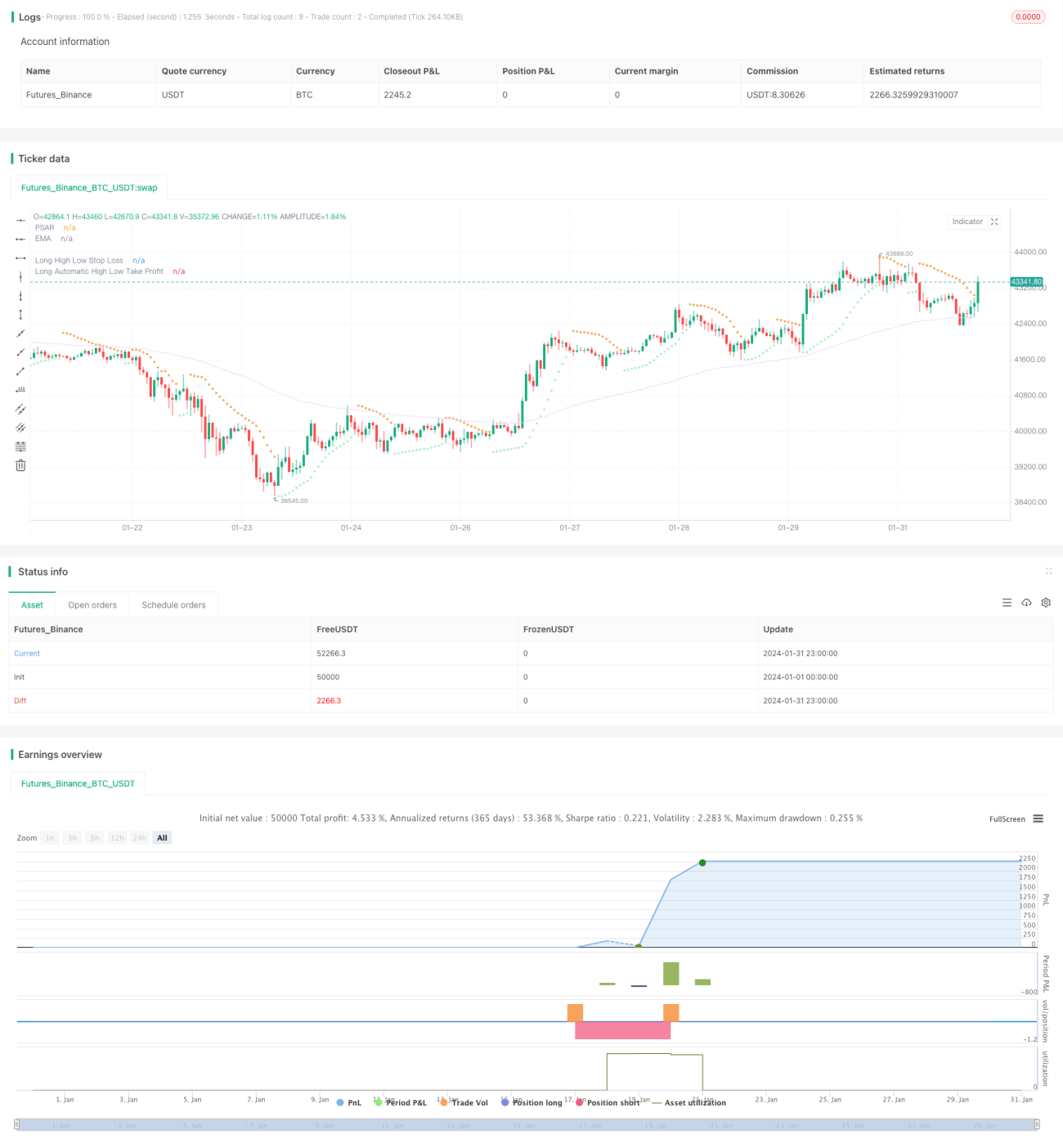

Stratégie d'équilibre du contrôle psychologique en trading

Aperçu

Cette stratégie vise à équilibrer la psychologie du trader et les performances de trading en fixant différents paramètres, afin d'obtenir des rendements plus stables. Elle utilise des indicateurs tels que les moyennes mobiles, les bandes de Bollinger, les canaux de Keltner pour juger des tendances du marché et de la volatilité, combine l'indicateur PSAR pour détecter les signaux de retournement, et exploite l'indicateur TTM Squeeze pour évaluer le momentum. Les signaux de trading sont générés par la combinaison de ces indicateurs. Parallèlement, la stratégie gère les risques via un stop-loss basé sur les hauts et les bas et un take-profit basé sur le ratio risque/récompense.

