トレンドブレイクアウトと移動平均線フォロー戦略

概要

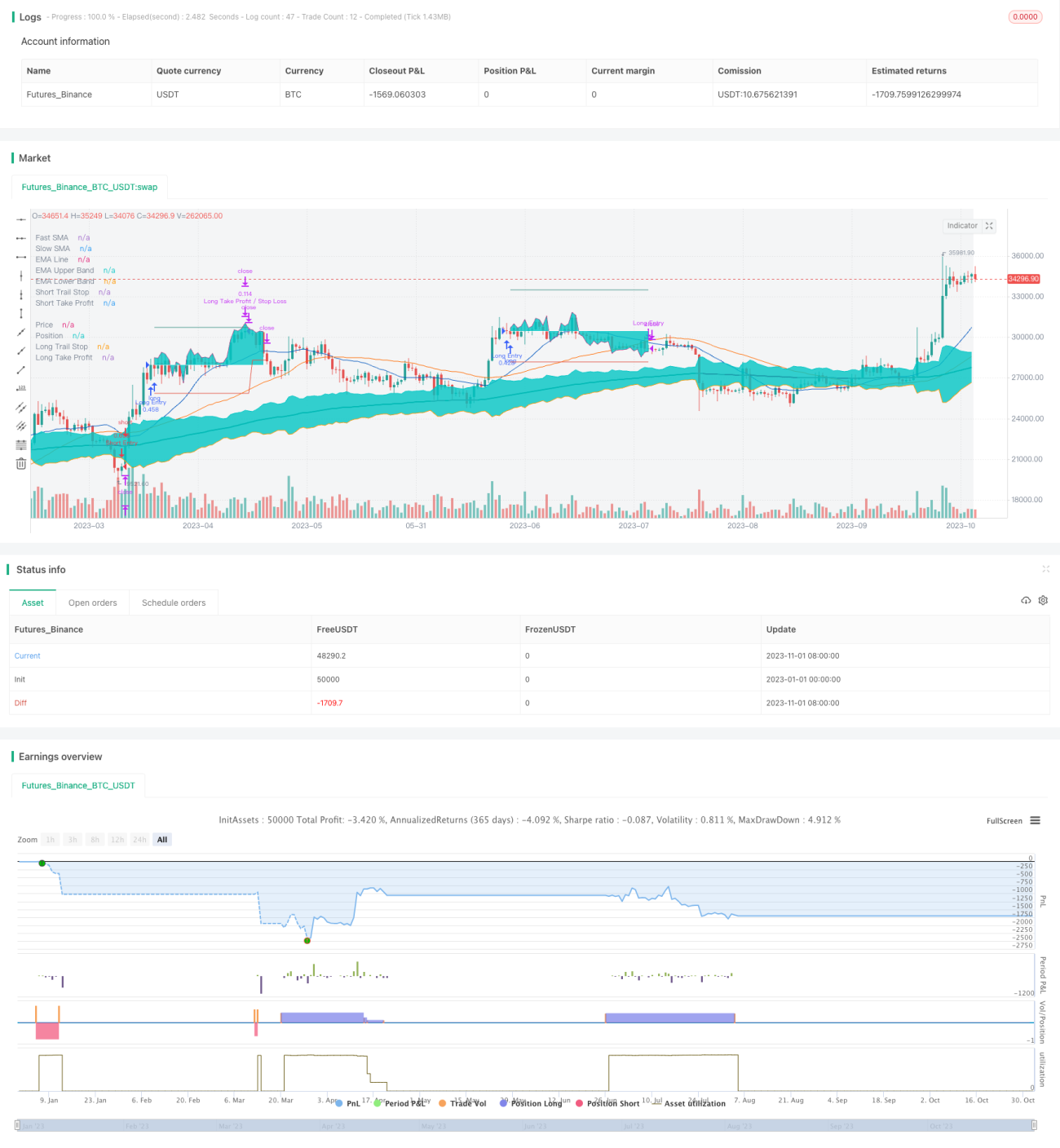

この戦略は、単純移動平均線のゴールデンクロスとデッドクロスを利用してトレンド方向を判断し、トレンドの開始時にフルポジションで買いまたは売りを行い、損切りと利確注文を設定してリスクを管理します。エントリー後は移動平均線を使って継続的にトレンドを追跡し、トレンドが逆行した場合には迅速に損切りを行います。この戦略には設定可能な損切り、利確、ポジション管理モジュールが備わっており、パラメータを柔軟に調整できるため、異なる銘柄に適用可能です。

