ईएमए और एडीएक्स के साथ ट्रिपल सुपरट्रेंड

लेखक:चाओझांग, दिनांक: 2022-05-08 20:48:42टैगःईएमएएडीएक्स

एक रणनीति प्रकाशित करना जिसमें एडीएक्स और ईएमए फ़िल्टर भी शामिल हैं

प्रविष्टिः सभी तीन सुपरट्रेंड सकारात्मक हो जाते हैं। यदि एडीएक्स और ईएमए का फ़िल्टर लागू किया जाता है, तो यह भी जांचें कि क्या एडीएक्स चयनित स्तर से ऊपर है और बंद ईएमए से ऊपर है बाहर निकलनाः जब पहला सुपरट्रेंड नकारात्मक हो जाता है

छोटी प्रविष्टियों के लिए विपरीत

एक फ़िल्टर एक ही पक्ष पर पुनः प्रवेश करने या उससे बचने के लिए दिया जाता है। उदाहरण के लिए, एक लंबे बाहर निकलने के बाद, यदि शॉर्ट सिंगल ट्रिगर होने से पहले प्रवेश की स्थिति फिर से संतुष्ट हो जाती है तो यदि चयनित हो तो पुनः प्रवेश करना पड़ता है।

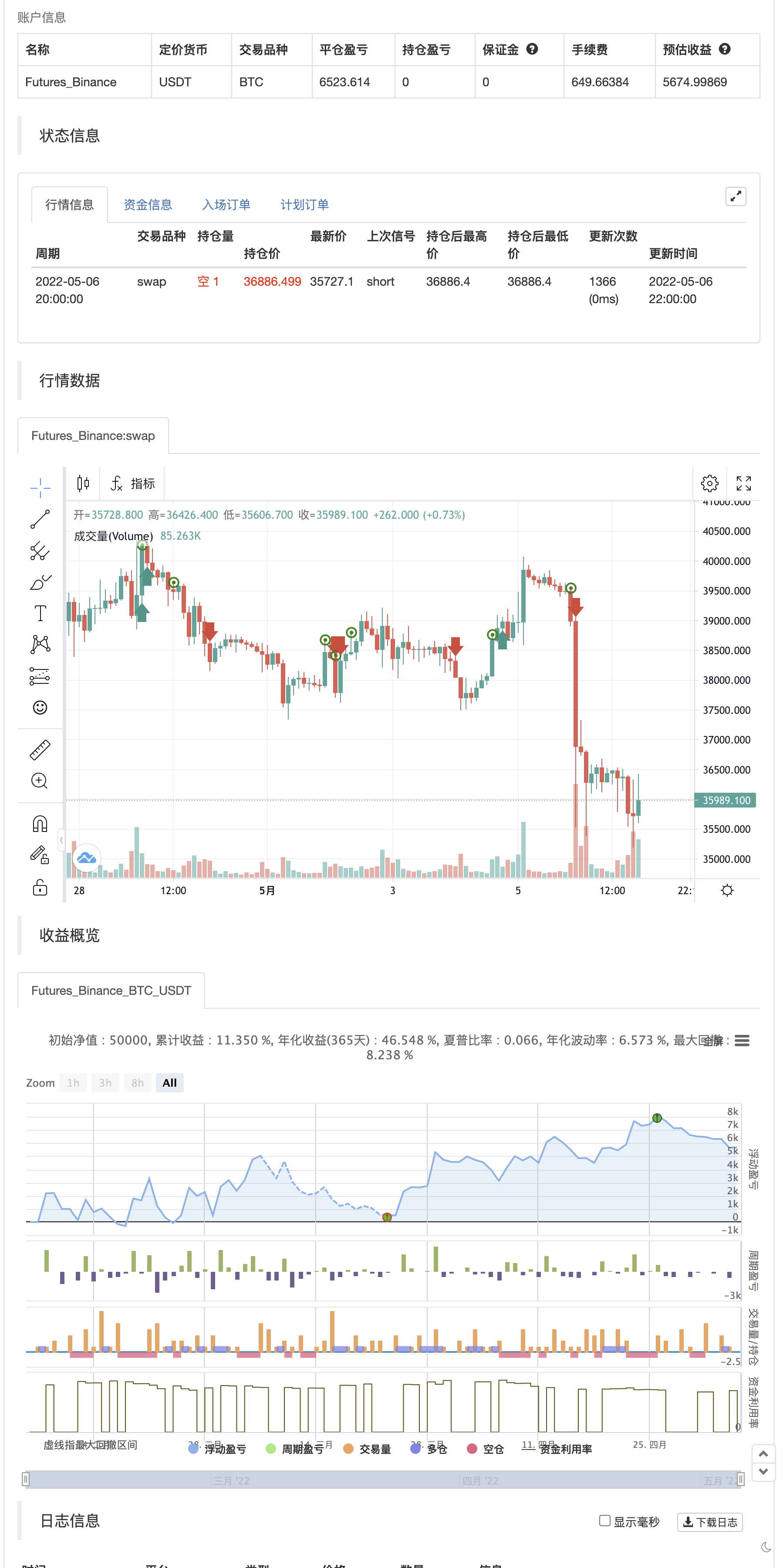

बैकटेस्ट

/*backtest

start: 2022-02-07 00:00:00

end: 2022-05-07 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// ©kunjandetroja

