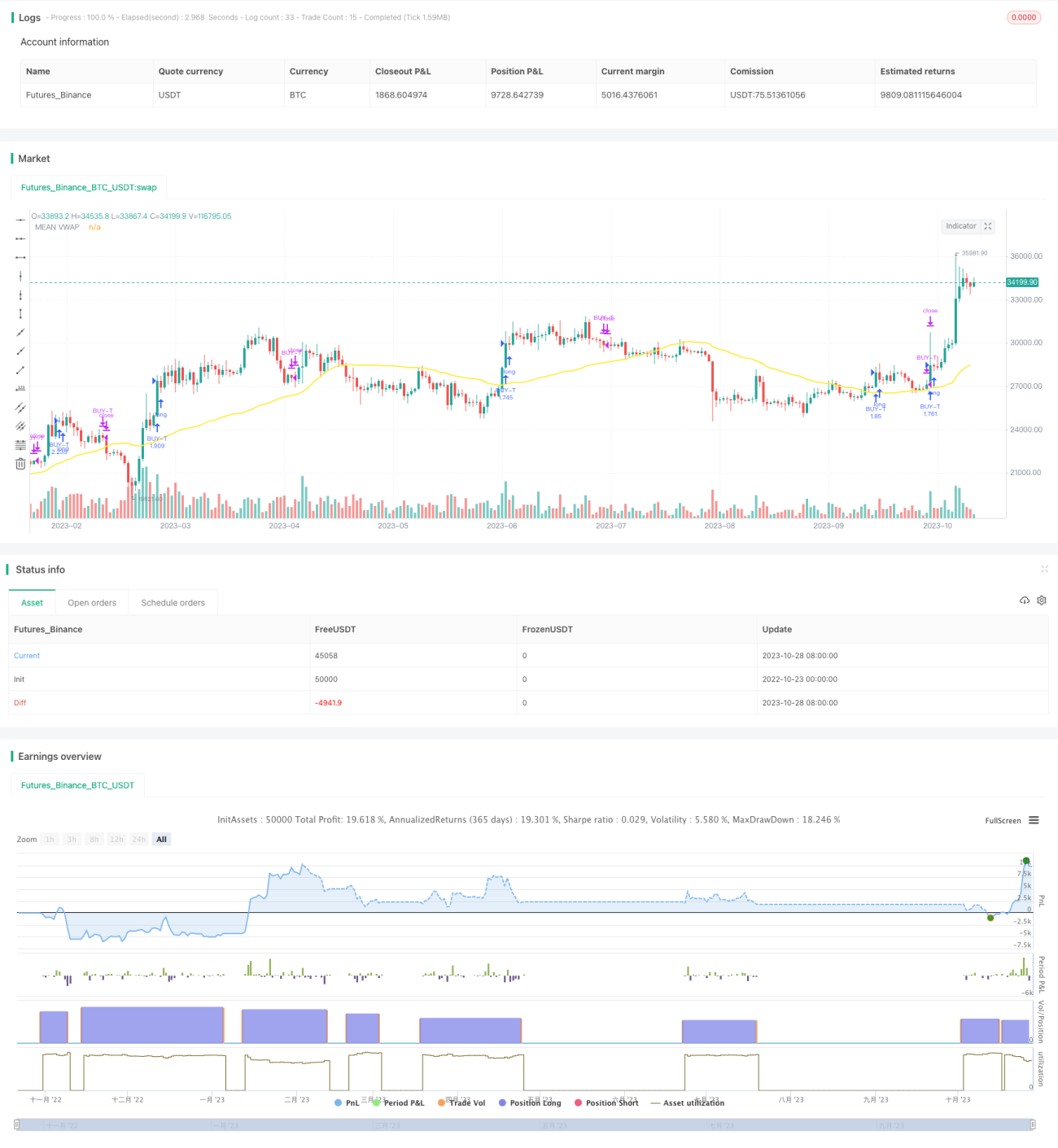

Strategi Perdagangan Algoritmik Pelacakan Dua Garis

Ikhtisar

Strategi ini terutama memanfaatkan prinsip persilangan rata-rata bergerak, dikombinasikan dengan sinyal pembalikan indikator RSI, serta algoritma pelacakan dua garis khusus untuk melakukan perdagangan pelacakan persilangan rata-rata bergerak. Strategi ini melacak persilangan dua rata-rata bergerak dengan periode berbeda: satu rata-rata bergerak cepat melacak tren jangka pendek, dan satu rata-rata bergerak lambat melacak tren jangka panjang. Ketika rata-rata bergerak cepat menembus ke atas rata-rata bergerak lambat, ini menunjukkan tren jangka pendek naik, sehingga dapat membeli; ketika rata-rata bergerak cepat menembus ke bawah rata-rata bergerak lambat, ini menunjukkan tren jangka pendek berakhir, dan posisi harus ditutup.

