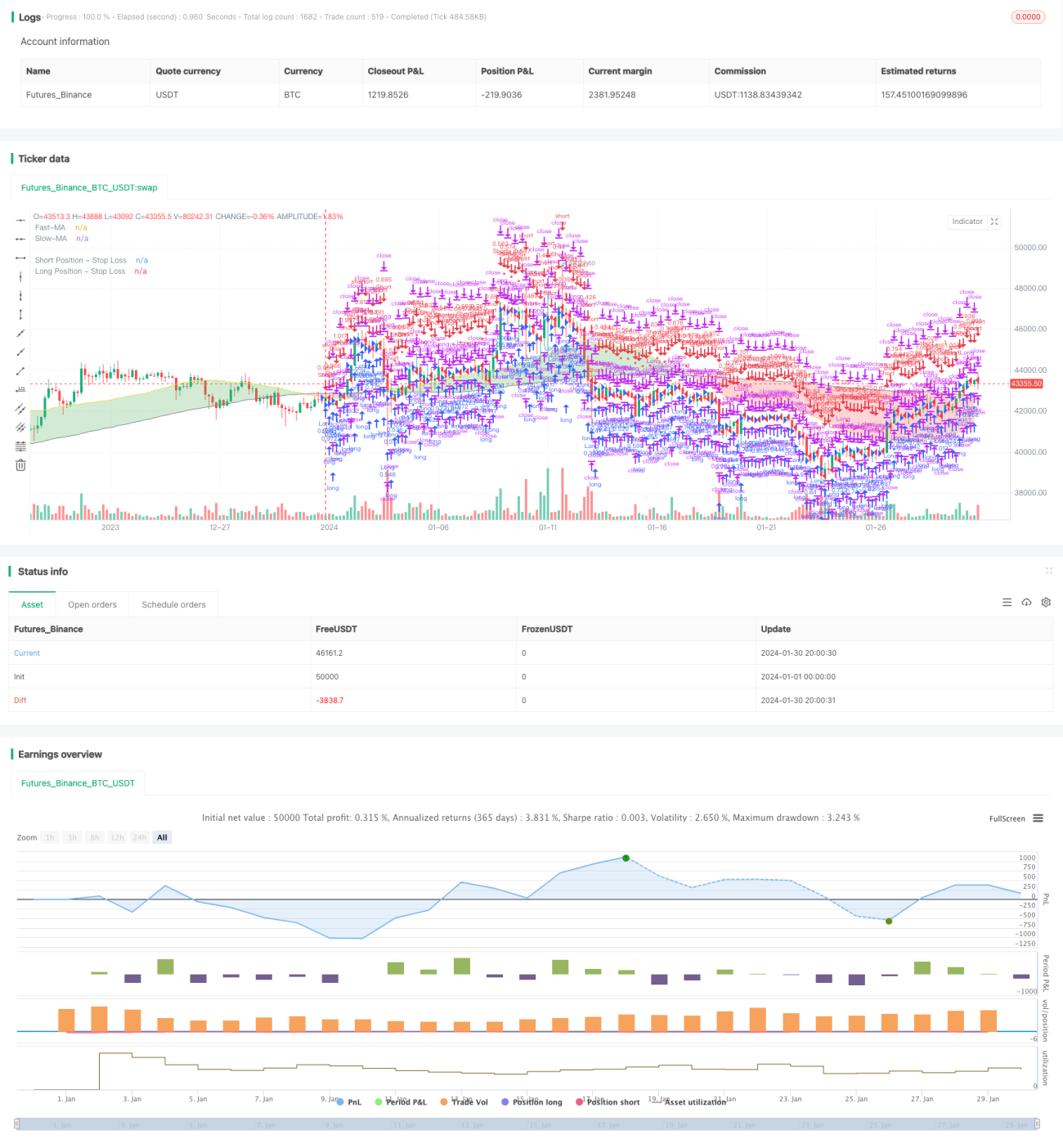

Stratégie de trading quantitatif à double moyenne mobile

Aperçu

Cette stratégie calcule une moyenne mobile rapide et une moyenne mobile lente, combinées avec l'indicateur Parabolic SAR pour générer des signaux d'achat et de vente. Il s'agit d'une stratégie de suivi de tendance. Elle prend une position longue lorsque la moyenne mobile rapide croise au-dessus de la moyenne mobile lente, et une position courte lorsqu'elle croise en dessous. L'indicateur Parabolic SAR est utilisé pour filtrer les faux signaux de cassure.

