Stratégie de trading ADX bidirectionnelle

Aperçu

La stratégie de trading bidirectionnelle ADX est une stratégie quantitative qui exploite l'indice directionnel moyen (ADX) pour effectuer des transactions dans les deux sens. En calculant l'écart entre l'indicateur ADX et les indicateurs DIPlus et DIMinus, elle définit un seuil pour déterminer si un signal de trading est généré, et réalise des transactions longues et courtes afin de dégager des profits.

Principe de la stratégie

- Calcul de la plage de variation réelle (True Range)

- Calcul du mouvement directionnel haussier (Directional Movement Plus) et du mouvement directionnel baissier (Directional Movement Minus)

- Calcul de la plage de variation réelle lissée (Smoothed True Range)

- Calcul du mouvement directionnel haussier lissé (Smoothed Directional Movement Plus) et du mouvement directionnel baissier lissé (Smoothed Directional Movement Minus)

- Calcul des indicateurs DIPlus, DIMinus et ADX

- Calcul de l'écart entre DIPlus et ADX, et entre DIMinus et ADX

- Définition des seuils d'écart pour les transactions longues et courtes

- Génération d'un signal de trading lorsque l'écart dépasse le seuil

- Émission d'ordres d'achat et de vente

Le cœur de cette stratégie consiste à utiliser des indicateurs de mouvement directionnel tels que l'ADX pour déterminer la direction et la force de la tendance, combinés à une règle de décision basée sur les écarts pour fixer des seuils et effectuer des transactions automatisées.

Analyse des avantages

- L'utilisation de l'ADX pour déterminer la direction de la tendance permet de capturer avec précision les tendances du marché.

- L'application de la règle de décision par écart filtre efficacement les faux signaux.

- Le trading bidirectionnel permet de capter pleinement les opportunités haussières et baissières.

- Le trading entièrement automatisé ne nécessite aucune intervention humaine.

- La logique de la stratégie est claire, facile à comprendre et à modifier.

Analyse des risques

- L'indicateur ADX présente un certain retard et peut manquer les points de retournement de tendance.

- Le risque de trading bidirectionnel est accru, ce qui peut amplifier les pertes.

- Un réglage inapproprié des paramètres peut entraîner des transactions excessives.

- Les données de backtest ne peuvent pas représenter le marché réel, les risques en trading réel persistent.

Solutions :

- Combiner avec d'autres indicateurs pour confirmer les signaux de trading.

- Optimiser les paramètres pour contrôler la fréquence des transactions.

- Utiliser un Position Sizing strict pour gérer la taille des positions.

Axes d'optimisation

- Optimiser les paramètres de l'ADX pour améliorer sa sensibilité.

- Ajouter d'autres indicateurs pour filtrer les signaux.

- Appliquer des algorithmes d'apprentissage automatique pour optimiser les paramètres.

- Utiliser des stratégies avancées de stop-loss pour contrôler le risque de perte.

- Combiner des modèles prédictifs pour obtenir des signaux de trading plus précis.

Conclusion

La stratégie de trading bidirectionnelle ADX est dans l'ensemble une stratégie quantitative très pratique. Elle utilise l'indicateur ADX pour juger de la tendance et capturer les opportunités de trading dans les deux sens. En même temps, elle applique une règle de décision basée sur les écarts pour garantir la validité des signaux. Cette stratégie possède une logique claire et simple, facile à modifier et à optimiser, et constitue une stratégie de suivi de tendance bidirectionnelle. Grâce à une optimisation raisonnable des paramètres, à l'application de stratégies de stop-loss et au filtrage des signaux, il est possible de renforcer encore la stabilité et la rentabilité de la stratégie.

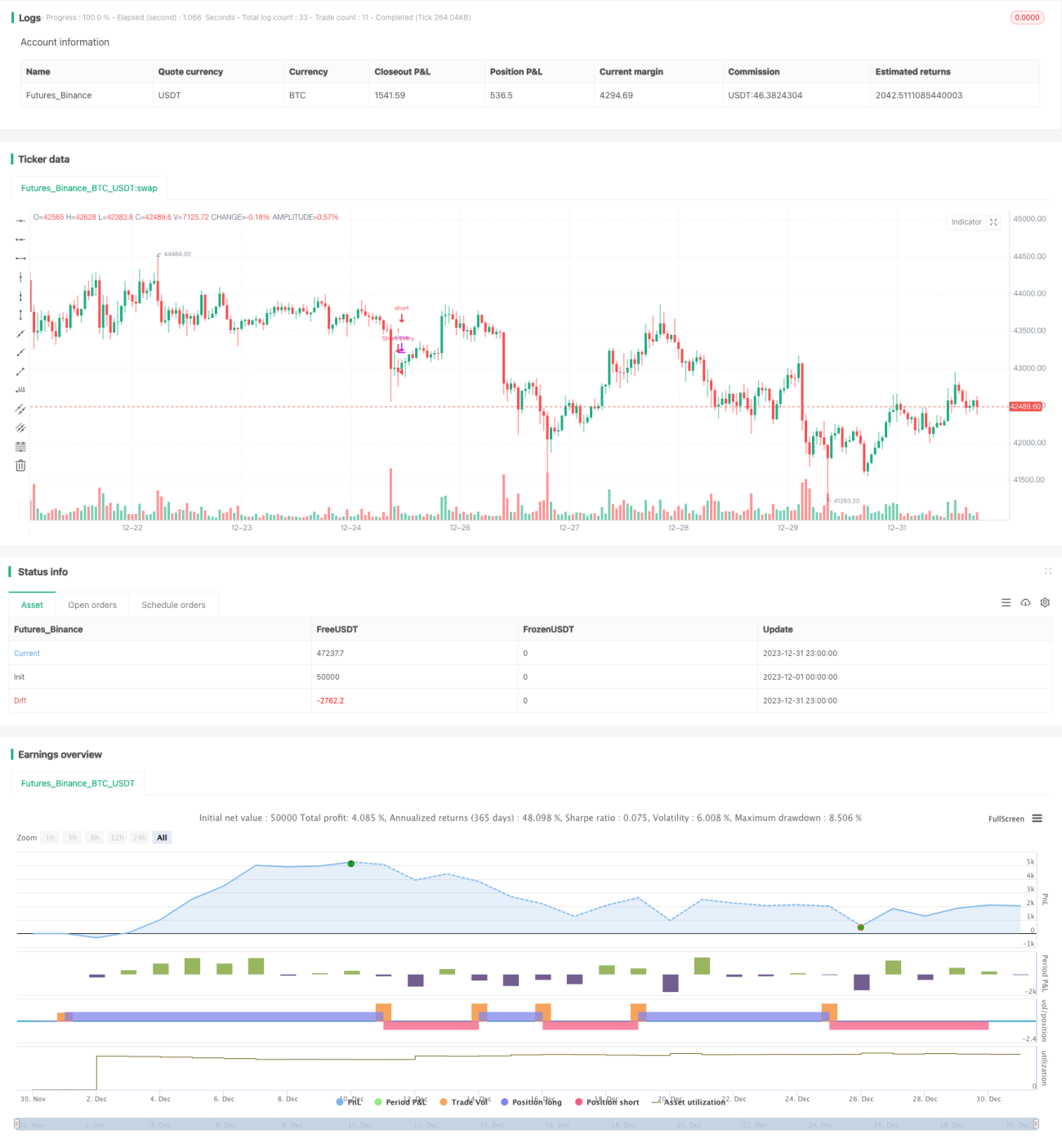

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5- 1