Estrategia de negociación con medias móviles dobles en marcos temporales cruzados

Resumen

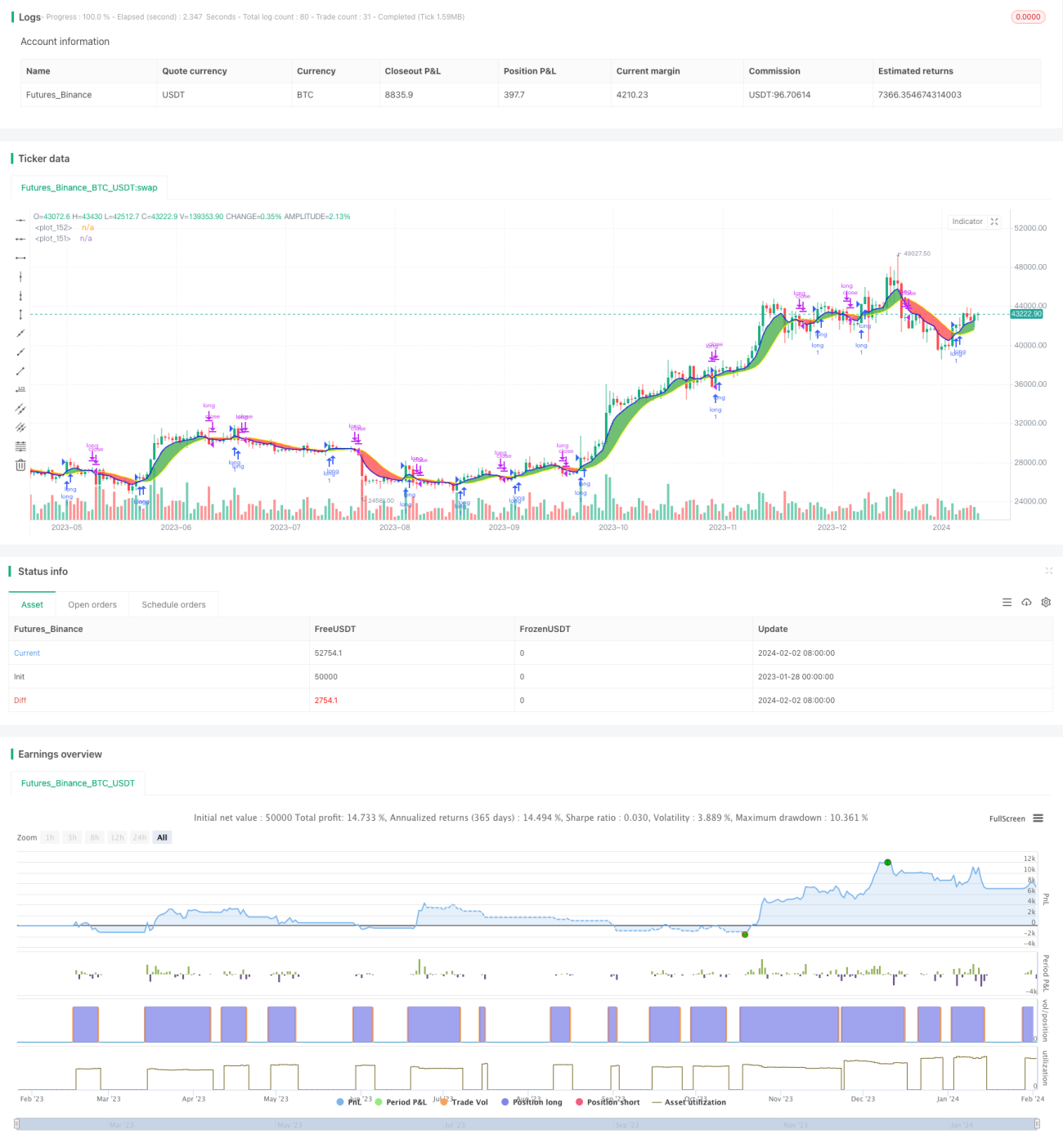

Esta estrategia genera señales de compra y venta en dos marcos de tiempo diferentes mediante el cálculo de dos tipos distintos de medias móviles. Es una excelente estrategia sandbox para experimentar con diferentes tipos de medias móviles y combinaciones de marcos de tiempo.

Principio de la Estrategia

La estrategia utiliza dos medias móviles: una rápida y una lenta. El marco de tiempo de la media móvil rápida debe ser mayor o igual al del gráfico. Cuando la media móvil rápida cruza al alza la media móvil lenta, se genera una señal de compra; cuando la cruza a la baja, se genera una señal de venta.

El usuario puede elegir entre varios tipos de medias móviles, como SMA, EMA, KAMA, etc., y los marcos de tiempo pueden ser diferentes, lo que permite experimentar con combinaciones para encontrar los parámetros óptimos.

Análisis de Ventajas

La mayor ventaja de esta estrategia es que permite ajustar parámetros de manera muy conveniente para experimentar con diferentes combinaciones y encontrar la configuración óptima.

El usuario puede seleccionar libremente el tipo, la longitud temporal y el marco de tiempo de las dos medias móviles, y el sistema calculará y mostrará los resultados en tiempo real. Esto es mucho más fácil que probar combinaciones de parámetros una por una.

Además, la estrategia incorpora funciones de stop-loss y take-profit, lo que reduce el riesgo y aumenta la probabilidad de ganancias.

Análisis de Riesgos

El mayor riesgo de esta estrategia es que una configuración inadecuada de parámetros puede generar señales de trading demasiado frecuentes, aumentando así los costos de transacción y las pérdidas por deslizamiento.

Además, el cruce de dos medias móviles es propenso a generar señales falsas. Si los parámetros no se eligen correctamente, las señales de compra y venta pueden no ser fiables.

Estos riesgos pueden mitigarse optimizando los parámetros o combinando la estrategia con otros indicadores.

Direcciones de Optimización

Se puede considerar agregar otros indicadores para filtrar las señales basadas en el cruce de dos medias móviles, por ejemplo, utilizando el RSI para confirmar las señales de compra y venta, reduciendo así las señales falsas.

También se puede intentar entrenar y optimizar los parámetros de las medias móviles para encontrar la mejor combinación. Otra posibilidad es utilizar métodos de aprendizaje automático para optimizar dinámicamente los parámetros.

Resumen

Esta estrategia es un excelente sandbox experimental para el cruce de dos medias móviles. Su ventaja radica en la rápida iteración de diferentes combinaciones de parámetros para encontrar la mejor estrategia de trading. Por supuesto, existen riesgos asociados a una configuración inadecuada de parámetros, que pueden reducirse agregando otros indicadores de filtro. Si se continúa optimizando esta estrategia, es probable que se obtengan mejores resultados de trading.

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.- 1