1

Follow

1802

Followers

概要

超一戦略は、超一インディケーターに基づいて取引判断を行うトレンドフォロー戦略です。この戦略では、超一インディケーターの転換線、基準線、および雲帯の関係を利用して現在のトレンド方向を判断し、価格の戻りを利用してエントリーします。

超一戦略は主に中長期のトレンド取引に適しており、大きなトレンドの中で利益を得ることができます。また、この戦略はトレンド識別能力に優れています。

戦略の原理

超一戦略は以下の要素を判断して取引方向を決定します。

- 転換線と基準線の関係: 転換線が上にある場合は強気、下にある場合は弱気

- 雲帯の色: 雲帯が緑色の場合は強気、赤色の場合は弱気

- 価格の戻り: 価格が転換線と基準線の外側に戻ってからエントリー

具体的には、戦略の取引シグナルは以下の通りです。

買いシグナル:

- 転換線が基準線より上

- 価格が転換線と基準線より上

- 転換線と基準線が雲帯より上

- 価格が転換線と基準線の下に戻る

売りシグナル:

- 転換線が基準線より下

- 価格が転換線と基準線より下

- 転換線と基準線が雲帯より下

- 価格が転換線と基準線の上に戻る

買い/売りシグナルが同時に満たされた場合、ポジション状況に応じてエントリーを行います。

優位性分析

超一戦略には以下の優位性があります。

- 超一インディケーターの組み合わせでトレンド方向を判断するため、精度が高い

- 転換線と基準線で中期・短期トレンドを明確に判断でき、雲帯で長期トレンドを判断できる

- 価格が転換線・基準線まで戻る条件により、偽のブレイクアウトによる損失を回避できる

- リスク管理は直近の最高値・最安値を用いてストップロスを設定するため、1回の損失を効果的に抑えられる

- リスクリワード比が合理的で、安定した収益を目指す

- 異なる時間枠で適用可能で、中長期のトレンド取引に適する

- 戦略の考え方が明確で理解しやすく、パラメータ最適化の余地が大きい

- 様々な市場環境で良好な結果が期待できる

リスク分析

超一戦略には以下のリスクも存在します。

- レンジ相場ではストップロスが頻繁に発動され、収益に影響を与える可能性がある

- トレンドが急変した場合、ポジションを迅速に反転できず損失が発生する可能性がある

- 設定したリスクリワード比がすべての銘柄に適しているわけではなく、対象に応じたパラメータ調整が必要

- 雲帯ブレイク後の上昇余地が限られている場合、利益が限られる可能性がある

- インディケーターのパラメータは繰り返しテストと最適化が必要で、パラメータ調整が頻繁な銘柄には不向き

以下の方法でリスクを低減できます。

- パラメータを最適化し、異なる時間枠や銘柄の特性に合わせる

- 他のインディケーターと組み合わせてエントリーシグナルをフィルターし、レンジ相場での偽ブレイクを避ける

- ストップロス位置を動的に調整し、発動確率を下げる

- 異なるリスクリワード比の設定をテストする

- チャートパターンなどを用いてトレンドシグナルの強弱を判断する

最適化の方向性

超一戦略は以下の点から最適化が可能です。

- 転換線と基準線のパラメータを最適化し、取引対象の特性に合わせる

- 雲帯のパラメータを最適化し、長期トレンドの判断精度を高める

- ストップロスアルゴリズムを最適化(ATRに基づくストップロスや動的ストップロスなど)

