Strategi Breakout Trailing

Ikhtisar

Strategi ini terutama menggunakan indikator "Kanal Donchian" untuk menerapkan strategi trading breakout berbasis pelacakan. Strategi ini menggabungkan dua pendekatan trading yaitu tren dan breakout, dengan mendeteksi tren jangka panjang terlebih dahulu, lalu mencari titik breakout dalam periode yang lebih pendek untuk melakukan entry, sehingga dapat melakukan trading searah dengan tren. Selain itu, strategi ini juga menetapkan level stop loss dan take profit untuk mengendalikan rasio risiko-imbal hasil setiap transaksi. Secara keseluruhan, strategi ini memiliki keunggulan dalam mengikuti tren, sehingga dapat bertindak sesuai tren dan memanfaatkan peluang tren jangka panjang.

Prinsip Strategi

- Mengatur parameter indikator "Kanal Donchian", dengan periode default 20;

- Mengatur EMA (Exponential Moving Average) yang dihaluskan, dengan periode default 200;

- Mengatur rasio risiko-imbal hasil, default 1,5;

- Mengatur parameter pullback breakout, masing-masing untuk posisi long dan short;

- Mencatat apakah breakout sebelumnya adalah level tertinggi atau terendah;

- Sinyal long: Jika breakout sebelumnya adalah level terendah, dan harga berada di atas batas atas Kanal Donchian dan di atas EMA, maka menghasilkan sinyal long;

- Sinyal short: Jika breakout sebelumnya adalah level tertinggi, dan harga berada di bawah batas bawah Kanal Donchian dan di bawah EMA, maka menghasilkan sinyal short;

- Setelah masuk posisi long, stop loss ditetapkan pada batas bawah Kanal Donchian dikurangi 5 poin, take profit ditetapkan sebagai rasio risiko-imbal hasil dikalikan jarak stop loss;

- Setelah masuk posisi short, stop loss ditetapkan pada batas atas Kanal Donchian dikurangi 5 poin, take profit ditetapkan sebagai rasio risiko-imbal hasil dikalikan jarak stop loss.

Dengan cara ini, strategi menggabungkan penentuan tren dan operasi breakout, sehingga dapat bertindak sesuai tren dan menangkap peluang dalam periode yang lebih pendek di tengah tren jangka panjang. Selain itu, pengaturan stop loss dan take profit dapat mengendalikan risiko-imbal hasil setiap transaksi.

Analisis Keunggulan

- Melacak tren jangka panjang, bertindak sesuai tren, menghindari trading melawan tren.

- Kanal Donchian sebagai indikator jangka panjang, dikombinasikan dengan filter EMA, dapat menentukan arah tren dengan cukup baik.

- Mekanisme stop loss dan take profit mengendalikan risiko setiap transaksi, dapat membatasi potensi kerugian.

- Optimalisasi rasio risiko-imbal hasil dapat memperbesar rasio untung-rugi, mengejar imbal hasil berlebih.

- Parameter backtest fleksibel, dapat disesuaikan dengan kombinasi parameter terbaik untuk pasar yang berbeda.

Analisis Risiko

- Kanal Donchian dan EMA sebagai indikator filter mungkin menghasilkan sinyal yang salah.

- Trading breakout rentan terjebak, perlu mengidentifikasi latar belakang tren yang jelas.

- Jarak stop loss dan take profit tetap, tidak dapat disesuaikan dengan tingkat volatilitas pasar.

- Ruang optimalisasi parameter terbatas, efektivitas pada perdagangan nyata sulit dijamin.

- Sistem trading tidak tahan terhadap banyak kejadian acak, peristiwa black swan dapat menyebabkan kerugian besar.

Arah Optimalisasi

- Dapat mempertimbangkan untuk menambahkan lebih banyak indikator sebagai filter, misalnya indikator osilator, untuk meningkatkan kualitas sinyal.

- Dapat mengatur stop loss dan take profit cerdas, menyesuaikan posisi untung-rugi secara dinamis berdasarkan volatilitas pasar dan indikator ATR.

- Dapat menggunakan metode seperti machine learning untuk menguji dan mengoptimalkan parameter, agar lebih mendekati pasar nyata.

- Dapat mengoptimalkan logika entry, menambahkan indikator volume atau volatilitas sebagai kondisi tambahan, untuk menghindari jebakan.

- Dapat mempertimbangkan untuk menggabungkan dengan strategi trend following atau machine learning, membentuk strategi campuran untuk meningkatkan stabilitas.

