Stratégie de trading de retournement avec Bandes de Bollinger + RSI + ADX + ATR

Aperçu

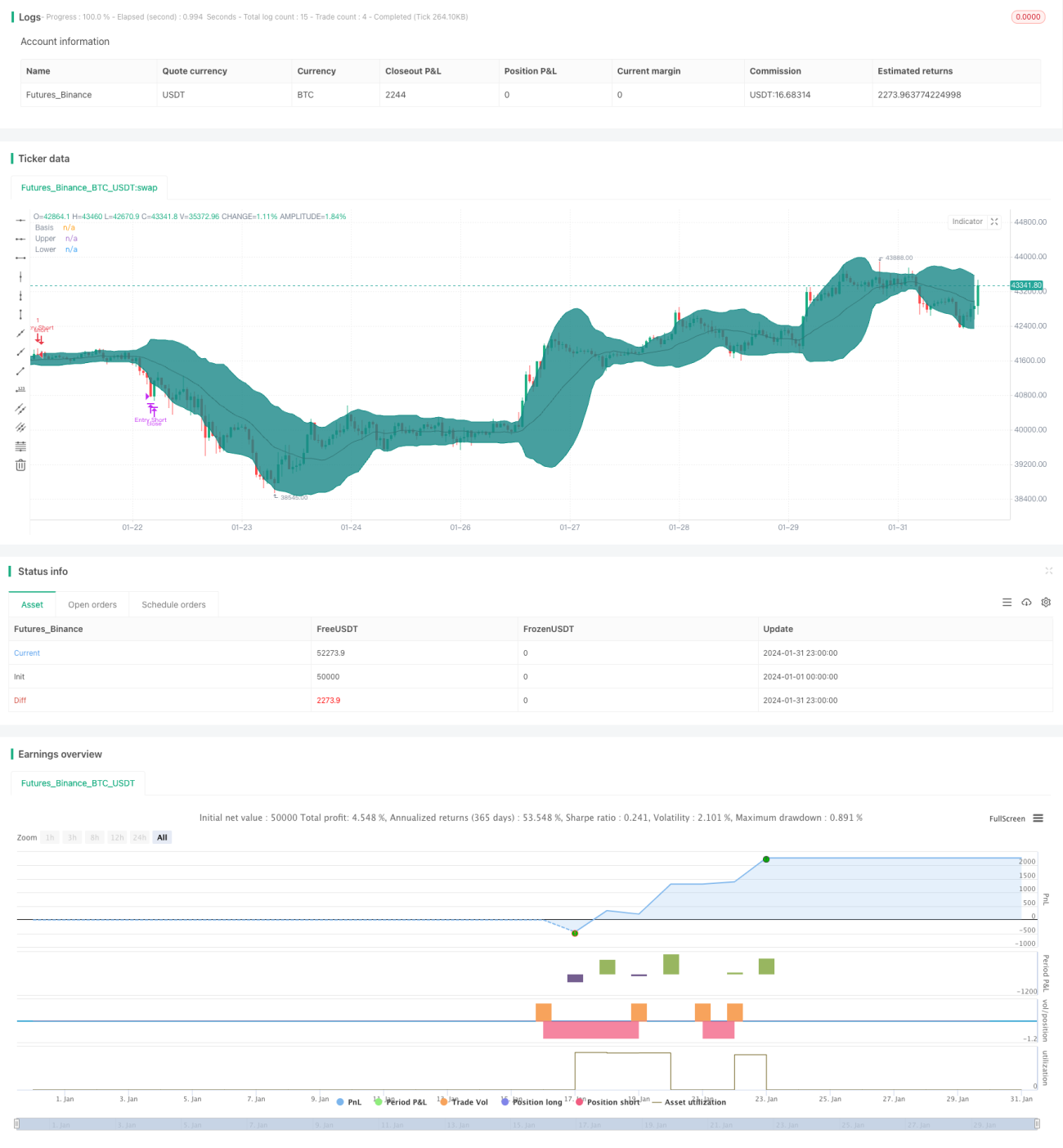

Cette stratégie combine plusieurs indicateurs techniques. Lorsque les bandes de Bollinger signalent un retournement de prix, elle utilise les indicateurs RSI, ADX et ATR pour évaluer la structure du marché et rechercher des opportunités de trading de retournement à haute probabilité.

Principe de la stratégie

-

Utiliser les bandes de Bollinger sur 20 périodes. Lorsque le prix atteint les bandes supérieure ou inférieure, attendre la formation d'une bougie de retournement pour générer un signal d'achat ou de vente.

-

L'indicateur RSI détermine si le marché est dans une zone de range. RSI supérieur à 60 indique une zone haussière, inférieur à 40 indique une zone baissière.

-

ADX inférieur à 20 indique un marché en range, supérieur à 20 indique un marché en tendance.

-

Stop-loss basé sur l'ATR et trailing stop.

-

Filtrer les signaux en utilisant la moyenne mobile EMA.

Analyse des avantages de la stratégie

-

Combinaison de multiples indicateurs pour former des signaux de trading à haute probabilité.

-

Paramètres configurables pour s'adapter à différents environnements de marché.

-

Règles de stop-loss strictes pour contrôler efficacement les risques.

Analyse des risques de la stratégie

-

Un réglage inadéquat des paramètres peut entraîner des transactions trop fréquentes.

-

La probabilité d'échec du retournement subsiste.

-

Le trailing stop peut s'avérer inefficace dans certains marchés.

Directions d'optimisation de la stratégie

-

Tester davantage de combinaisons d'indicateurs pour trouver des configurations de paramètres plus adaptées.

-

Identifier rapidement les opportunités de retournement continu après un échec de cassure.

-

Tester différentes méthodes de stop-loss pour les rendre plus intelligentes.

Résumé

Cette stratégie utilise les bandes de Bollinger comme signal de trading de base, tout en utilisant plusieurs indicateurs auxiliaires pour former un système de filtrage à haute probabilité, et les règles de stop-loss sont également complètes. L'ajustement des paramètres et l'optimisation des indicateurs peuvent encore renforcer les performances de la stratégie. Globalement, cette stratégie constitue un système fiable de trading de retournement.

- 1