Stratégie de trading quantitative combinant tendance et oscillation.

Aperçu

La stratégie de double tendance et oscillation est une stratégie de trading quantitatif combinant tendance et oscillation. Elle utilise la combinaison de deux indicateurs pour identifier la direction et la force de la tendance, et recherche les meilleurs points d'entrée lorsque la tendance oscille.

Principe de la stratégie

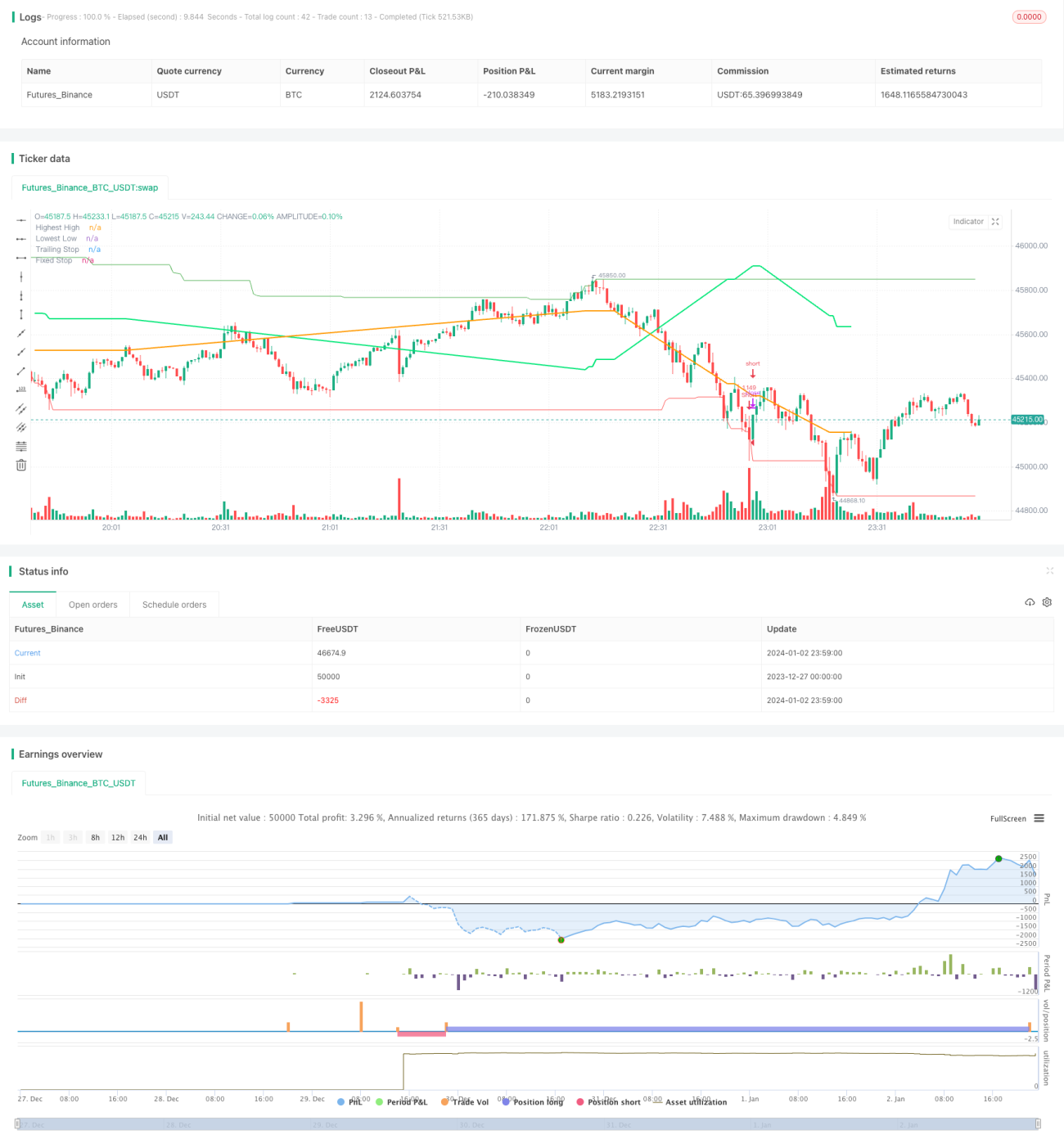

Cette stratégie utilise principalement deux indicateurs publics : Trend Surfers et Mawreez's Trend Oscillator.

Trend Surfers est un indicateur de stop suiveur de tendance. Il calcule les plus hauts et plus bas sur une période donnée pour déterminer l'évolution des prix et suggérer une position de stop. Par exemple, lorsque le prix dépasse le plus haut des 168 dernières bougies, c'est un signal haussier ; lorsqu'il casse le plus bas des 168 dernières bougies, c'est un signal baissier.

Mawreez's Trend Oscillator est un oscillateur à deux lignes. Similaire au MACD, il utilise la différence des DI pour juger de la direction et de la force de la tendance. La courbe de cet indicateur au-dessus de 0 est haussière, en dessous est baissière.

Les règles de trading sont les suivantes :

- Entrée longue : lorsque Trend Surfers franchit la ligne haute et que Mawreez's Trend Oscillator est haussier.

- Entrée courte : lorsque Trend Surfers casse la ligne basse et que Mawreez's Trend Oscillator est baissier.

Le stop-loss combine un stop suiveur de tendance et un stop fixe.

Avantages

Cette stratégie combine les indicateurs de tendance et d'oscillation, permettant à la fois de capturer la tendance et de trouver de bons prix d'entrée en période d'oscillation. Ses avantages sont :

- Double filtre des indicateurs, évitant efficacement les faux signaux de cassure.

- Combinaison tendance/oscillation, facilitant l'accumulation à bas prix dans les zones d'oscillation ou la prise de positions allégées en haut.

- Utilisation de multiples méthodes de stop-loss, permettant un bon contrôle du risque.

Analyse des risques

Cette stratégie comporte également certains risques :

- La combinaison de deux indicateurs peut entraîner des signaux manqués.

- L'indicateur de tendance et l'oscillateur peuvent émettre des signaux contradictoires.

- Un stop fixe peut être déclenché trop tôt.

Pour atténuer ces risques, on peut :

- Assouplir les paramètres des indicateurs pour réduire le filtrage.

- Ajouter des règles de confirmation de tendance pour éviter les conflits.

- Ajuster dynamiquement la position du stop.

Pistes d'optimisation

Cette stratégie offre des possibilités d'optimisation supplémentaires :

- Tester différentes combinaisons de paramètres et périodes pour trouver les meilleurs réglages.

- Ajouter des indicateurs auxiliaires comme la volatilité ou le volume.

- Utiliser des techniques d'apprentissage automatique pour optimiser dynamiquement les indicateurs et paramètres.

Conclusion

La stratégie de double tendance et oscillation combine les avantages du suivi de tendance et des oscillateurs. Elle permet d'identifier la direction de la tendance tout en saisissant les opportunités d'oscillation. En optimisant les paramètres et les règles, sa rentabilité peut être encore améliorée. Cette stratégie présente un bon potentiel de développement.

- 1