Estrategia de tendencia de engulfing dinámico

Resumen

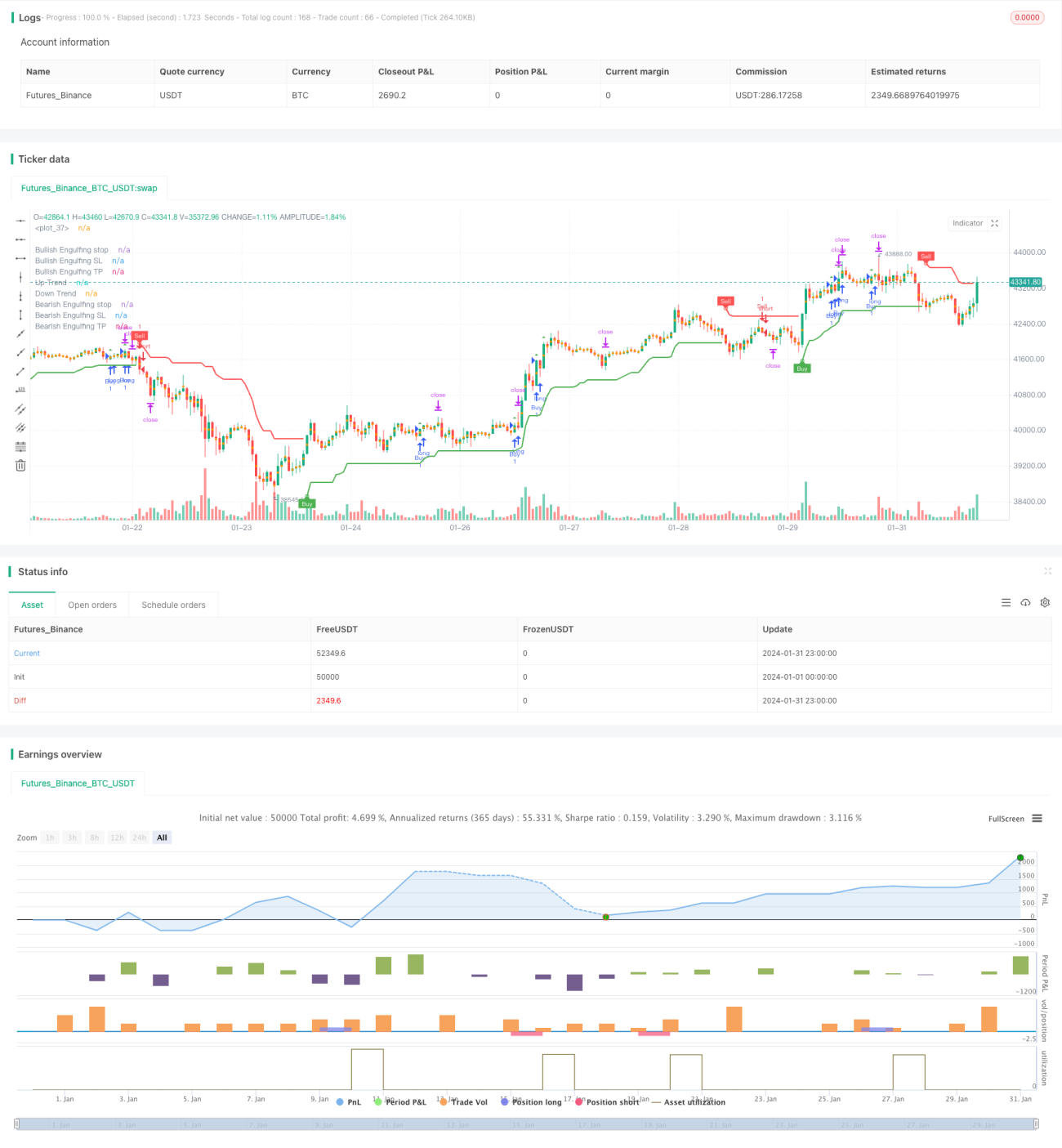

La estrategia de tendencia de engullimiento dinámico es una estrategia que opera según la formación de engullimiento en la dirección de la tendencia. Esta estrategia utiliza el Rango Verdadero Promedio (ATR) para medir la volatilidad del mercado, el indicador de Súper Tendencia para determinar la dirección de la tendencia del mercado, y realiza operaciones largas y cortas cuando se cumple la formación de engullimiento y coincide con la dirección de la tendencia. Los niveles de stop loss y take profit también se calculan dinámicamente en función de la formación de engullimiento.