//@version=5

strategy('Triple Supertrend with EMA and ADX', overlay=true)

m1 = input.float(1,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 1')

m2 = input.float(2,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 2')

m3 = input.float(3,"ATR Multi",minval = 1,maxval= 6,step=0.5,group='ST 3')

p1 = input.int(10,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 1')

p2 = input.int(15,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 2')

p3 = input.int(20,"ATR Multi",minval = 5,maxval= 25,step=1,group='ST 3')

len_EMA = input.int(200,"EMA Len",minval = 5,maxval= 250,step=1)

len_ADX = input.int(14,"ADX Len",minval = 1,maxval= 25,step=1)

len_Di = input.int(14,"Di Len",minval = 1,maxval= 25,step=1)

adx_above = input.float(25,"adx filter",minval = 1,maxval= 50,step=0.5)

var bool long_position = false

adx_filter = input.bool(false, "Add Adx & EMA filter")

renetry = input.bool(true, "Allow Reentry")

f_getColor_Resistance(_dir, _color) =>

_dir == 1 and _dir == _dir[1] ? _color : na

f_getColor_Support(_dir, _color) =>

_dir == -1 and _dir == _dir[1] ? _color : na

[superTrend1, dir1] = ta.supertrend(m1, p1)

[superTrend2, dir2] = ta.supertrend(m2, p2)

[superTrend3, dir3] = ta.supertrend(m3, p3)

EMA = ta.ema(close, len_EMA)

[diplus,diminus,adx] = ta.dmi(len_Di,len_ADX)

// ADX Filter

adxup = adx > adx_above and close > EMA

adxdown = adx > adx_above and close < EMA

sum_dir = dir1 + dir2 + dir3

dir_long = if(adx_filter == false)

sum_dir == -3

else

sum_dir == -3 and adxup

dir_short = if(adx_filter == false)

sum_dir == 3

else

sum_dir == 3 and adxdown

Exit_long = dir1 == 1 and dir1 != dir1[1]

Exit_short = dir1 == -1 and dir1 != dir1[1]

// BuySignal = dir_long and dir_long != dir_long[1]

// SellSignal = dir_short and dir_short != dir_short[1]

// if BuySignal

// label.new(bar_index, low, 'Long', style=label.style_label_up)

// if SellSignal

// label.new(bar_index, high, 'Short', style=label.style_label_down)

longenter = if(renetry == false)

dir_long and long_position == false

else

dir_long

shortenter = if(renetry == false)

dir_short and long_position == true

else

dir_short

if longenter

long_position := true

if shortenter

long_position := false

strategy.entry('BUY', strategy.long, when=longenter)

strategy.entry('SELL', strategy.short, when=shortenter)

strategy.close('BUY', Exit_long)

strategy.close('SELL', Exit_short)

//buy1 = ta.barssince(dir_long)

//sell1 = ta.barssince(dir_short)

//colR1 = f_getColor_Resistance(dir1, color.red)

//colS1 = f_getColor_Support(dir1, color.green)

//colR2 = f_getColor_Resistance(dir2, color.orange)

//colS2 = f_getColor_Support(dir2, color.yellow)

//colR3 = f_getColor_Resistance(dir3, color.blue)

//colS3 = f_getColor_Support(dir3, color.maroon)

//plot(superTrend1, 'R1', colR1, linewidth=2)

//plot(superTrend1, 'S1', colS1, linewidth=2)

//plot(superTrend2, 'R1', colR2, linewidth=2)

//plot(superTrend2, 'S1', colS2, linewidth=2)

//plot(superTrend3, 'R1', colR3, linewidth=2)

//plot(superTrend3, 'S1', colS3, linewidth=2)

// // Intraday only

// var int new_day = na

// var int new_month = na

// var int new_year = na

// var int close_trades_after_time_of_day = na

// if dayofmonth != dayofmonth[1]

// new_day := dayofmonth

// if month != month[1]

// new_month := month

// if year != year[1]

// new_year := year

// close_trades_after_time_of_day := timestamp(new_year,new_month,new_day,15,15)

// strategy.close_all(time > close_trades_after_time_of_day)

संबंधित

- GM-8 और ADX दोहरी चलती औसत रणनीति

- VuManChu Cipher B + Divergences रणनीति

- प्रवृत्ति के अनुसार परिवर्तनीय स्थिति ग्रिड रणनीति

- खरीद/बिक्री के साथ ईएमए एडीएक्स आरएसआई का स्केलिंग

- वीडब्ल्यूएमए-एडीएक्स गति और ट्रेंड-आधारित बिटकॉइन लंबी रणनीति

- वॉल्यूम आधारित गतिशील डीसीए रणनीति

- इलियट वेव थ्योरी 4-9 इम्पल्स वेव ऑटोमैटिक डिटेक्शन ट्रेडिंग रणनीति

- स्टॉक सुपरटीआरडी एटीआर 200 एमए

- चलती औसत रंगीन ईएमए/एसएमए

- बहु-समय-सीमा व्यापार

अधिक

- ईएमए बैंड + लेलेडसी + बोलिंगर बैंड ट्रेंड कैचिंग रणनीति

- आरएसआई एमटीएफ ओबी+ओ

- एमएसीडी विली रणनीति

- आरएसआई - खरीदें बेचें संकेत

- हेकिन-अशी प्रवृत्ति

- एचए बाजार पूर्वाग्रह

- इचिमोकू क्लाउड स्मूथ ऑसिलेटर

- विलियम्स %R - चिकनी

- क्यूक्यूई एमओडी + एसएसएल हाइब्रिड + वाद्दाह अट्टार विस्फोट

- स्ट्रैट खरीदें/बेचें

- टॉम डेमार्क अनुक्रमिक ताप मानचित्र

- jma + dwma मल्टीग्रेन द्वारा

- मैजिक एमएसीडी

- संकेतों के साथ Z स्कोर

- पाइन भाषा संस्करण

- 3EMA + बोलिंगर + PIVOT

- मल्टीग्रेन द्वारा बैगेट

- मिलमशीन

- K का रिवर्स इंडिकेटर I

- घेर लेने वाली मोमबत्तियाँ