二線追跡アルゴリズム取引戦略

概要

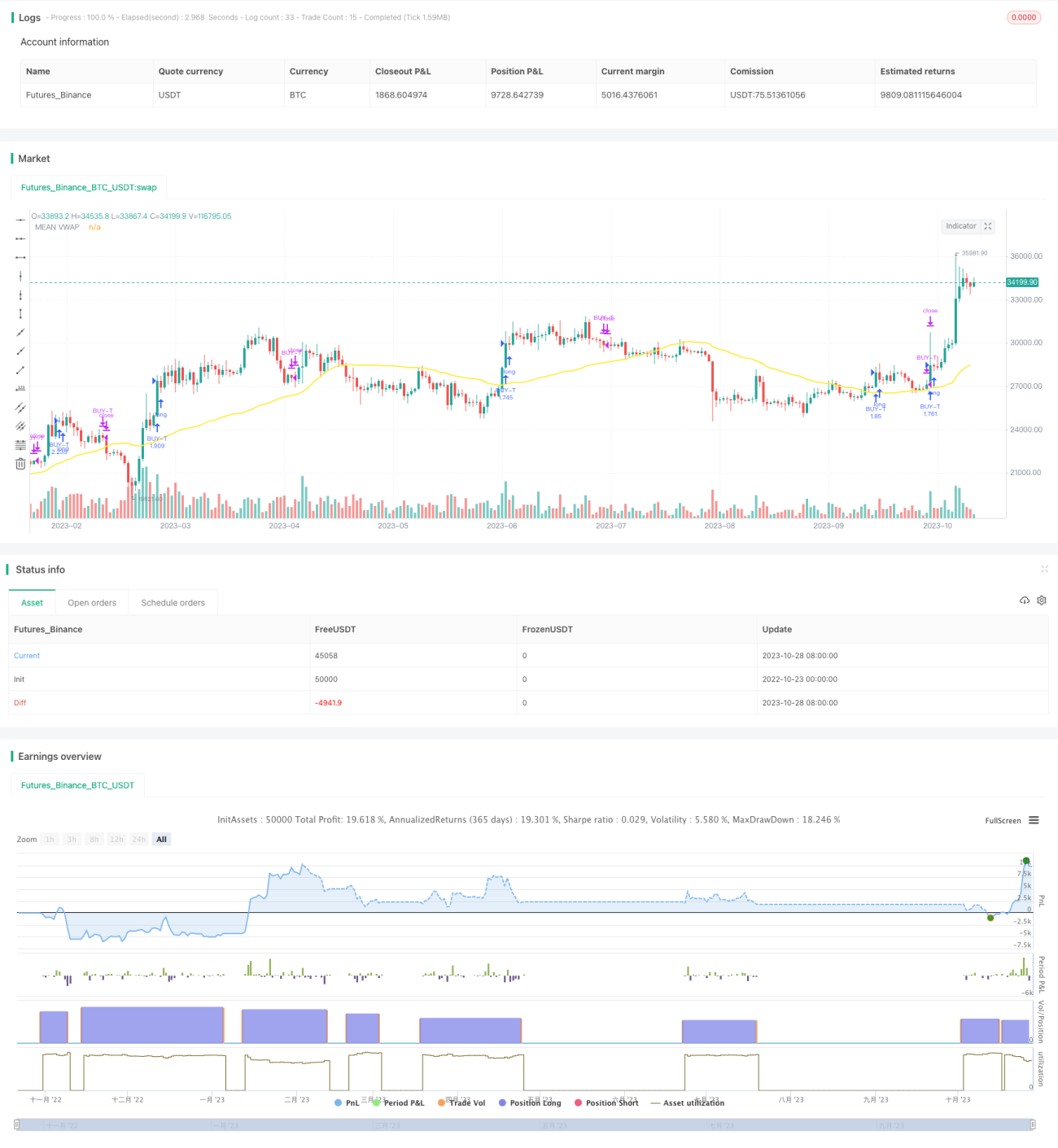

本戦略は主に移動平均線のクロス原理を利用し、RSI指標の反転シグナル、およびカスタムの二線追跡アルゴリズムを組み合わせて移動平均線クロス追跡取引を実現します。戦略は異なる周期の二本の移動平均線のクロスを追跡し、一方の短期移動平均線が短期トレンドを、もう一方の長期移動平均線が長期トレンドを追跡します。短期移動平均線が長期移動平均線を上抜けた場合、短期トレンドが上向きであることを示し、買いシグナルとなります。短期移動平均線が長期移動平均線を下抜けた場合、短期トレンドの終了を示し、ポジションを決済します。

