समर्थन प्रतिरोध दोलन व्यापार रणनीति

1

Follow

1802

Followers

अवलोकन

यह रणनीति RSI, स्टोकास्टिक इंडिकेटर के क्रॉसओवर रणनीति को, क्लोजिंग स्लिपेज ऑप्टिमाइजेशन रणनीति के साथ जोड़कर, ट्रेडिंग लॉजिक का सटीक नियंत्रण और सटीक स्टॉप-लॉस तथा टेक-प्रॉफिट सुनिश्चित करती है। साथ ही, सिग्नल ऑप्टिमाइजेशन को शामिल करके, ट्रेंड को बेहतर ढंग से नियंत्रित किया जा सकता है और पूंजी का उचित प्रबंधन किया जा सकता है।

रणनीति का सिद्धांत

- RSI इंडिकेटर ओवरबॉट और ओवरसोल्ड क्षेत्रों का निर्धारण करता है, तथा स्टोकास्टिक इंडिकेटर के K-मान और D-मान के गोल्डन क्रॉस और डेड क्रॉस के साथ मिलकर ट्रेडिंग सिग्नल बनाता है।

- कैंडलस्टिक पैटर्न की पहचान शामिल की गई है, जो ट्रेंड सिग्नल के निर्धारण में सहायता करती है और गलत ट्रेडिंग से बचाती है।

- SMA मूविंग एवरेज ट्रेंड दिशा के निर्धारण में सहायता करता है। जब शॉर्ट-टर्म मूविंग एवरेज नीचे से ऊपर की ओर लॉन्ग-टर्म मूविंग एवरेज को पार करता है, तो यह बुलिश सिग्नल होता है।

- क्लोजिंग स्लिपेज रणनीति, उच्चतम मूल्य और निम्नतम मूल्य के उतार-चढ़ाव की सीमा के आधार पर स्टॉप-लॉस और टेक-प्रॉफिट मूल्य निर्धारित करती है।

लाभ विश्लेषण

- RSI इंडिकेटर पैरामीटर ऑप्टिमाइजेशन, ओवरबॉट और ओवरसोल्ड क्षेत्रों का अच्छी तरह से निर्धारण करता है, जिससे गलत ट्रेडिंग से बचा जा सकता है।

- STO इंडिकेटर पैरामीटर ऑप्टिमाइजेशन, स्मूथिंग पैरामीटर के समायोजन से शोर को फ़िल्टर कर सकता है और सिग्नल की गुणवत्ता में सुधार कर सकता है।

- Heikin-Ashi तकनीकी विश्लेषण शामिल किया गया है, जो कैंडलस्टिक के बॉडी की दिशा में बदलाव को पहचानता है, जिससे ट्रेडिंग सिग्नल की सटीकता सुनिश्चित होती है।

- SMA मूविंग एवरेज बड़ी प्रवृत्ति की दिशा के निर्धारण में सहायता करता है, जिससे प्रवृत्ति के विपरीत ट्रेडिंग से बचा जा सकता है।

- स्टॉप-लॉस और टेक-प्रॉफिट स्लिपेज रणनीति के साथ मिलाकर, प्रत्येक ट्रेड से लाभ को अधिकतम सीमा तक सुरक्षित किया जा सकता है।

जोखिम विश्लेषण

- बाजार में लगातार गिरावट के समय, पूंजी को बड़ा जोखिम होता है।

- ट्रेडिंग की आवृत्ति बहुत अधिक हो सकती है, जिससे ट्रेडिंग लागत और स्लिपेज लागत बढ़ जाती है।

- RSI इंडिकेटर झूठे सिग्नल उत्पन्न कर सकता है, इसलिए इसे अन्य इंडिकेटर्स के साथ फ़िल्टर किया जाना चाहिए।

रणनीति ऑप्टिमाइजेशन

- RSI पैरामीटर समायोजित करें, ओवरबॉट और ओवरसोल्ड निर्धारण को ऑप्टिमाइज़ करें।

- STO इंडिकेटर के पैरामीटर समायोजित करें, स्मूथिंग और अवधि, सिग्नल गुणवत्ता में सुधार करें।

- मूविंग एवरेज की अवधि समायोजित करें, ट्रेंड निर्धारण को ऑप्टिमाइज़ करें।

- अधिक तकनीकी संकेतक शामिल करें, सिग्नल निर्धारण की सटीकता में सुधार करें।

- स्टॉप-लॉस और टेक-प्रॉफिट अनुपात को ऑप्टिमाइज़ करें, प्रति ट्रेड जोखिम को कम करें।

