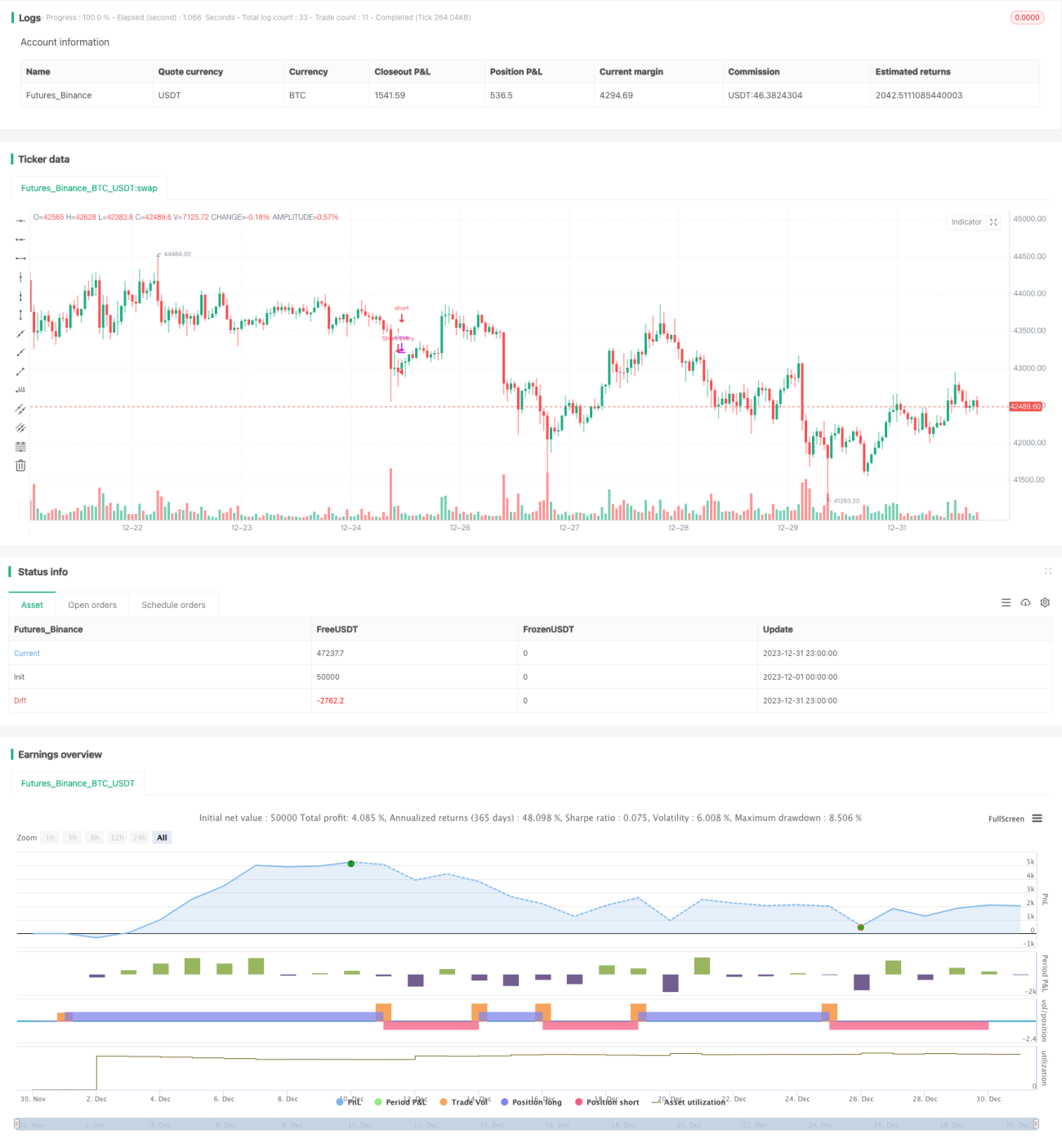

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1