अवलोकन

सुपर-वन रणनीति एक प्रवृत्ति व्यापार रणनीति है जो सुपर-वन संकेतक के आधार पर व्यापार निर्णय लेती है। यह रणनीति सुपर-वन संकेतक की रूपांतरण रेखा, आधार रेखा और बादल पट्टी के संबंध का उपयोग करके वर्तमान प्रवृत्ति की दिशा का निर्धारण करती है, और मूल्य सुधार के आधार पर प्रवेश करती है।

सुपर-वन रणनीति मुख्य रूप से मध्यम से दीर्घकालिक प्रवृत्ति व्यापार के लिए उपयुक्त है, और बड़ी प्रवृत्तियों में लाभ कमा सकती है। इस रणनीति में प्रवृत्ति पहचान की मजबूत क्षमता भी है।

रणनीति सिद्धांत

सुपर-वन रणनीति मुख्य रूप से निम्नलिखित तत्वों का मूल्यांकन करके व्यापार की दिशा तय करती है:

-

रूपांतरण रेखा और आधार रेखा का संबंध: जब रूपांतरण रेखा ऊपर होती है तो तेजी का संकेत, नीचे होने पर मंदी का संकेत।

-

बादल पट्टी का रंग: जब बादल पट्टी हरी हो तो तेजी, लाल होने पर मंदी।

-

मूल्य सुधार: प्रवेश के लिए मूल्य का रूपांतरण रेखा और आधार रेखा के बाहर वापस आना आवश्यक है।

विशेष रूप से, रणनीति के व्यापार संकेत हैं:

लॉन्ग सिग्नल:

- रूपांतरण रेखा आधार रेखा से ऊपर हो

- मूल्य रूपांतरण रेखा और आधार रेखा से ऊपर हो

- रूपांतरण रेखा और आधार रेखा बादल पट्टी से ऊपर हों

- मूल्य रूपांतरण रेखा और आधार रेखा के नीचे वापस आ जाए

शॉर्ट सिग्नल:

- रूपांतरण रेखा आधार रेखा से नीचे हो

- मूल्य रूपांतरण रेखा और आधार रेखा से नीचे हो

- रूपांतरण रेखा और आधार रेखा बादल पट्टी से नीचे हों

- मूल्य रूपांतरण रेखा और आधार रेखा के ऊपर वापस आ जाए

जब लॉन्ग/शॉर्ट संकेत एक साथ पूरे होते हैं, तो स्थिति के अनुसार पोजीशन खोली जाती है।

लाभ विश्लेषण

सुपर-वन रणनीति के निम्नलिखित लाभ हैं:

-

सुपर-वन संकेतकों के संयोजन का उपयोग करके प्रवृत्ति दिशा का निर्धारण, जिसमें सटीकता अधिक होती है।

-

रूपांतरण रेखा और आधार रेखा मध्यम-अल्पकालिक प्रवृत्ति को स्पष्ट रूप से इंगित करती हैं, जबकि बादल पट्टी दीर्घकालिक प्रवृत्ति को इंगित करती है।

-

मूल्य को रूपांतरण रेखा के बाहर वापस आने की शर्त, जो झूठी ब्रेकआउट से होने वाले नुकसान से बचाती है।

-

जोखिम प्रबंधन में हाल ही की अवधि में उच्चतम और निम्नतम मूल्य स्तरों के आधार पर स्टॉप-लॉस निर्धारित किया जाता है, जो प्रति व्यापार होने वाले नुकसान को प्रभावी ढंग से नियंत्रित करता है।

-

लाभ-हानि अनुपात उचित है, स्थिर लाभ प्राप्त करने पर ध्यान केंद्रित करता है।

-

विभिन्न समयसीमाओं में लागू किया जा सकता है, मध्यम से दीर्घकालिक प्रवृत्ति व्यापार के लिए उपयुक्त।

-

रणनीति की सोच स्पष्ट और समझने में आसान है, मापदंडों के अनुकूलन के लिए बड़ी गुंजाइश है।

-

विभिन्न बाजार स्थितियों में अच्छा प्रदर्शन कर सकती है।

जोखिम विश्लेषण

सुपर-वन रणनीति में निम्नलिखित जोखिम भी हैं:

-

साइडवेज़ बाजार में, स्टॉप-लॉस बार-बार ट्रिगर हो सकता है, जिससे लाभ प्रभावित होता है।

-

जब प्रवृत्ति तेज़ी से बदलती है, तो पोजीशन को समय पर उलटा नहीं किया जा सकता, जिससे नुकसान हो सकता है।

-

निर्धारित लाभ-हानि अनुपात सभी परिसंपत्तियों के लिए उपयुक्त नहीं है, विभिन्न उपकरणों के लिए मापदंडों को समायोजित करने की आवश्यकता है।

-

जब बादल पट्टी से ब्रेकआउट के बाद ऊपर जाने की जगह सीमित हो, तो लाभ सीमित हो सकता है।

-

संकेतक मापदंडों को बार-बार परीक्षण और अनुकूलन की आवश्यकता होती है, उन उपकरणों के लिए उपयुक्त नहीं है जहां मापदंडों में बार-बार बदलाव की आवश्यकता होती है।

निम्नलिखित विधियों से जोखिम कम किया जा सकता है:

-

मापदंडों को अनुकूलित करना ताकि वे विभिन्न समयसीमाओं और उपकरणों की विशेषताओं के अनुरूप हों।

-

प्रवेश संकेतों को फ़िल्टर करने के लिए अन्य संकेतकों का संयोजन, साइडवेज़ बाजार में झूठी ब्रेकआउट से बचने के लिए।

-

स्टॉप-लॉस स्थिति को गतिशील रूप से समायोजित करना, स्टॉप-लॉस के ट्रिगर होने की संभावना को कम करना।

-

विभिन्न लाभ-हानि अनुपात सेटिंग्स का परीक्षण करना।

-

चार्ट पैटर्न जैसी विधियों का उपयोग करके प्रवृत्ति संकेत की ताकत का निर्धारण करना।

अनुकूलन दिशाएँ

सुपर-वन रणनीति को निम्नलिखित पहलुओं से अनुकूलित किया जा सकता है:

-

रूपांतरण रेखा और आधार रेखा के मापदंडों को अनुकूलित करना ताकि वे व्यापार किए जाने वाले उपकरण की विशेषताओं के अनुरूप हों।

-

बादल पट्टी के मापदंडों को अनुकूलित करना ताकि बादल पट्टी दीर्घकालिक प्रवृत्ति के निर्धारण में अधिक सटीक हो।

-

स्टॉप-लॉस एल्गोरिदम को अनुकूलित करना, जैसे ATR के आधार पर स्टॉप-लॉस सेट करना या गतिशील स्टॉप-लॉस का उपयोग करना।

-

अन्य संकेतकों के साथ संयोजन करके संकेतों को फ़िल्टर करना, अधिक फ़िल्टर शर्तें जोड़कर गलत प्रवेश की संभावना को कम करना।

-

लाभ-हानि अनुपात सेटिंग को अनुकूलित करना, रणनीति को विभिन्न उपकरणों और समयसीमाओं पर अनुकूल बनाना।

-

पोजीशन प्रबंधन के लिए मार्टिंगेल विधि का उपयोग करना, विभिन्न बाजार उतार-चढ़ाव आवृत्तियों के अनुकूल होना।

-

मशीन लर्निंग विधियों का उपयोग करके मापदंडों का अनुकूलन, उच्च स्थिरता प्राप्त करना।

-

विभिन्न व्यापार समय अवधि निर्धारित करना, रात्रि सत्र और दिवस सत्र की बाजार स्थितियों के अनुसार समायोजन करना।

सारांश

कुल मिलाकर, सुपर-वन रणनीति मध्यम से दीर्घकालिक प्रवृत्ति व्यापार के लिए बहुत उपयुक्त है। इसमें सुपर-वन संकेतक का उपयोग करके प्रवृत्ति दिशा निर्धारित करने का स्पष्ट लाभ है, साथ ही मूल्य सुधार के आधार पर प्रवेश करने से गलत प्रवेश से बचा जा सकता है। मापदंडों को अनुकूलित करके, रणनीति को अधिक उपकरणों और अधिक समयसीमाओं पर स्थिर लाभ प्राप्त करने में सक्षम बनाया जा सकता है। यह रणनीति समझने में आसान होने के साथ-साथ अनुकूलन की बड़ी गुंजाइश रखती है, और रणनीति अनुसंधान और सीखने के लिए आधारभूत रणनीतियों में से एक के रूप में उपयुक्त है।

