移動平均線多重階差トレンド追跡戦略

1

Follow

1802

Followers

概要

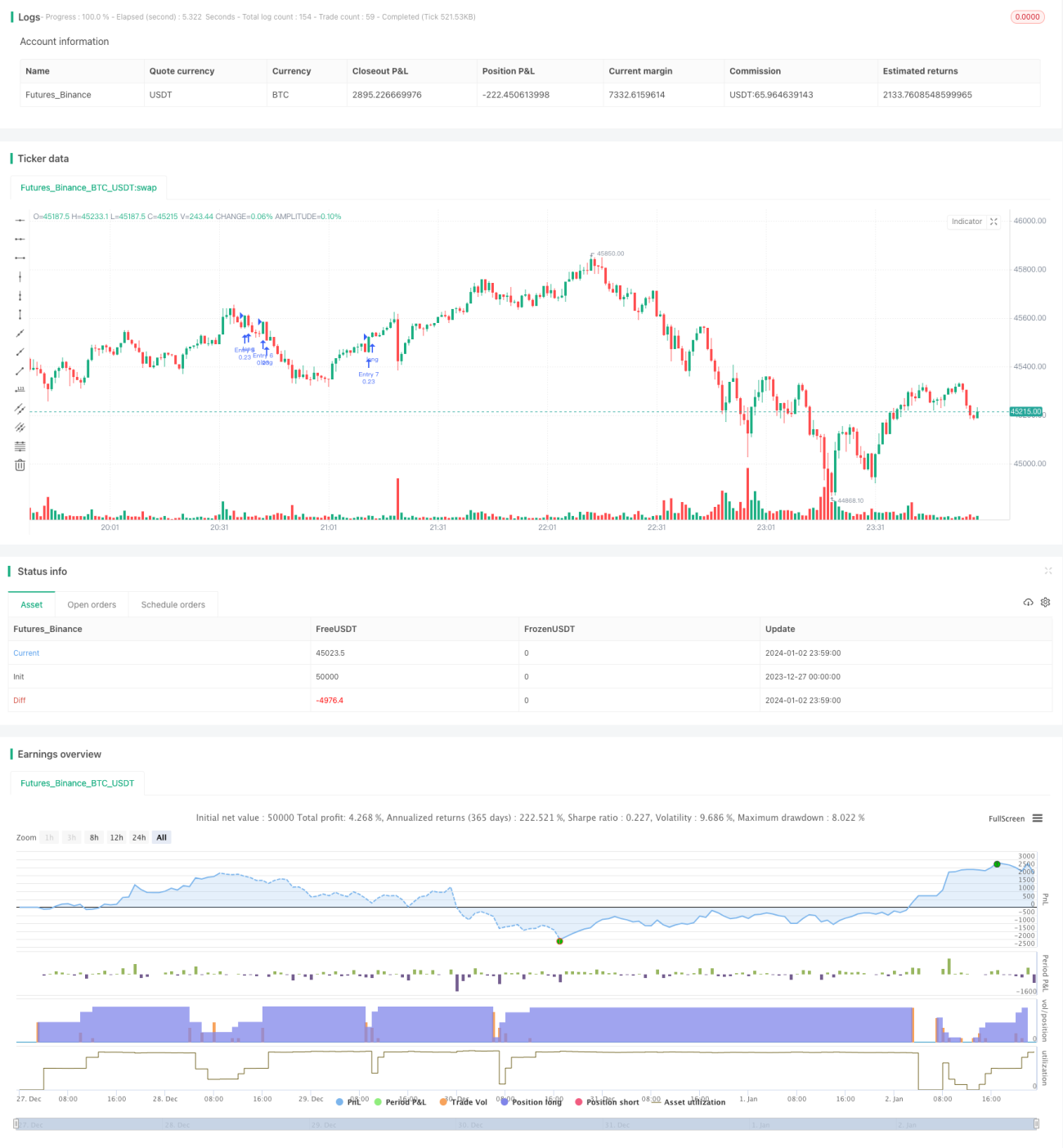

この戦略は移動平均線のマルチタイムフレーム差に基づき、中長期トレンドを追跡し、差別化ポジションの買い上がりモードを採用することで資金の指数関数的成長を実現します。戦略の最大の利点は、中長期トレンドを捉え、段階的に買い増しすることで超過収益を得られる点です。

戦略の原理

- 9日移動平均線、100日移動平均線、200日移動平均線に基づきマルチタイムフレームを構築します。

- 短期移動平均線が下から上へ長期移動平均線を突破したときに買いシグナルが発生します。

- 7段階の差別化ポジション買い上がりモードを採用し、新規ポジションを開くたびに前のポジションが満杯かどうかを判断し、すでに6ポジションある場合は追加しません。

- 各ポジションに固定利確・損切りポイント(3%)を設定し、リスク管理を行います。

以上が本戦略の基本的な取引ロジックです。

戦略の利点

- 中長期トレンドを効果的に捉え、相場の指数関数的成長を最大限享受できます。

- マルチタイムフレームの移動平均線を使用して差別化することで、短期的な市場ノイズに影響されにくくなります。

- 固定の利確・損切りポイントを設定することで、各ポジションのリスクを効果的に管理します。

- 差別化買い上がりモードを採用し、段階的にポジションを構築することで、トレンドの機会を捉え、超過収益を得られます。

戦略のリスクと解決策

- 打ち切られるリスクがあります。相場が転換した場合、タイムリーに損切りして退出できず、巨額の損失を被る可能性があります。解決策は、移動平均線の期間を短縮し、損切りの速度を速めることです。

- ポジションリスクがあります。突発的な事象により損失が許容範囲を超えた場合、追証やロスカットのリスクが生じます。解決策は、初期ポジション比率を適切に減らすことです。

- 過大な損失のリスクがあります。相場が急落した場合、差別化買い上がりが空売りに転換し、700%以上の損失が発生する可能性があります。解決策は、固定損切り比率を拡大し、損切り速度を速めることです。

戦略の最適化方向

- 異なるパラメータの移動平均線の組み合わせをテストし、より優れたパラメータを探すことができます。

- ポジション構築のポジション数を最適化できます。異なる差別化ポジション数をテストし、最適解を見つけます。

- 固定損切り・利確の設定をテストできます。利確範囲を適切に拡大し、より高い収益率を追求します。

まとめ

この戦略は全体的に相場の中長期トレンドを捉えるのに非常に適しており、段階的な買い増し方式を採用することで、リスク対収益比が極めて高い超過収益を得ることができます。同時に一定の操作リスクも存在するため、パラメータの調整などの方法で制御し、利益とリスクのバランスを見つける必要があります。全体的に、この戦略は実運用で検証する価値が十分にあり、実運用結果に基づいてさらに調整・最適化を行うことが推奨されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1