多因子モデル・モメンタム・リバーサル戦略

概要

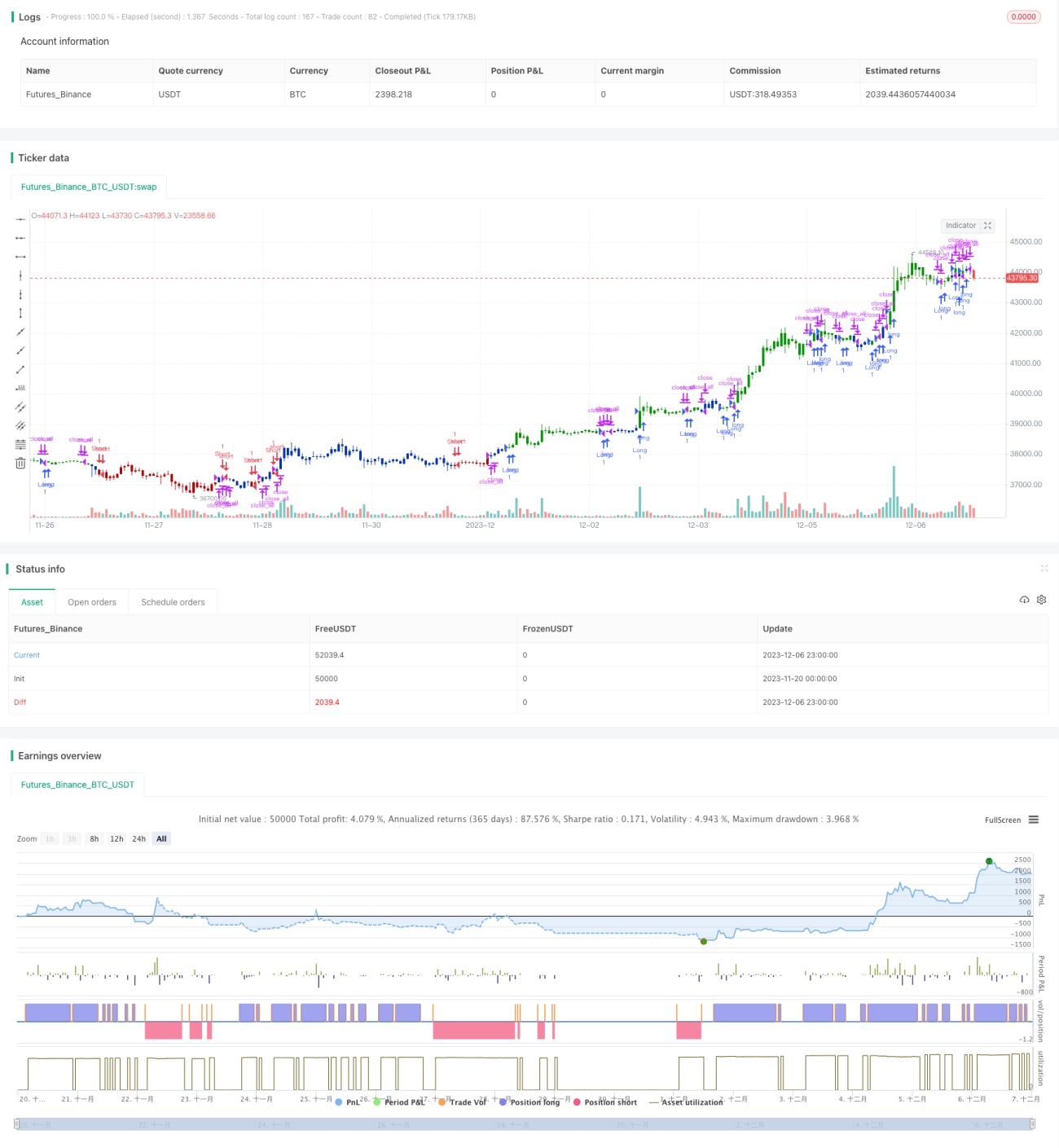

マルチファクターモデル・モメンタム・逆張り戦略は、マルチファクターモデルとモメンタム反転戦略を組み合わせることで、より安定した高いリターンを実現します。本戦略は、123逆張りと連響指標を2つの独立したシグナルとして使用し、両方のシグナルが一致したときにポジションを構築します。