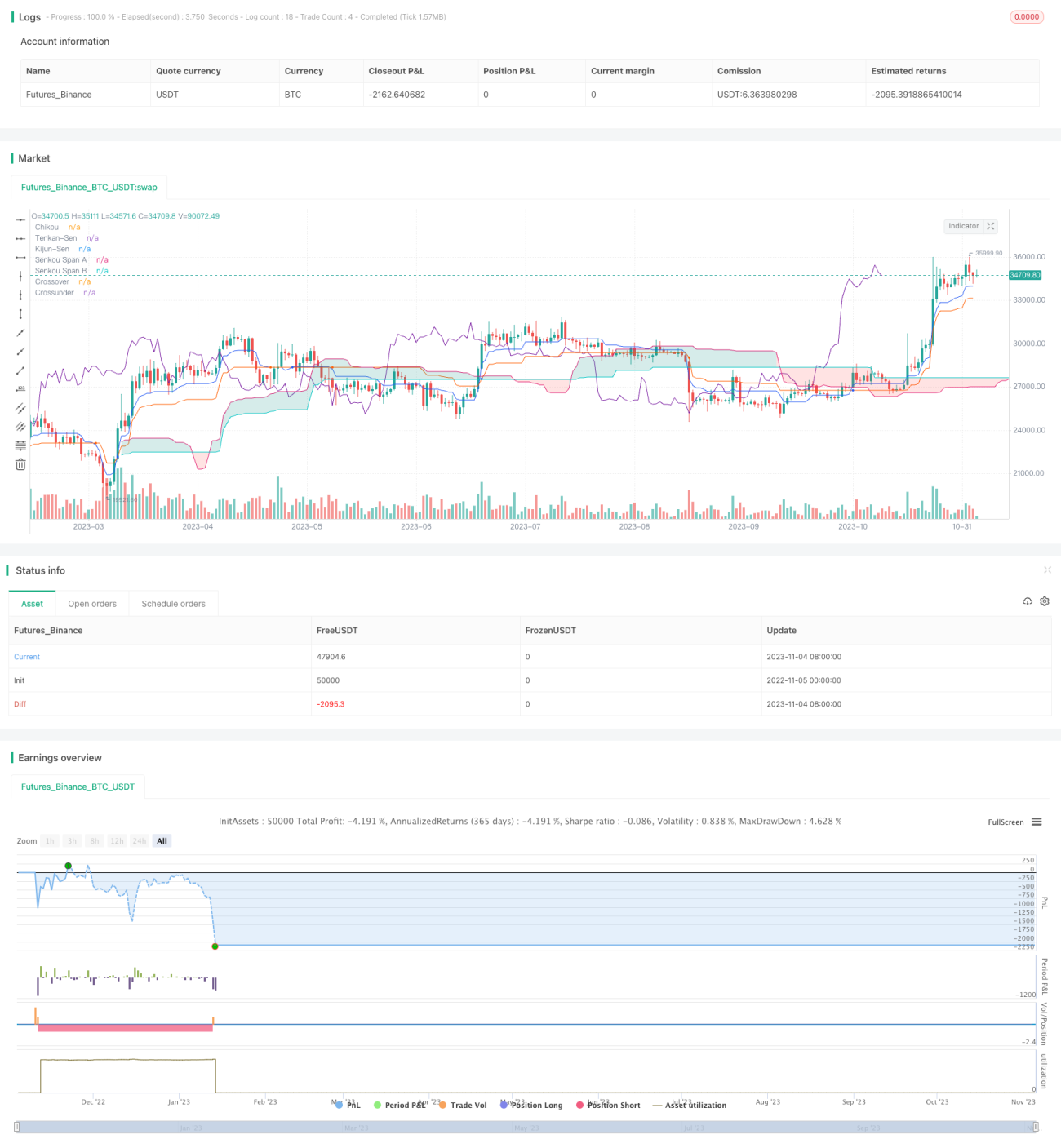

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1