戦略の原理

-

異なるパラメータの2組のVWAP移動平均線を計算し、それぞれ長期トレンドと短期トレンドを表します。

- 長期トレンドを計算するためのスロー天幕線と基準線

- 短期トレンドを計算するためのファスト天幕線と基準線

-

各組の天幕線と基準線の平均値をそれぞれスロー移動平均線とファスト移動平均線とします。

-

ボリンジャーバンド指標を計算し、レンジ相場とブレイクアウトを判断します。

- 中央線はファスト移動平均線とスロー移動平均線の平均値

- ボリンジャーバンドの上限・下限はブレイクアウトの判断に使用

-

TSV指標を計算し、出来高のエネルギーを判断します。

- TSVが0より大きい場合、上昇力が下降力より強いことを示す

- TSVがそのEMAより大きい場合、力が強まっていることを示す

-

RSI指標を計算し、買われすぎ・売られすぎを判断します。

- RSIが30未満は売られすぎゾーンで、買いシグナル

- RSIが70超は買われすぎゾーンで、売りシグナル

-

エントリー条件:

- ファスト移動平均線がスロー移動平均線を上抜ける

- 終値がボリンジャーバンドの上限を上抜ける

- TSVが0より大きく、かつそのEMAより大きい

- RSIが30未満

-

エグジット条件:

- ファスト移動平均線がスロー移動平均線を下抜ける

- RSIが70超

優位性分析

-

二本の移動平均線システムを使用することで、長期・短期両方のトレンドを同時に捉えられる。

-

RSI指標により、買われすぎゾーンでの買い、売られすぎゾーンでの売りを回避できる。

-

TSV指標により、トレンドを支える十分な出来高が確保されていることを確認できる。

-

ボリンジャーバンドを利用して、重要なブレイクアウトポイントを判断できる。

-

複数の指標を組み合わせることで、偽のブレイクアウトを効果的にフィルタリングできる。

リスク分析

-

移動平均線システムは誤ったシグナルを発生しやすいため、補助指標によるフィルタリングが必要。

-

RSI指標のパラメータは最適化が必要であり、適切でないと売買ポイントを逃す可能性がある。

-

TSV指標もパラメータに敏感で、入念なテストが必要。

-

ボリンジャーバンド上限のブレイクアウトは偽のブレイクアウトである可能性があり、検証が必要。

-

複数の指標を組み合わせることでパラメータ最適化が難しく、過剰最適化のリスクがある。

-

トレーニングデータとテストデータが不十分だと、カーブフィッティングを引き起こす可能性がある。

最適化の方向性

-

より多くの周期パラメータをテストし、最適なパラメータの組み合わせを探す。

-

MACD、KDなどの他の指標をRSIの代わりに、または組み合わせて試す。

-

パラメータ最適化にはwalk forward分析を十分に活用する。

-

ストップロス戦略を追加し、一取引あたりの損失を抑制する。

-

機械学習モデルを導入してシグナル判断を補助することを検討する。

-

異なる市場に合わせてパラメータを調整し、単一のパラメータ組み合わせに過度に依存しない。

まとめ

本戦略は二本の移動平均線システムによって長期・短期トレンドを捉え、同時にRSI、TSV、ボリンジャーバンドなどの複数の指標でシグナルをフィルタリングします。戦略の利点はトレンドに乗り、長期上昇相場を捉えられることです。しかし、ある程度の偽シグナルのリスクも存在し、さらなるパラメータ最適化とストップロスによるリスク低減が必要です。総じて、本戦略はトレンドフォローと反転指標を組み合わせたもので、長期上昇相場において良好な効果を発揮しますが、異なる市場に応じてパラメータを調整する必要があります。

- 1