戦略の原理

マルチファクターモデル・モメンタム・逆張り戦略は、123逆張り戦略と連響指標戦略の2つのサブ戦略から構成されます。

123逆張り戦略は、価格が2日連続で上昇または下落した際に、STOCH指標を用いて市場が過熱または過冷状態かを判断し、取引シグナルを生成します。具体的には、価格が2日連続で上昇し、かつ9日STOCHスローラインが50未満の場合に買いシグナル、価格が2日連続で下落し、かつ9日STOCHファストラインが50超の場合に売りシグナルとします。

連響指標戦略は、異なる期間の移動平均線とオシレーター系指標を重ね合わせることで、トレンドの方向性と強さを判断します。線形加重や正弦波の加算などの手法により、総合的に相場の強弱を判断します。この指標は等級分けされ、1~9が強い買い優勢、-1~-9が強い売り優勢を示します。

最終的に、戦略は両方のシグナルが一致した場合に、買いまたは売りポジションを選択します。

優位性の分析

マルチファクターモデル・モメンタム・逆張り戦略は、逆張りファクターと勢いファクターを組み合わせることで、反転の機会を捉えつつ、トレンドに乗り、偽のブレイクアウトを回避できるため、勝率が高くなります。戦略の優位性は具体的に以下の通りです。

- 123逆張り戦略は逆張りシグナル源として、短期的な反転による超過収益を捉えます。

- 連響指標はトレンドの方向性と強さを判断し、反転の余地が大きすぎることによる損失リスクを回避します。

- 両者を組み合わせることで、ある程度互いの長所を補完し、短所を補い、シグナルの品質を高めます。

- 単一モデルと比較して、マルチファクターの組み合わせは戦略の安定性を向上させます。

リスク分析

マルチファクターモデル・モメンタム・逆張り戦略には一定の優位性があるものの、以下のようなリスクも存在します。

- 反転が完了せず、価格が再び反転して下落することによる損失。適切にストップロスを設定することで防ぐことができます。

- 両方のシグナルが一致しない場合、方向性を確定できない。パラメータ調整により、両者の一致度を高めることが可能です。

- モデルが複雑でパラメータが多く、調整や最適化が容易ではない。

- 複数のサブモデルを同時に監視する必要があり、実運用での難易度と心理的負担が大きい。ある程度の自動売買要素を導入することで、運用負担を軽減できます。

最適化の方向性

マルチファクターモデル・モメンタム・逆張り戦略は、以下の点から最適化が可能です。

- 123逆張り戦略のパラメータ調整により、反転シグナルの精度と信頼性を高める。

- 連響指標のパラメータ調整により、判断するトレンドを実際のトレンドに近づける。

- 機械学習アルゴリズムを導入し、パラメータの組み合わせを自動最適化する。

- ポジション管理モジュールを追加し、ポジション調整をより定量化・体系化する。

- ストップロスモジュールを追加する。事前にストップロス価格を設定することで、1回の損失を効果的に管理する。

まとめ

マルチファクターモデル・モメンタム・逆張り戦略は、逆張りファクターと勢いファクターを総合的に活用し、高いシグナル品質を維持しつつ、マルチファクターの重ね合わせにより高い勝率を実現します。本戦略は、反転の機会を捉え、かつトレンドに乗るという二重の利点を持ち、効率的で安定した定量戦略です。今後は、パラメータ調整やリスク管理などの面から継続的に最適化することで、戦略のリスクリターン比をさらに向上させることができます。

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 11/11/2019

// This is combo strategies for get a cumulative signal. - 1