- 他のインディケーターと組み合わせてシグナルをフィルターし、誤エントリーの確率を減らす

- リスクリワード比の設定を最適化し、異なる銘柄や時間枠の特性に適応させる

- マーチンゲール方式でポジション管理を行い、相場の変動頻度に対応する

- 機械学習を用いてパラメータを最適化し、より高い安定性を実現する

- 異なる取引時間帯を設定し、夜間取引と日中取引の特徴に応じて調整する

まとめ

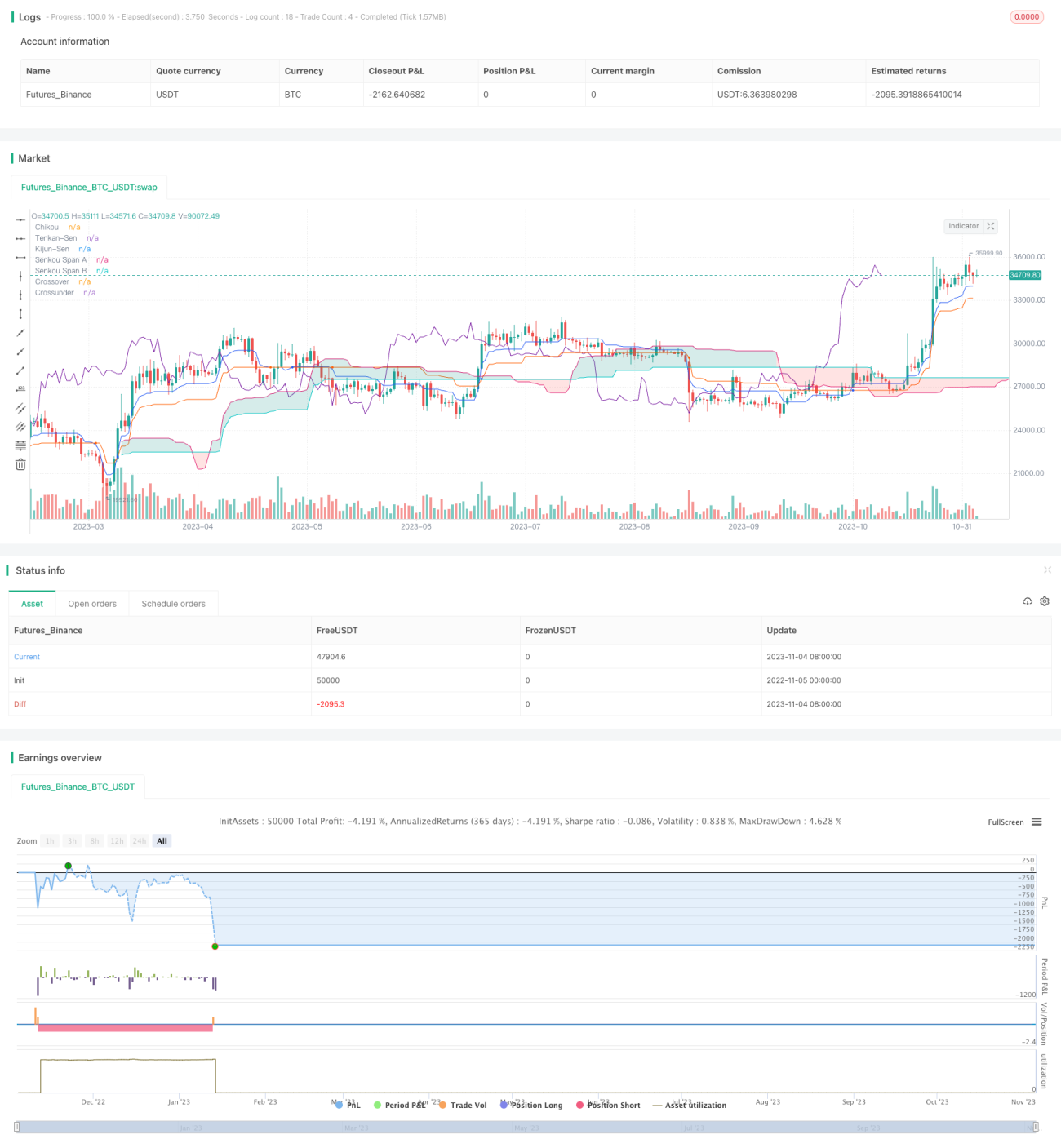

超一戦略は総合的に見て、中長期トレンド取引に非常に適した戦略です。超一インディケーターによるトレンド方向の判断力は明確で、価格の戻りを利用したエントリーにより誤エントリーを効果的に回避できます。パラメータ設定を最適化することで、より多くの銘柄や時間枠で安定した収益を達成できます。この戦略は理解しやすく、かつ最適化の余地が大きいため、戦略研究や学習の基礎戦略として適しています。

Source

Pine

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1