クオンツ二因子反転慣性取引戦略

概要

クォンツ・デュアルファクター・リバーサル・イナーシャ・トレーディング戦略(Quant Dual Factor Reversal Inertia Trading Strategy)は、価格反転シグナルと市場の慣性シグナルを組み合わせたクォンツ取引戦略です。本戦略はまずストキャスティクス指標を用いて価格反転シグナルを生成し、次に相対変動率指標(RVI)による市場の慣性シグナルと組み合わせて、最終的にデュアルファクター駆動の取引判断を実現します。

戦略の原理

本戦略は主に以下の2つの部分に基づいています。

-

価格反転部分は、ウルフ・イェンセン(Ulf Jensen)が著書で提唱した考え方を採用しています。具体的には、終値が2日連続で上昇し、かつ9日スローストキャスティクスが50未満の場合に買い建て、終値が2日連続で下落し、かつ9日ファストストキャスティクスが50を超える場合に売り建てます。

-

市場の慣性部分は相対変動率指標(RVI)を使用します。この指標の値は0から100の間で変動し、50を超えると市場の長期トレンドが上昇、50未満だと長期トレンドが下降であることを示します。

以上から、本戦略は価格反転シグナルと市場の慣性シグナルを統合し、最終的に現在の市場方向を判断します。両方のシグナルが一致した場合に取引シグナルが発生します。

優位性分析

本戦略の最大の利点は、反転とトレンドという2つの取引思考を組み合わせている点にあります。反転シグナルは短期的な調整を捉え、取引機会を提供します。慣性シグナルは長期トレンドが一致している場合にのみ建て玉を行うことを保証し、ノイズを効果的にフィルタリングできます。

また、デュアルファクター駆動によりシグナルの質が向上し、ストキャスティクス指標のパラメータ最適化やRVIの平滑化最適化が戦略改善の余地を提供します。

リスク分析

本戦略が直面する主なリスクは以下の通りです。

-

反転シグナルの識別が不正確になるリスク。パラメータが妥当かどうかを検証する必要があります。

-

慣性シグナルが誤ったシグナルを発するリスク。RVI指標自体にラグが生じるため、平滑化パラメータの調整が必要です。

-

デュアルファクターのシグナルタイミングが適切に一致せず、取引機会を逃すリスク。異なるパラメータ下での一致状況をテストする必要があります。

さらに、反転系戦略はトレンド相場において損失が拡大するリスクがあります。ストップロスルールを厳守する必要があります。

最適化の方向性

本戦略は以下の観点から最適化が可能です。

-

ストキャスティクス指標のパラメータを最適化し、反転シグナルの質と適時性を向上させる。

-

RVI指標の平滑化パラメータを最適化し、慣性判断の精度を高める。

-

異なる保有期間をテストし、最適な保有サイクルを決定する。

-

ストップロスメカニズムを追加する。異なるストップロスポイントでバックテストを行い、最適な位置を見つける。

-

出来高の変動などの他のファクターシグナルを追加し、マルチファクター駆動を形成することも検討できる。

まとめ

クォンツ・デュアルファクター・リバーサル・イナーシャ・トレーディング戦略は、反転とトレンドのファクターを総合的に考慮し、ストキャスティクス指標とRVI指標を用いて取引シグナルを生成します。本戦略はデュアルファクター駆動、反転機会の捕捉、シグナルフィルタリングなどの利点を持ち、多面的なパラメータ最適化によりさらに改善できます。リスク管理も非常に重要であり、ストップロスを厳格に実行する必要があります。本戦略はクォンツ取引に優れた考え方を提供します。

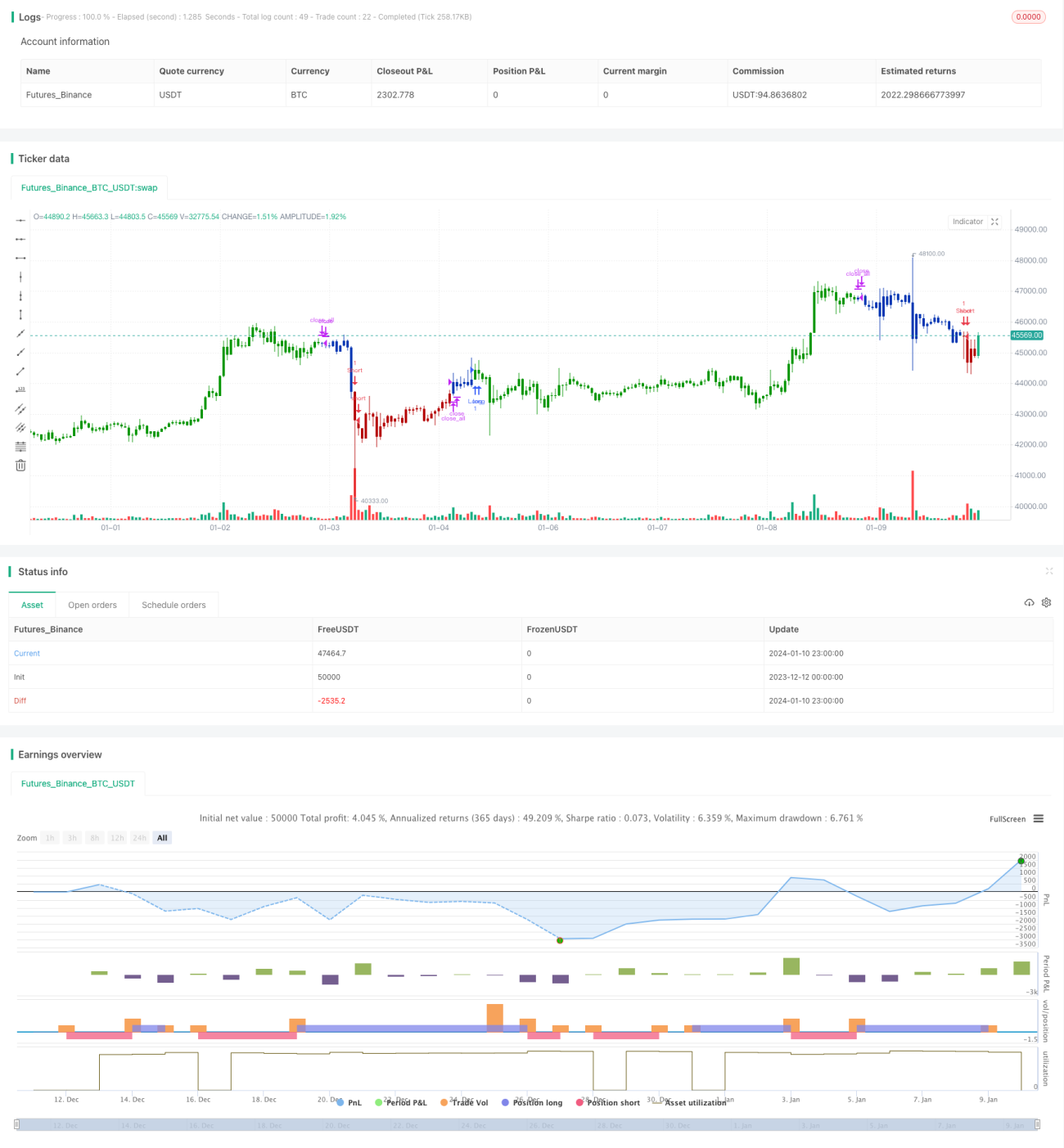

/*backtest

start: 2023-12-12 00:00:00

end: 2024-01-11 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 27/11/2020

// This is combo strategies for get a cumulative signal. - 1