追跡型ブレイクアウト戦略

概要

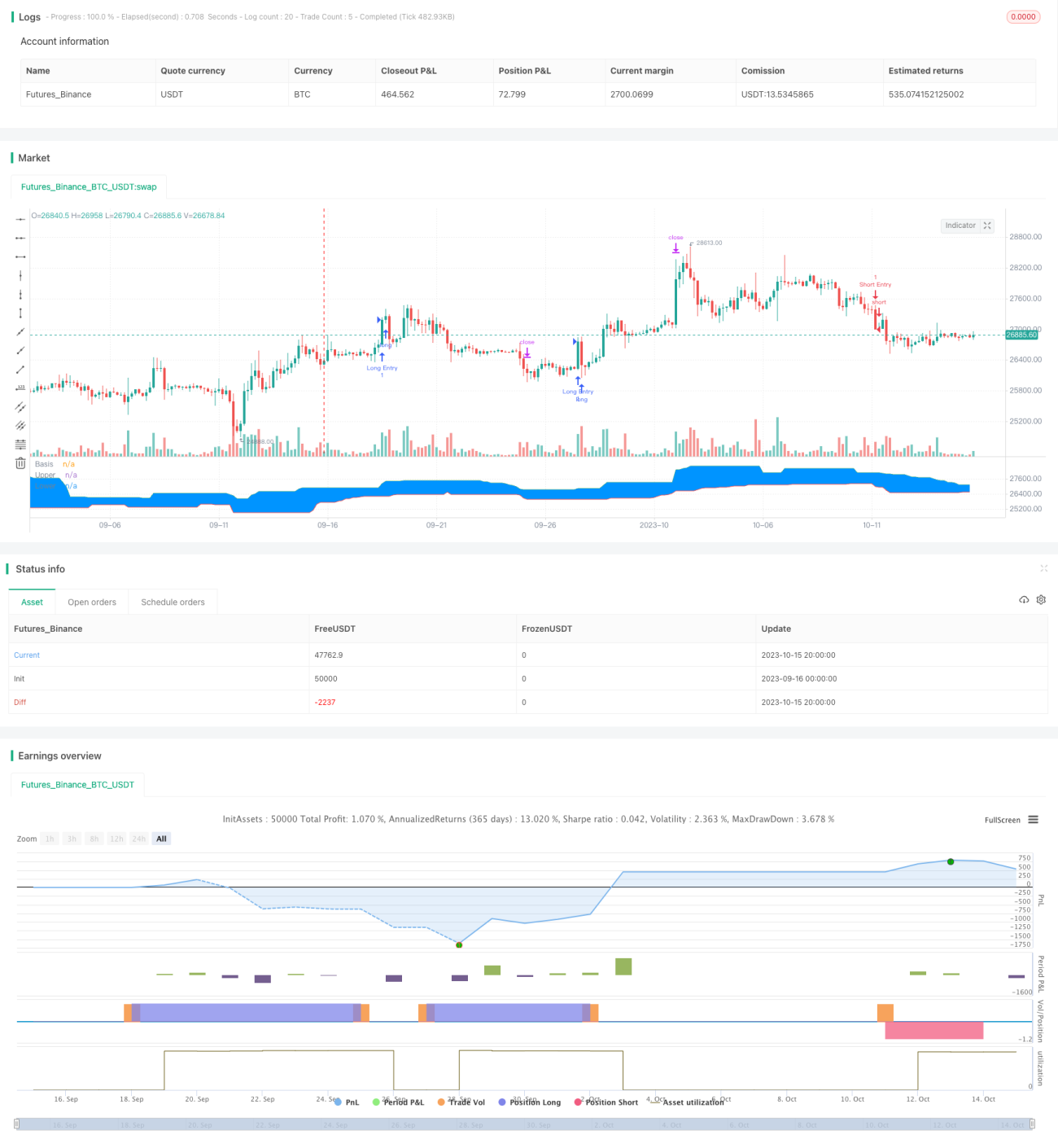

本戦略は主に「ドンチャンチャンネル」指標を使用して、トレンドフォロー型のブレイクアウト戦略を実現します。この戦略はトレンドとブレイクアウトの2つの取引アイデアを組み合わせ、長期的なトレンド判断に基づいて、より短い周期のブレイクアウトポイントを探してエントリーし、トレンド相場での順張り取引を実現します。さらに、ストップロスとテイクプロフィットの水準を設定し、各取引のリスクリワード比をコントロールします。全体的に、この戦略はトレンドを追跡する利点を持ち、流れに乗って長期的なトレンドの機会を捉えることができます。