戦略の原理

この戦略は主に単純移動平均線のゴールデンクロスとデッドクロスを用いてトレンドの開始と終了を判断します。まず、短期SMA(例:21日線)と長期SMA(例:49日線)の関係からトレンド方向を判断します。短期線が長期線を下から上にクロスした場合、上昇トレンドに入ったと見なし、その時点で買いポジションを開きます。短期線が長期線を上から下にクロスした場合、下降トレンドに入ったと見なし、その時点で売りポジションを開きます。

エントリー後、戦略はリアルタイムで価格とSMAの関係を監視します。価格が上からSMAを下回った場合、上昇トレンドが終了したと見なし、買いポジションを決済します。価格が下からSMAを上回った場合、下降トレンドが終了したと見なし、売りポジションを決済します。

リスク管理のため、ポジションを開く際には同時にストップ注文と利確注文を発注します。損切りの距離はATRに基づいて設定し、利確の距離はパーセンテージまたはATRに基づいて選択可能です。ポジションを開いた後、ストップ注文はリアルタイムで価格を追跡し、トレンドフォローを実現します。利確注文が到達すると一部のポジションを決済し、残りのポジションはそのまま追跡を続け、最終的に全ポジションが決済されます。

この戦略にはポジション管理モジュールもあり、取引ごとの資金利用率を制限することで、1回の取引のリスクエクスポージャーを管理できます。また、最大ドローダウン設定により、戦略全体のリスクを制御できます。

戦略の利点

- 移動平均線の比較でトレンド方向を判断するため、原理がシンプルで理解しやすい

- エントリー後はリアルタイムでストップを追跡し、利益の大部分を確保できる

- 設定可能な損切り・利確方法により、異なる銘柄に応じて調整可能

- 1回の取引リスクが管理可能で、全額投入しない

- 最大ドローダウン設定により、戦略の総損失を制限できる

リスクと解決策

- ダブル移動平均線のクロスには一定の遅れが生じ、トレンド開始の最適なエントリーポイントを逃す可能性がある

- パラメータの調整を繰り返し、異なる期間の移動平均線の組み合わせをテストする必要がある

- 移動平均線のクロスには誤ったシグナルが一定数含まれ、エントリー精度は100%ではない

- トレーリングストップは突破される可能性があり、全利益を確定できない

- 適度にストップ距離を緩め、価格に一定の調整余地を与える必要がある

- 最大ドローダウン制限が保守的すぎると、上昇の機会を逃す可能性がある

- 最大ドローダウンの割合を適度に広げ、戦略により多くの許容範囲を与える

最適化の方向性

- 異なるパラメータの組み合わせを試し、最適な移動平均線の期間を選択する

- トレンド強度指標を追加し、エントリーの精度を高める

- ストップ戦略を最適化し、トレンド中にできるだけ高値追い・安値追いを行う

- 異なる利確戦略をテストし、最適な利確ポイントを選択する

- ポジション管理方法を最適化し、資金効率を高める

- 最大ドローダウン設定を調整し、リターンとリスクのバランスを取る

まとめ

この戦略は全体的に初心者にとって非常に適した入門戦略であり、原理がシンプルで理解・習得が容易です。同時に適度なリスク管理機能を備えており、大きな損失の確率を減らすことができます。パラメータ最適化により良好な結果を得ることができます。しかし、その本質的な欠陥から、高度に精確な操作は不可能です。初心者の練習用戦略として使用することをお勧めしますが、高い効率と高い勝率を求めるトレーダーには適していません。より良い取引結果を得るには、より強い予測能力を持つ戦略を探す必要があります。

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1