Kesimpulan

Sebagai strategi breakout berbasis pelacakan, inti dari strategi ini adalah dengan mendeteksi tren jangka panjang terlebih dahulu, kemudian menggunakan breakout sebagai sinyal untuk bertindak sesuai tren, serta menetapkan stop loss dan take profit untuk mengendalikan risiko setiap transaksi. Strategi ini memiliki beberapa keunggulan, tetapi juga memiliki ruang untuk dioptimalkan. Secara keseluruhan, jika dapat menangani masalah seperti pengaturan parameter, pemilihan waktu entry, dan diperkuat dengan teknik lain, strategi ini dapat menjadi strategi trend following yang praktis. Namun, investor harus tetap ingat bahwa sistem trading apa pun tidak dapat sepenuhnya menghindari risiko pasar, dan manajemen risiko perlu dilakukan dengan baik.

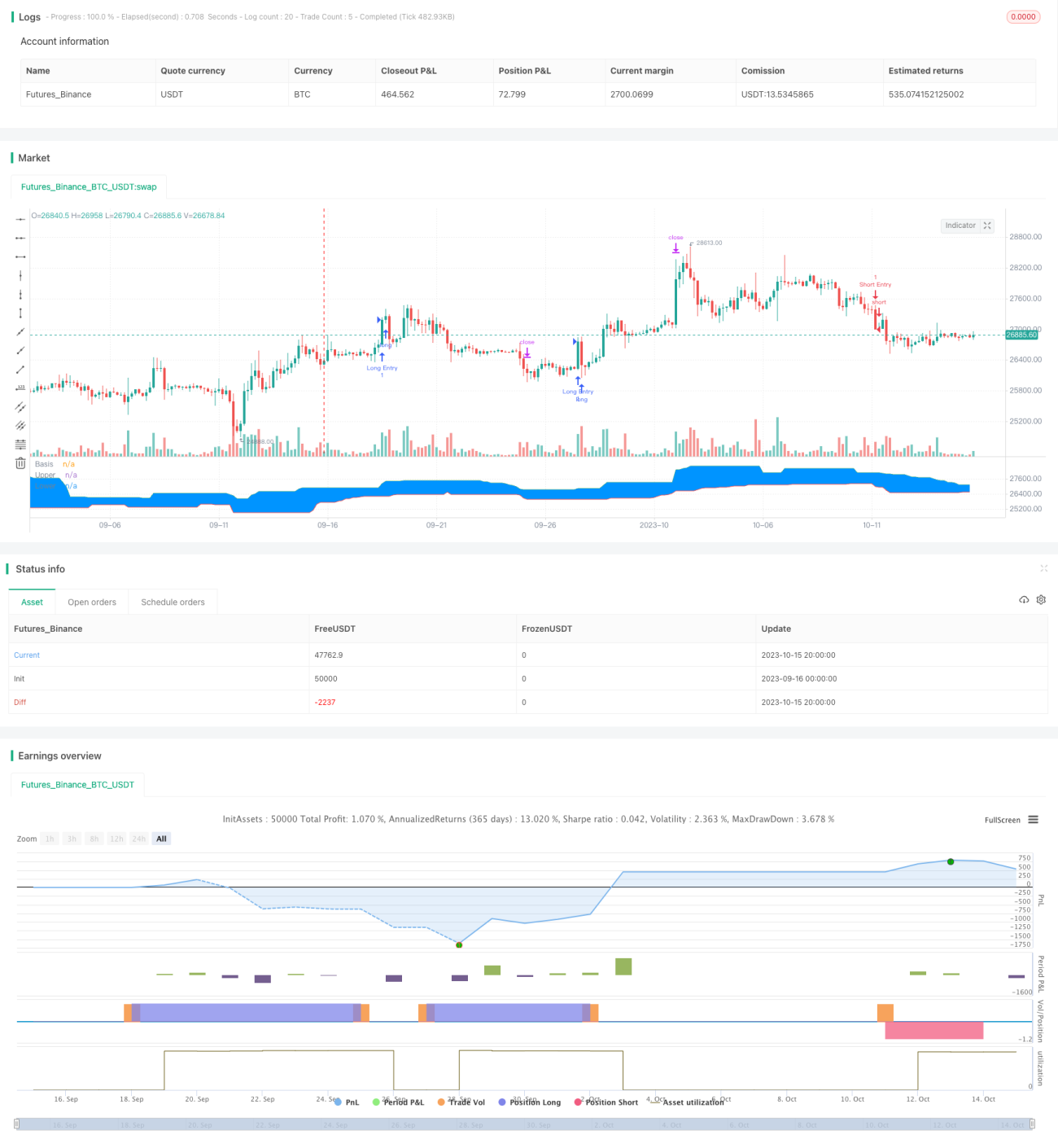

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1