Principe de la stratégie

- Calcul de la moyenne mobile rapide et de la moyenne mobile lente. Les paramètres des moyennes mobiles sont personnalisables.

- Comparaison des deux moyennes mobiles pour déterminer la direction de la tendance du marché. Lorsque la moyenne mobile rapide croise au-dessus de la moyenne mobile lente, le marché est considéré comme haussier ; lorsqu'elle croise en dessous, le marché est considéré comme baissier.

- Utilisation de la relation entre le prix de clôture et les moyennes mobiles comme confirmation supplémentaire. Un signal d'achat n'est généré que lorsque la ligne rapide croise au-dessus de la ligne lente et que le prix de clôture est supérieur à la ligne rapide. Un signal de vente n'est généré que lorsque la ligne rapide croise en dessous de la ligne lente et que le prix de clôture est inférieur à la ligne rapide.

- Utilisation de l'indicateur Parabolic SAR pour filtrer les faux signaux de cassure. Un signal d'achat final n'est déclenché que si la ligne rapide croise au-dessus de la ligne lente, le prix de clôture est supérieur à la ligne rapide, et le cours de l'action est supérieur à la valeur de Parabolic SAR. L'inverse est vrai pour un signal de vente.

- Définition d'un niveau de stop-loss basé sur la perte maximale acceptable. Le prix de stop-loss spécifique est calculé à l'aide de l'indicateur ATR.

Avantages de la stratégie

- Utilisation des moyennes mobiles pour déterminer la direction de la tendance du marché, évitant ainsi les transactions fréquentes dans un marché en range sans direction claire.

- La double condition de filtrage permet d'éviter efficacement les problèmes courants de faux signaux de cassure.

- L'intégration d'une stratégie de stop-loss permet de contrôler efficacement les pertes par transaction.

Risques de la stratégie

- Les stratégies basées sur des indicateurs sont sujettes à de faux signaux.

- Le risque de change n'est pas pris en compte.

- La stratégie peut manquer les premières phases de mouvements dans une direction différente.

Pour remédier à ces problèmes, les améliorations suivantes peuvent être envisagées :

- Optimiser les paramètres des moyennes mobiles pour les adapter à des instruments spécifiques.

- Combiner avec d'autres indicateurs ou modèles pour filtrer les signaux.

- Envisager un hedging en temps réel ou une conversion automatique du risque de change via le compte de courtage.

Pistes d'optimisation

- Optimiser les paramètres des moyennes mobiles pour mieux capturer les tendances.

- Ajouter une combinaison de modèles pour améliorer la précision des signaux.

- Valider sur plusieurs périodes pour éviter d'être piégé.

- Optimiser la stratégie de stop-loss pour améliorer la stabilité de la stratégie.

Conclusion

Cette stratégie est une stratégie de suivi de tendance typique à double moyenne mobile combinée avec des indicateurs. En comparant la direction des deux moyennes mobiles (rapide et lente), elle détermine la tendance du marché, et en utilisant plusieurs filtres pour éviter les faux signaux, elle génère des signaux de trading. De plus, la stratégie intègre une fonction de stop-loss pour contrôler les pertes par transaction. Son principal avantage réside dans une logique simple et claire, facile à comprendre et à implémenter, et pouvant être optimisée de manière flexible selon les besoins. L'inconvénient est qu'en tant qu'outil grossier de détermination de tendance, la précision des signaux doit être améliorée, ce qui peut être réalisé par l'introduction de modèles avancés comme l'apprentissage automatique.

- 1