प्रवृत्ति और अस्थिरता को मिलाकर मात्रात्मक ट्रेडिंग रणनीति

अवलोकन

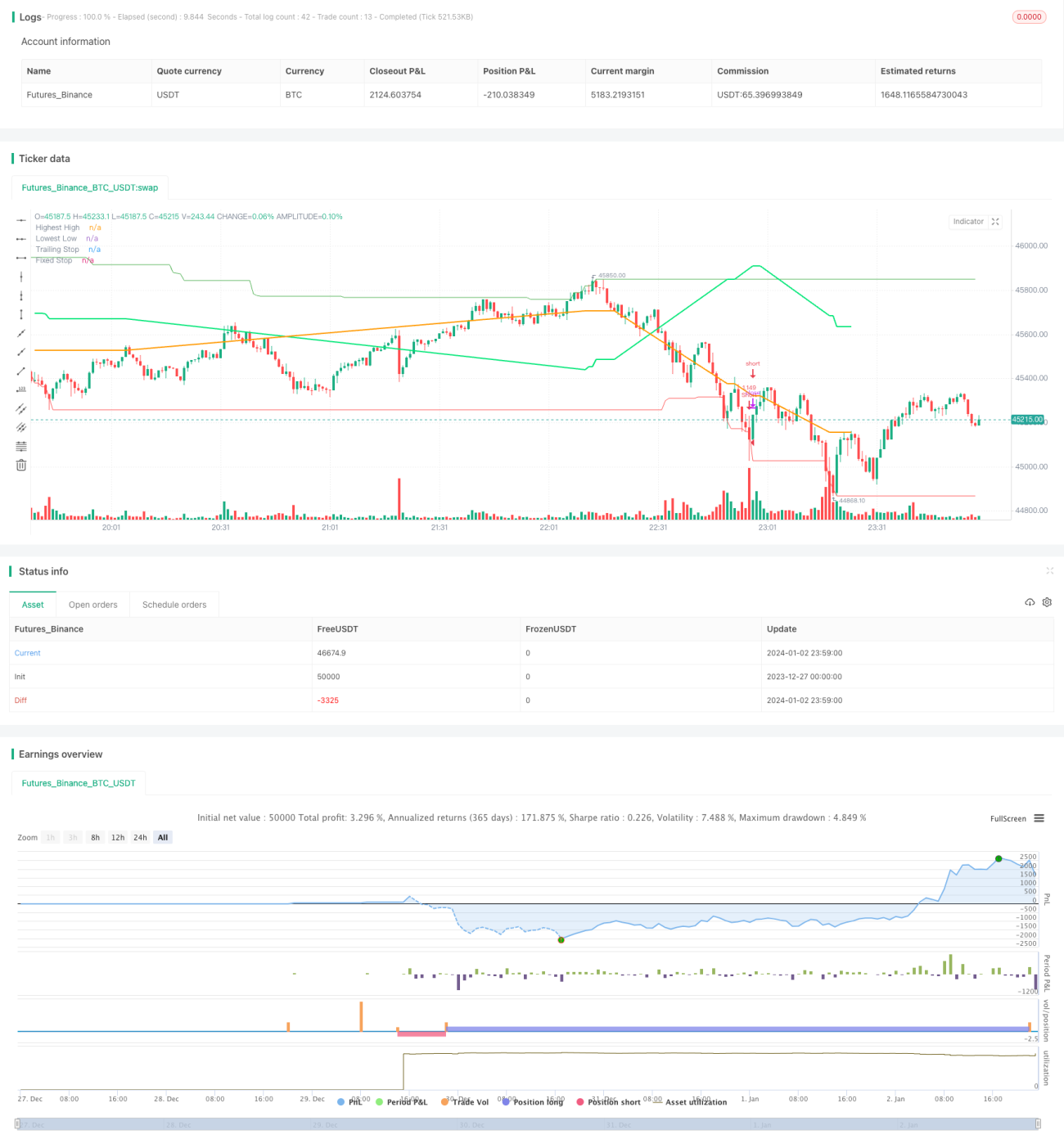

दोहरी प्रवृत्ति दोलन रणनीति एक मात्रात्मक ट्रेडिंग रणनीति है जो प्रवृत्ति और दोलन को जोड़ती है। यह दो संकेतकों के संयोजन का उपयोग करके प्रवृत्ति की दिशा और ताकत की पहचान करती है, और प्रवृत्ति में दोलन होने पर बेहतर प्रवेश अवसर खोजती है।

रणनीति सिद्धांत

यह रणनीति मुख्य रूप से दो सार्वजनिक संकेतकों का उपयोग करती है: ट्रेंड सर्फ़र्स और मावरीज़ ट्रेंड ऑसिलेटर।