Prinsip Strategi

-

Hitung dua set garis VWAP dengan parameter berbeda, masing-masing mewakili tren jangka panjang dan tren jangka pendek

- Garis langit lambat dan garis dasar menghitung tren jangka panjang

- Garis langit cepat dan garis dasar menghitung tren jangka pendek

-

Ambil rata-rata dari masing-masing dua set garis langit dan garis dasar sebagai rata-rata bergerak lambat dan rata-rata bergerak cepat

-

Hitung indikator Bollinger Bands untuk menentukan konsolidasi dan breakout

- Garis tengah adalah rata-rata dari rata-rata bergerak cepat dan lambat

- Pita atas dan bawah Bollinger digunakan untuk menentukan breakout

-

Hitung indikator TSV untuk menilai energi volume perdagangan

- TSV > 0 menunjukkan kekuatan kenaikan lebih besar daripada kekuatan penurunan

- TSV lebih besar dari EMA-nya menunjukkan kekuatan yang meningkat

-

Hitung indikator RSI untuk menentukan kondisi overbought dan oversold

- RSI di bawah 30 adalah zona oversold, dapat membeli

- RSI di atas 70 adalah zona overbought, harus menjual

-

Kondisi masuk:

- Rata-rata bergerak cepat menembus ke atas rata-rata bergerak lambat

- Harga penutupan menembus ke atas pita atas Bollinger

- TSV > 0 dan lebih besar dari EMA-nya

- RSI di bawah 30

-

Kondisi keluar:

- Rata-rata bergerak cepat menembus ke bawah rata-rata bergerak lambat

- RSI di atas 70

Analisis Keunggulan

-

Menggunakan sistem rata-rata bergerak ganda, dapat menangkap tren jangka panjang dan jangka pendek secara bersamaan

-

Indikator RSI menghindari pembelian di area overbought dan penjualan di area oversold

-

Indikator TSV memastikan ada volume perdagangan yang cukup untuk mendukung tren

-

Memanfaatkan Bollinger Bands untuk menentukan titik breakout kritis

-

Kombinasi berbagai indikator dapat menyaring breakout palsu secara efektif

Analisis Risiko

-

Sistem rata-rata bergerak rentan menghasilkan sinyal palsu, memerlukan indikator bantu untuk menyaring

-

Parameter indikator RSI perlu dioptimalkan, jika tidak dapat melewatkan titik beli/jual

-

Indikator TSV juga sensitif terhadap parameter, perlu diuji secara cermat

-

Breakout di atas pita atas Bollinger bisa jadi merupakan breakout palsu, perlu diverifikasi

-

Kombinasi banyak indikator membuat optimasi parameter sulit, rentan terhadap overfitting

-

Data pelatihan dan pengujian yang tidak memadai dapat menyebabkan kurva fitting

Arah Optimasi

-

Uji lebih banyak parameter periode untuk menemukan kombinasi parameter terbaik

-

Coba indikator lain seperti MACD, KD sebagai pengganti atau kombinasi dengan RSI

-

Optimasi parameter harus memanfaatkan analisis walk forward secara penuh

-

Tambahkan strategi stop loss untuk mengontrol kerugian per transaksi

-

Pertimbangkan untuk menambahkan model pembelajaran mesin untuk membantu penilaian sinyal

-

Sesuaikan parameter untuk pasar yang berbeda, jangan terlalu bergantung pada satu kombinasi parameter

Kesimpulan

Strategi ini menangkap tren jangka panjang dan jangka pendek melalui sistem rata-rata bergerak ganda, sambil menggunakan berbagai indikator seperti RSI, TSV, dan Bollinger Bands untuk menyaring sinyal. Keunggulan strategi adalah dapat mengikuti tren dan menangkap gelombang kenaikan jangka panjang. Namun, ada juga risiko sinyal palsu tertentu, yang memerlukan optimasi parameter lebih lanjut dan pengendalian stop loss untuk mengurangi risiko. Secara keseluruhan, strategi ini menggabungkan pelacakan tren dan indikator pembalikan, efektif di pasar naik jangka panjang, tetapi perlu penyesuaian parameter untuk pasar yang berbeda.

- 1