内部上昇率に基づくストップロスを用いたロングショートモメンタムブレイクアウト戦略

概要

本戦略は、異常な上昇を示すローソク足を識別し、現在の市場に突発的な一方向の相場が存在するかどうかを判断します。異常な上昇を示すローソク足が識別された場合、そのローソク足の高値付近に買い指値注文を設定し、同時に前のローソク足の安値付近にストップロス注文を設定することで、高レバレッジのリスク管理を伴うロングポジションを形成します。戦略はストップロスラインをリアルタイムで監視し、価格がストップロスラインを下回った場合、即座に注文をキャンセルして損切りを行います。

戦略の原理

本戦略は主に異常な上昇を示すローソク足の形成を判断します。close > open かつ high < high[1] かつ low > low[1] のローソク足が出現した場合、現在の期間に異常な上昇相場が存在すると見なします。このとき、ロングポジションのエントリーシグナルが発生し、エントリー価格は現在のローソク足の最高値付近とします。同時に、ストップロス価格は前のローソク足の最安値付近に設定し、高レバレッジのリスク管理モードを形成します。価格がストップロスラインを突破したかどうかを継続的に監視することで、リスク管理を実現します。

優位性分析

本戦略の最大の利点は、相場の短期的な異常な急騰相場を捉え、超高速取引を実現できることです。また、比較的大きなストップロス幅を設定することで、高レバレッジを活用したリスク管理取引を行い、より大きな利益を得ることが可能です。さらに、戦略はストップロスラインの自動監視を実現しており、価格がストップロスラインを下回った場合には迅速に損切りを行い、取引リスクを効果的にコントロールします。

リスク分析

本戦略の主なリスクは、異常な上昇の判断が不正確であり、相場の急騰を効果的に捉えられず、取引シグナルの誤判断確率が高いことです。また、ストップロス位置の設定も取引リスクと収益に大きな影響を与えます。ストップロスが緩すぎると取引損失のリスクが高まり、ストップロスが狭すぎると相場の上昇に追随して利益を得ることが難しくなります。バックテストを通じてストップロス位置を最適化する必要があります。

最適化の方向性

本戦略は以下の点から最適化が可能です。

-

異常な上昇の判断基準に、より多くの指標やディープラーニングモデルを導入し、戦略の取引シグナル判断精度を向上させることができます。

-

ストップロス位置の設定について、大量の統計分析と最適化分析を行い、取引リスクと収益レベルのバランスが取れたより適切なストップロス位置を見つけることができます。

-

出来高フィルターやレンジブレイクアウトの検証など、より多くの高頻度取引リスク管理メカニズムを導入し、損失を抱える確率を低減できます。

-

戦略のエントリー基準を調整し、異常な上昇を示すローソク足に限定せず、より多くの指標やモデルを組み合わせて判断を行い、多重検証メカニズムを形成することも可能です。

まとめ

本戦略は全体として典型的な高頻度取引戦略であり、短期ブレイクアウト型の戦略に分類されます。相場の突発的な異常変動を捉えることで超高速取引を実現します。同時に、ストップロスリスク管理と高レバレッジメカニズムを用いてリスクをコントロールします。本戦略には最適化の余地が大きく、複数の観点から調整・最適化を行うことで、最終的にはリスクを抑えつつ、より高い超高速取引収益を得ることを目指します。

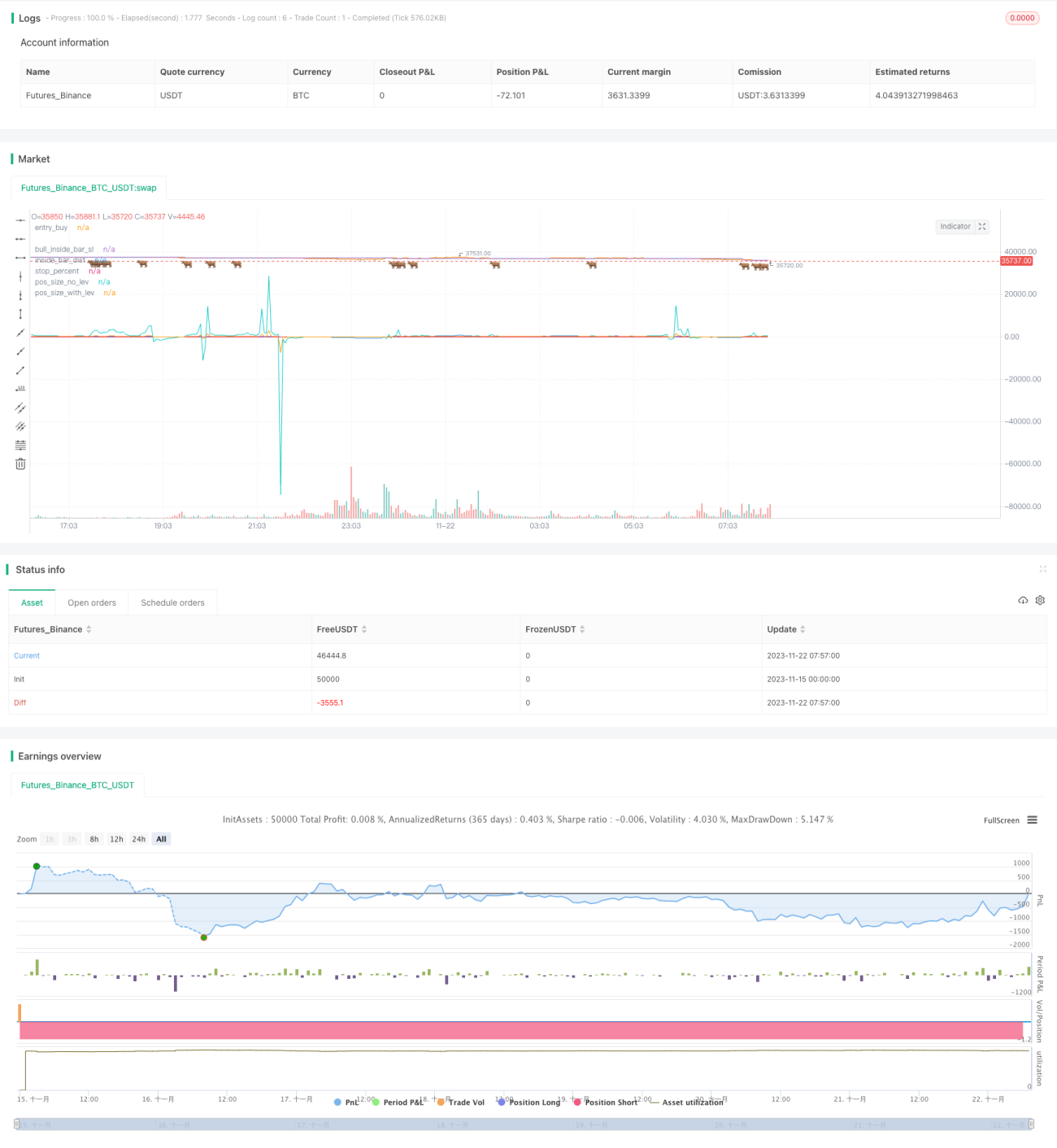

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 08:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// LOVE JOY PEACE PATIENCE KINDNESS GOODNESS FAITHFULNESS GENTLENESS SELF-CONTROL

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JoshuaMcGowan

// I needed to test/verify the functionality for canceling an open limit order in a strategy and also work thru the pieces needed to set the position sizing so each loss is a set amount. - 1