戦略の原理

-

「ドンチャンチャンネル」指標のパラメータを設定します。デフォルト期間は20。

-

EMA平滑移動平均線を設定します。デフォルト期間は200。

-

リスクリワード比を設定します。デフォルトは1.5。

-

ブレイクアウト後の押し目(リトレースメント)パラメータを、ロングとショートそれぞれに設定します。

-

前回のブレイクアウトが高値か安値かを記録します。

-

ロングシグナル:前回のブレイクアウトが安値であり、かつ価格がドンチャンチャンネルの上限(アッパーバンド)を上回り、かつEMA平均線を上回った場合、ロングシグナルを生成します。

-

ショートシグナル:前回のブレイクアウトが高値であり、かつ価格がドンチャンチャンネルの下限(ロワーバンド)を下回り、かつEMA平均線を下回った場合、ショートシグナルを生成します。

-

ロングポジションに入った後、ストップロスをドンチャンチャンネルの下限から5ポイント(pips)下げた位置に設定し、テイクプロフィットをリスクリワード比×ストップロス幅に設定します。

-

ショートポジションに入った後、ストップロスをドンチャンチャンネルの上限から5ポイント上げた位置に設定し、テイクプロフィットをリスクリワード比×ストップロス幅に設定します。

この方法により、戦略はトレンド判断とブレイクアウト操作を組み合わせ、流れに乗りながら長期的なトレンドの中でより短い周期の機会を捉えます。同時に、ストップロスとテイクプロフィットの設定により、一取引あたりのリスクリワード状況をコントロールできます。

優位性の分析

-

長期的なトレンドを追跡し、流れに乗ることで逆張り取引を避けます。

-

ドンチャンチャンネルは長期指標として、EMA移動平均線によるフィルターと組み合わせることで、トレンドの方向性を良好に判断できます。

-

ストップロスとテイクプロフィットのメカニズムにより各取引のリスクをコントロールし、損失を制限できます。

-

リスクリワード比を最適化することで、損益比を拡大し、超過収益を追求できます。

-

バックテストのパラメータ設定が柔軟で、異なる市場に合わせて最適なパラメータの組み合わせを調整できます。

リスク分析

-

ドンチャンチャンネルとEMA移動平均線をフィルター指標として使用すると、誤ったシグナルを発する可能性があります。

-

ブレイクアウト取引は騙し(フェイクアウト)に遭いやすいため、明確なトレンド背景を特定する必要があります。

-

ストップロスとテイクプロフィットの距離が固定されており、市場の変動度合いに応じて調整できません。

-

パラメータの最適化余地が限られており、実運用での効果を保証できません。

-

取引システムはランダムなイベントに耐えられず、ブラックスワン現象により大きな損失が発生する可能性があります。

最適化の方向性

-

オシレーター系指標など、さらに多くの指標を追加してフィルタリングし、シグナルの品質を向上させることが考えられます。

-

市場の変動度合いやATR指標に基づいて、損益ポジションを動的に調整するスマートストップロス・テイクプロフィットを設定できます。

-

機械学習などの手法を用いてパラメータをテスト・最適化し、実際の市場により適合させることができます。

-

エントリーロジックを最適化し、出来高やボラティリティ指標を補助条件として追加することで、罠を回避できます。

-

トレンドフォロー戦略や機械学習との組み合わせを検討し、ハイブリッド戦略として安定性を高めることができます。

まとめ

本戦略はトレンドフォロー型ブレイクアウト戦略として、長期的なトレンドを判断した上で、ブレイクアウトをシグナルとして順張りし、ストップロスとテイクプロフィットを設定して一取引あたりのリスクをコントロールするという考え方が中核です。この戦略には一定の優位性がありますが、改善の余地もあります。全体として、パラメータ設定やエントリータイミングの選択などの問題を適切に処理し、他の技術で補強できれば、実用的なトレンドフォロー戦略となり得ます。しかし、投資家はどんな取引システムも市場リスクを完全に回避することはできないため、リスク管理を徹底する必要があることを覚えておくべきです。

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1