निष्कर्ष

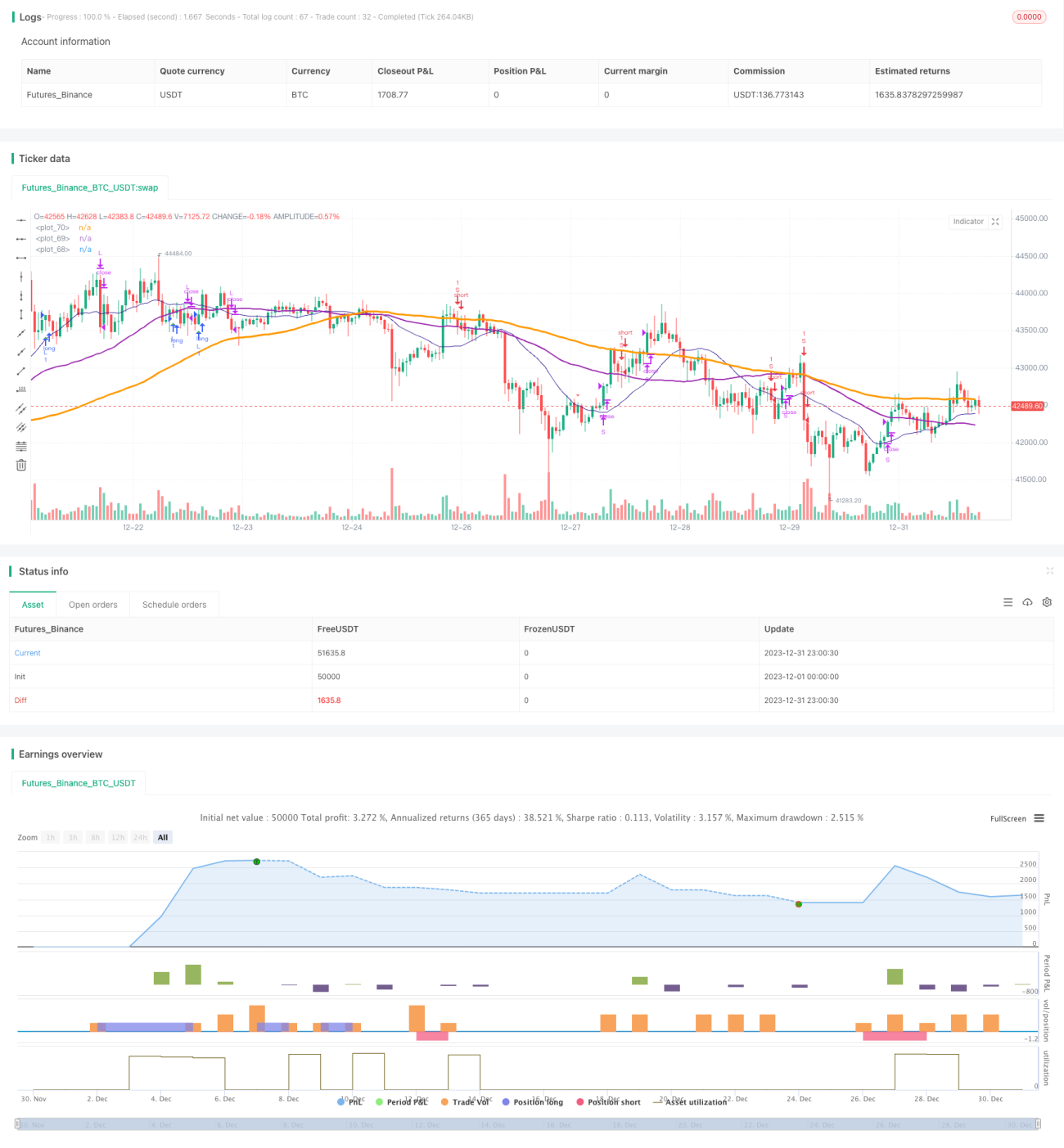

यह रणनीति कई मुख्यधारा तकनीकी संकेतकों के लाभों को एकीकृत करती है, पैरामीटर ऑप्टिमाइजेशन और नियमों के सुधार के माध्यम से ट्रेडिंग सिग्नल की गुणवत्ता और स्टॉप-लॉस/टेक-प्रॉफिट के बीच संतुलन प्राप्त करती है। इसमें एक निश्चित सामान्यता और स्थिर लाभ क्षमता है। निरंतर ऑप्टिमाइजेशन के माध्यम से, जीत दर और लाभ दर को और बढ़ाया जा सकता है।

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1