Principe de la stratégie

La logique principale de cette stratégie est la suivante :

-

Détection de la tendance : utilisation de la moyenne mobile exponentielle (EMA) pour déterminer la direction de la tendance des prix. Un prix au-dessus de l'EMA indique une tendance haussière, en dessous une tendance baissière.

-

Détection des retournements : utilisation du PSAR pour identifier les points de retournement des prix. Un point PSAR apparaissant au-dessus du prix est un signal haussier, en dessous un signal baissier.

-

Évaluation du momentum : utilisation de l'indicateur TTM Squeeze pour mesurer la volatilité et le momentum du marché. Le TTM Squeeze compare la largeur des bandes de Bollinger et des canaux de Keltner pour mesurer la volatilité. Un squeeze indique une volatilité extrêmement faible. La libération du squeeze signale une augmentation de la volatilité et un possible mouvement directionnel important du prix.

-

Génération des signaux de trading : un signal haussier est généré lorsque le prix franchit à la hausse l'EMA et le point PSAR, et que l'indicateur TTM Squeeze sort du squeeze. Un signal baissier est généré lorsque le prix franchit à la baisse l'EMA et le point PSAR, et que le TTM Squeeze entre en squeeze.

-

Mode de stop-loss : stop-loss basé sur les hauts et les bas. Le point de stop-loss est défini en multipliant le plus haut ou le plus bas d'une période récente par un facteur défini.

-

Mode de take-profit : take-profit automatique basé sur le ratio risque/récompense. Le point de take-profit est calculé en multipliant le ratio entre la distance du stop-loss et le prix actuel par le paramètre de ratio risque/récompense.

Grâce au réglage des paramètres, il est possible de contrôler la fréquence des transactions, la gestion de la taille des positions, les niveaux de stop-loss et de take-profit, et d'équilibrer la psychologie du trading.

Analyse des avantages

Cette stratégie présente les avantages suivants :

-

Utilisation de multiples indicateurs pour améliorer la précision des signaux.

-

Priorité aux retournements, complétée par le suivi de tendance, permettant de capter les points de retournement et de réduire la probabilité d'acheter au sommet ou de vendre au creux.

-

L'indicateur TTM Squeeze permet de détecter efficacement les phases de consolidation dans une tendance, évitant ainsi des transactions inefficaces pendant ces périodes.

-

Le stop-loss basé sur les hauts et les bas est simple et pratique, et peut être ajusté en fonction du marché.

-

Le take-profit basé sur le ratio risque/récompense quantifie la relation entre gains et pertes, facilitant les ajustements.

-

Les paramètres sont flexibles et peuvent être affinés en fonction de la tolérance au risque personnelle.

Analyse des risques

Cette stratégie comporte également les risques suivants :

-

La combinaison de multiples indicateurs, bien qu'améliorant la précision, peut augmenter la probabilité de manquer des points d'entrée.

-

En tant que stratégie axée sur les retournements, elle peut être moins performante dans les marchés en forte tendance.

-

Le stop-loss basé sur les hauts et les bas peut parfois être franchi, sans pouvoir éviter complètement les risques.

-

Le take-profit basé sur le ratio risque/récompense peut devenir inefficace en cas de gaps de prix ou d'ajustements.

-

Un mauvais réglage des paramètres peut entraîner des pertes ou des stop-loss fréquents.

Pistes d'optimisation

Cette stratégie peut être optimisée dans les directions suivantes :

-

Ajouter ou ajuster les poids des indicateurs pour améliorer la précision des signaux.

-

Optimiser les paramètres des indicateurs de retournement et de tendance pour augmenter la probabilité de gains.

-

Optimiser les paramètres du stop-loss basé sur les hauts et les bas pour le rendre plus rationnel.

-

Tester différents ratios risque/récompense pour obtenir les résultats optimaux.

-

Ajuster le paramètre du nombre de positions pour réduire l'impact des pertes unitaires.

Conclusion

Dans l'ensemble, cette stratégie, grâce à une combinaison d'indicateurs et à un réglage des paramètres, parvient à équilibrer efficacement la psychologie du trading et à générer des rendements positifs stables. Bien qu'il existe encore une certaine marge d'amélioration, elle possède déjà une valeur pratique pour le trading en conditions réelles. Avec des retours du marché et des ajustements de paramètres, cette stratégie a le potentiel de devenir un outil efficace pour maîtriser la psychologie du trading et obtenir des bénéfices stables à long terme.

- 1