Stratégie de trading à double moyenne mobile avec cadres temporels croisés

Aperçu

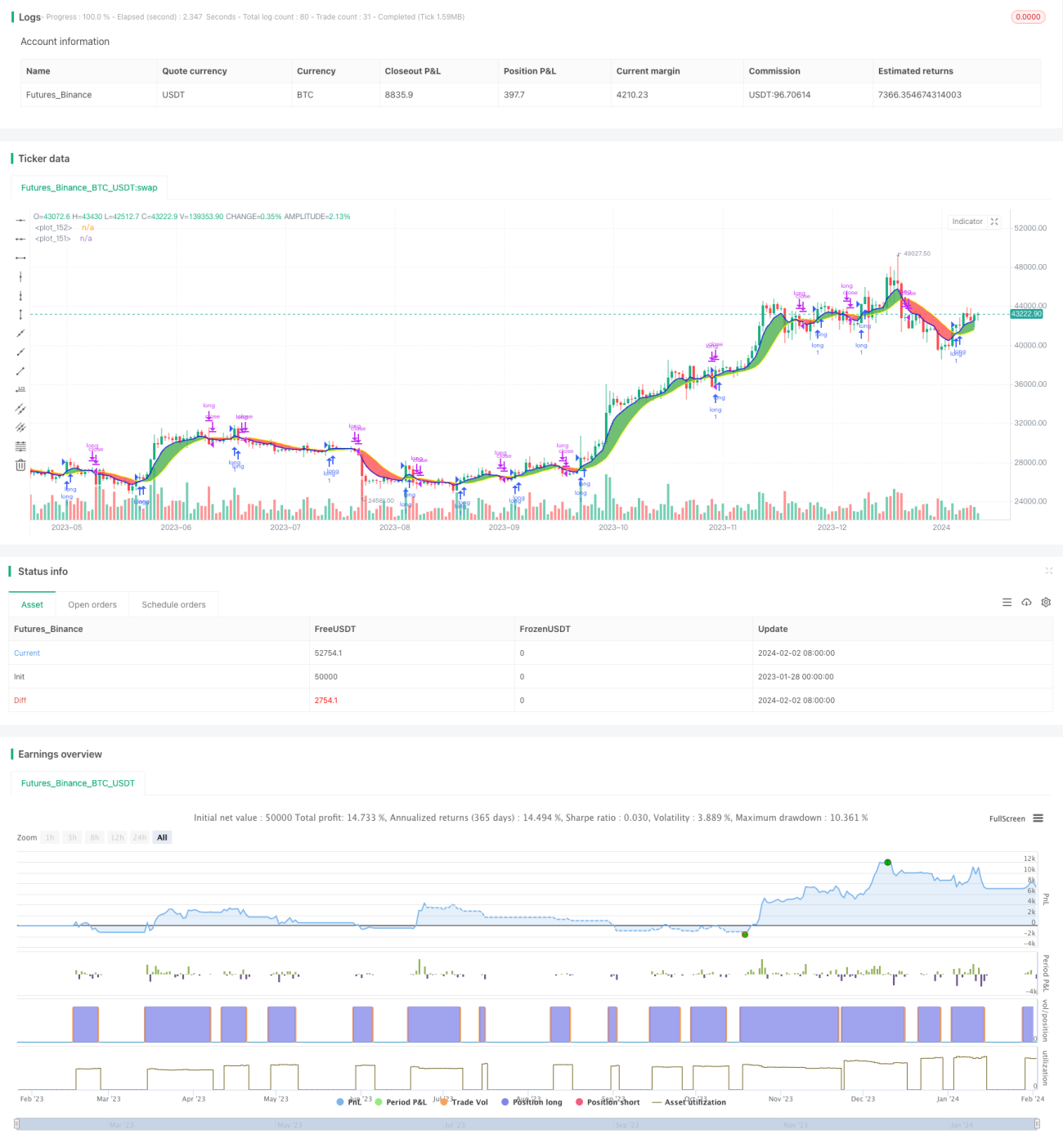

Cette stratégie génère des signaux d'achat et de vente en calculant deux types différents de moyennes mobiles sur deux périodes temporelles distinctes. Il s'agit d'une excellente stratégie bac à sable pour expérimenter différents types de moyennes mobiles et combinaisons de périodes.

Principe de la stratégie

La stratégie utilise deux moyennes mobiles : une moyenne mobile rapide et une moyenne mobile lente. Le cadre temporel de la moyenne mobile rapide doit être supérieur ou égal à celui du graphique. Lorsque la moyenne mobile rapide franchit à la hausse la moyenne mobile lente, un signal d'achat est généré ; lorsqu'elle la franchit à la baisse, un signal de vente est généré.

L'utilisateur peut choisir parmi plusieurs types de moyennes mobiles, comme SMA, EMA, KAMA, etc., et les périodes peuvent être différentes. Cela permet d'expérimenter différentes combinaisons pour trouver les paramètres optimaux.

Analyse des avantages

Le principal avantage de cette stratégie est la possibilité d'ajuster facilement les paramètres pour expérimenter différentes combinaisons et trouver la configuration optimale.

L'utilisateur peut librement choisir le type, la longueur et le cadre temporel des deux moyennes mobiles, et le système calcule et affiche les résultats en temps réel. C'est beaucoup plus simple que de tester des combinaisons de paramètres une par une.

De plus, la stratégie intègre des fonctions de stop-loss et de take-profit, ce qui réduit les risques et améliore la probabilité de gains.

Analyse des risques

Le principal risque de cette stratégie est qu'un mauvais réglage des paramètres peut entraîner des signaux de trading trop fréquents, augmentant ainsi les coûts de transaction et les pertes liées au slippage.

Par ailleurs, les doubles moyennes mobiles sont elles-mêmes sujettes aux faux signaux. Si les paramètres sont mal choisis, les signaux d'achat et de vente peuvent être peu fiables.

Ces risques peuvent être atténués en optimisant les paramètres et en combinant d'autres indicateurs.

Pistes d'optimisation

On peut envisager d'ajouter d'autres indicateurs pour filtrer les signaux, par exemple l'indicateur RSI pour confirmer les signaux d'achat et de vente, réduisant ainsi les faux signaux.

Il est également possible d'optimiser les paramètres des moyennes mobiles par apprentissage pour trouver la meilleure combinaison. On peut aussi recourir à des méthodes d'apprentissage automatique pour optimiser dynamiquement les paramètres.

Résumé

Cette stratégie est un excellent bac à sable pour expérimenter avec des doubles moyennes mobiles. Son atout réside dans la possibilité d'itérer rapidement sur différentes combinaisons de paramètres afin de trouver la stratégie de trading optimale. Bien sûr, elle comporte des risques liés à un mauvais réglage des paramètres, qu'il convient de réduire en filtrant avec d'autres indicateurs. En poursuivant son optimisation, on peut probablement obtenir de meilleurs résultats de trading.

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.- 1