Principios de la estrategia

- Calcular el ATR para medir la volatilidad del mercado.

- Calcular el indicador de Súper Tendencia para determinar la dirección principal de la tendencia del mercado.

- Definir las condiciones de mercado alcista y bajista.

- Identificar las formaciones de engullimiento alcista (en tendencia alcista) y bajista (en tendencia bajista) que coinciden con la dirección de la tendencia.

- Calcular los niveles de stop loss y take profit según la formación de engullimiento.

- Realizar operaciones largas o cortas cuando se identifica una formación de engullimiento y coincide con la dirección de la tendencia.

- Cerrar la posición cuando el precio toque el nivel de stop loss o take profit.

- Marcar las formaciones de engullimiento en el gráfico.

Análisis de ventajas de la estrategia

- Combina la formación de engullimiento con la identificación de tendencias para mejorar la calidad de las señales.

- Puede identificar puntos de inflexión de la tendencia para operar de manera específica.

- Las señales de largo y corto son claras, fáciles de captar el momento de operar.

- La estrategia de stop loss con engullimiento sigue la tendencia y controla el riesgo.

- El marco del código es claro, fácil de optimizar y mejorar.

Análisis de riesgos de la estrategia

Esta estrategia también presenta algunos riesgos:

- La formación de engullimiento puede ser una ruptura falsa, un error de identificación puede causar pérdidas.

- Es difícil determinar los parámetros de la formación de engullimiento, como el tamaño del volumen, la duración, etc.

- El mecanismo de identificación de tendencias puede ser imperfecto, lo que lleva a operaciones que no coinciden con la tendencia.

- La configuración de los niveles de stop loss y take profit depende de la experiencia, puede ser demasiado subjetiva.

- El rendimiento depende de la optimización de parámetros, requiere una gran cantidad de datos históricos para su validación.

Para los riesgos anteriores, se pueden controlar y mejorar mediante los siguientes métodos:

- Combinar con otros indicadores técnicos para filtrar señales de ruptura falsa.

- Utilizar métodos de cálculo de parámetros más robustos, como ATR adaptativo.

- Aumentar la confiabilidad del mecanismo de identificación de tendencias, por ejemplo, introduciendo modelos de aprendizaje automático.

- Utilizar algoritmos genéticos u otros medios para encontrar la mejor combinación de parámetros.

- Realizar backtesting en ventanas de tiempo más largas para garantizar la robustez de los parámetros.

Direcciones de optimización de la estrategia

- Se pueden introducir modelos de aprendizaje automático para mejorar la precisión de la identificación de tendencias.

- Combinar nuevos métodos de reconocimiento de patrones para mejorar la identificación de formaciones de engullimiento.

- Utilizar las últimas estrategias de take profit y stop loss para optimizar dinámicamente los puntos de take profit y stop loss.

- Se puede desarrollar una estrategia de ruptura de engullimiento más adecuada para operaciones a corto plazo basada en datos de alta frecuencia.

- Se puede aplicar a diferentes activos para ajustar y optimizar parámetros.

Conclusión

En general, la estrategia de tendencia de engullimiento dinámico combina la eficaz formación de engullimiento con una precisa identificación de la tendencia, creando una estrategia de trading con señales de entrada precisas y niveles razonables de take profit y stop loss. Durante su aplicación, se puede mejorar aún más la estabilidad y rentabilidad de la estrategia mediante la optimización de parámetros, el control de riesgos y la introducción de nuevas tecnologías. Esta estrategia tiene un marco claro y una gran versatilidad, lo que la hace digna de un estudio y aplicación más profundos.

- 1