Strategi Trading Kuantitatif yang Menggabungkan Tren dan Osilasi

Ikhtisar

Strategi Dual Trend Oscillator adalah strategi trading kuantitatif yang menggabungkan tren dan osilasi. Strategi ini menggunakan kombinasi dua indikator untuk mengidentifikasi arah dan kekuatan tren, serta mencari waktu masuk yang optimal saat tren berosilasi.

Prinsip Strategi

Strategi ini terutama memanfaatkan dua indikator publik: Trend Surfers dan Mawreez's Trend Oscillator.

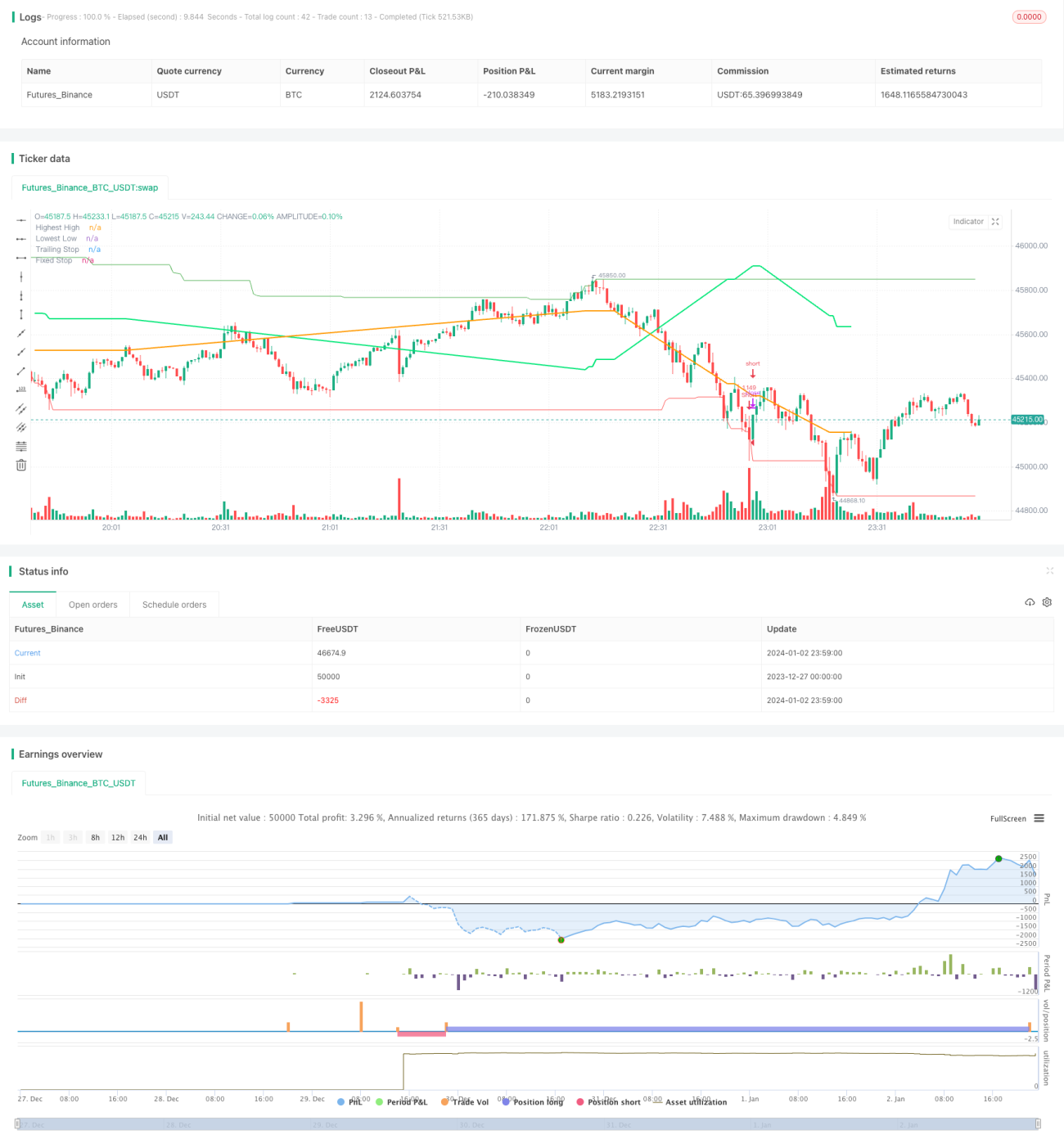

Trend Surfers adalah indikator stop loss yang mengikuti tren. Indikator ini menghitung harga tertinggi dan terendah dalam periode tertentu untuk menilai pergerakan harga dan memberikan posisi stop loss yang disarankan. Misalnya, ketika harga menembus harga tertinggi dari 168 candle terakhir, itu adalah sinyal bullish; ketika harga menembus harga terendah dari 168 candle terakhir, itu adalah sinyal bearish.

Mawreez's Trend Oscillator adalah indikator osilasi dua garis. Mirip dengan MACD, indikator ini menggunakan selisih DI untuk menentukan arah dan kekuatan tren. Ketika garis indikator berada di atas garis 0, itu adalah bullish; di bawah garis 0, itu adalah bearish.

Aturan trading strategi ini adalah:

- Masuk posisi long: ketika Trend Surfers menembus garis tertinggi dan indikator Mawreez's Trend Oscillator menunjukkan bullish, beli.

- Masuk posisi short: ketika Trend Surfers menembus garis terendah dan indikator Mawreez's Trend Oscillator menunjukkan bearish, jual.

Metode stop loss adalah kombinasi trailing stop loss dan fixed stop loss.

Analisis Keunggulan

Strategi ini menggabungkan indikator tren dan osilasi, sehingga mampu menangkap tren sekaligus mencari harga masuk yang lebih baik saat osilasi. Keunggulannya antara lain:

- Filter ganda dari dua indikator efektif menghindari false breakout.

- Menggabungkan tren dan osilasi memudahkan untuk menangkap akumulasi di zona rendah atau pelepasan beban di zona tinggi saat harga berada dalam kisaran osilasi.

- Menggunakan beberapa metode stop loss untuk mengontrol risiko dengan baik.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

- Kombinasi dua indikator rentan menyebabkan missed signal (kehilangan sinyal).

- Indikator tren dan osilasi dapat menghasilkan sinyal yang bertentangan.

- Fixed stop loss dapat menyebabkan stop loss terlalu dini.

Untuk mengatasi risiko ini, langkah-langkah berikut dapat diambil:

- Melonggarkan parameter indikator secara tepat untuk mengurangi tingkat penyaringan.

- Menambahkan aturan penentuan tren untuk menghindari konflik indikator.

- Menyesuaikan posisi stop loss secara dinamis.

Arah Optimasi

Strategi ini masih memiliki ruang untuk optimasi lebih lanjut:

- Menguji berbagai kombinasi parameter dan periode untuk menemukan parameter terbaik.

- Menambahkan aturan bantu seperti volatilitas, volume perdagangan, dll.

- Menggunakan teknik machine learning untuk mengoptimalkan indikator dan parameter secara dinamis.

Kesimpulan

Strategi Dual Trend Oscillator secara komprehensif memanfaatkan keunggulan indikator pengikut tren dan osilasi. Strategi ini dapat mengidentifikasi arah tren sekaligus menangkap peluang osilasi. Melalui optimasi parameter dan aturan, profitabilitas strategi dapat ditingkatkan lebih lanjut. Strategi ini memiliki prospek pengembangan yang baik.

- 1