ट्रेंड सर्फ़र्स एक प्रवृत्ति अनुवर्ती स्टॉप लॉस संकेतक है। यह एक निश्चित अवधि के भीतर उच्चतम और निम्नतम मूल्यों की गणना करके मूल्य प्रवृत्ति का निर्धारण करता है और सुझाए गए स्टॉप लॉस स्थान प्रदान करता है। उदाहरण के लिए, जब मूल्य पिछले 168 K-लाइनों के उच्चतम मूल्य को तोड़ता है, तो यह तेज़ी का संकेत है; जब मूल्य पिछले 168 K-लाइनों के निम्नतम मूल्य से नीचे आता है, तो यह मंदी का संकेत है।

मावरीज़ ट्रेंड ऑसिलेटर एक दोहरी रेखा वाला दोलन संकेतक है। यह MACD के समान है, DI के अंतर का उपयोग करके प्रवृत्ति की दिशा और ताकत का निर्धारण करता है। इस संकेतक का वक्र 0-रेखा से ऊपर होने पर तेज़ी और नीचे होने पर मंदी का संकेत माना जाता है।

इस रणनीति के ट्रेडिंग नियम हैं:

लॉन्ग प्रवेश: जब ट्रेंड सर्फ़र्स उच्चतम रेखा को तोड़ता है और मावरीज़ ट्रेंड ऑसिलेटर तेज़ी का संकेत देता है, तब खरीदें।

शॉर्ट प्रवेश: जब ट्रेंड सर्फ़र्स निम्नतम रेखा को तोड़ता है और मावरीज़ ट्रेंड ऑसिलेटर मंदी का संकेत देता है, तब बेचें।

स्टॉप लॉस विधि: प्रवृत्ति अनुवर्ती स्टॉप लॉस और निश्चित स्टॉप लॉस का संयोजन।

लाभ विश्लेषण

यह रणनीति प्रवृत्ति और दोलन संकेतकों को जोड़ती है, जिससे यह प्रवृत्ति को पकड़ सकती है और साथ ही दोलन में बेहतर मूल्य पर प्रवेश पा सकती है। इसके निम्नलिखित लाभ हैं:

- दोहरे संकेतक फ़िल्टर प्रभावी रूप से झूठे ब्रेकआउट से बचा सकते हैं।

- प्रवृत्ति और दोलन का संयोजन मूल्य दोलन क्षेत्र में कम स्तर पर संचय या उच्च स्तर पर हल्का प्रवेश पकड़ने में आसानी प्रदान करता है।

- एकाधिक स्टॉप लॉस विधियों का उपयोग जोखिम को अच्छी तरह नियंत्रित कर सकता है।

जोखिम विश्लेषण

इस रणनीति में कुछ जोखिम भी शामिल हैं:

- दोहरे संकेतक संयोजन से ट्रेड छूटने की संभावना बढ़ सकती है।

- प्रवृत्ति और दोलन संकेतक परस्पर विरोधी संकेत दे सकते हैं।

- निश्चित स्टॉप लॉस समय से पहले स्टॉप आउट कर सकता है।

इन जोखिमों से बचने के लिए निम्नलिखित उपाय किए जा सकते हैं:

- संकेतक मापदंडों को उचित रूप से ढीला करें, फ़िल्टर दर कम करें।

- प्रवृत्ति निर्धारण नियम जोड़ें, संकेतक विरोध से बचें।

- स्टॉप लॉस स्थान को गतिशील रूप से समायोजित करें।

अनुकूलन दिशाएँ

इस रणनीति में और अनुकूलन की गुंजाइश है:

- विभिन्न पैरामीटर संयोजनों और अवधि मापदंडों का परीक्षण करके सर्वोत्तम पैरामीटर खोजें।

- अस्थिरता, ट्रेडिंग वॉल्यूम जैसे सहायक नियम जोड़ें।

- मशीन लर्निंग तकनीकों का उपयोग करके संकेतकों और मापदंडों को गतिशील रूप से अनुकूलित करें।

निष्कर्ष

दोहरी प्रवृत्ति दोलन रणनीति प्रवृत्ति अनुवर्ती और दोलन संकेतकों के लाभों का एकीकरण करती है। यह प्रवृत्ति दिशा की पहचान कर सकती है और साथ ही दोलन के अवसरों का लाभ उठा सकती है। मापदंडों और नियमों के अनुकूलन के माध्यम से, रणनीति की लाभप्रदता को और बढ़ाया जा सकता है। इस रणनीति में विकास की अच्छी संभावनाएँ हैं।

- 1