1

Follow

1802

Followers

概要

双方向ADXトレーディング戦略は、平均方向性指数(ADX)インジケーターを活用して双方向取引を実現する定量戦略です。本戦略では、ADX指標とDIPlus・DIMinus指標の差を計算し、取引シグナルが発生するかどうかを判断するための閾値を設定することで、ロング・ショート両方向の取引を行い収益を上げます。

戦略の原理

- 真の変動幅(True Range)を計算

- 上昇方向性運動(Directional Movement Plus)と下降方向性運動(Directional Movement Minus)を計算

- 平滑化真の変動幅(Smoothed True Range)を計算

- 平滑化上昇方向性運動(Smoothed Directional Movement Plus)と平滑化下降方向性運動(Smoothed Directional Movement Minus)を計算

- DIPlus、DIMinus、ADX指標を計算

- DIPlusとADX、DIMinusとADXの差を計算

- ロング用とショート用の取引差値の閾値を設定

- 差値が閾値を超えた場合に取引シグナルが発生したと判断

- 買い注文と売り注文を発行

本戦略の中核は、ADXなどの方向性指数インジケーターを利用してトレンドの方向と強さを判断し、差値判定ルールを適用して閾値を設定し、自動取引を行うことです。

優位性分析

- ADXによるトレンド方向の判断で市場トレンドを正確に捉えられる

- 差値判定ルールの適用により、偽シグナルを効果的に除去できる

- 双方向取引により、ロング・ショート両方の機会を十分に捉えられる

- 完全自動取引で人手を介さない

- 戦略ロジックが明確で理解・修正が容易

リスク分析

- ADX指標には遅延が存在し、トレンドの転換点を見逃す可能性がある

- 双方向取引によりリスクが増大し、損失が拡大する可能性がある

- パラメータ設定が不適切だと過剰取引につながる恐れがある

- バックテストデータは実際の市場を再現できるわけではなく、実運用リスクは依然として存在する

解決策:

- 他の指標と組み合わせて取引シグナルを確認する

- パラメータを最適化し、取引頻度を制御する

- 厳格なポジションサイジングにより取引ポジションを管理する

最適化の方向性

- ADXパラメータを最適化し、感度を改善する

- 他の指標を追加してシグナルをフィルタリングする

- 機械学習アルゴリズムを適用してパラメータを最適化する

- 高度なストップロス戦略を利用して損失リスクを抑制する

- モデル予測と組み合わせてより正確な取引シグナルを得る

まとめ

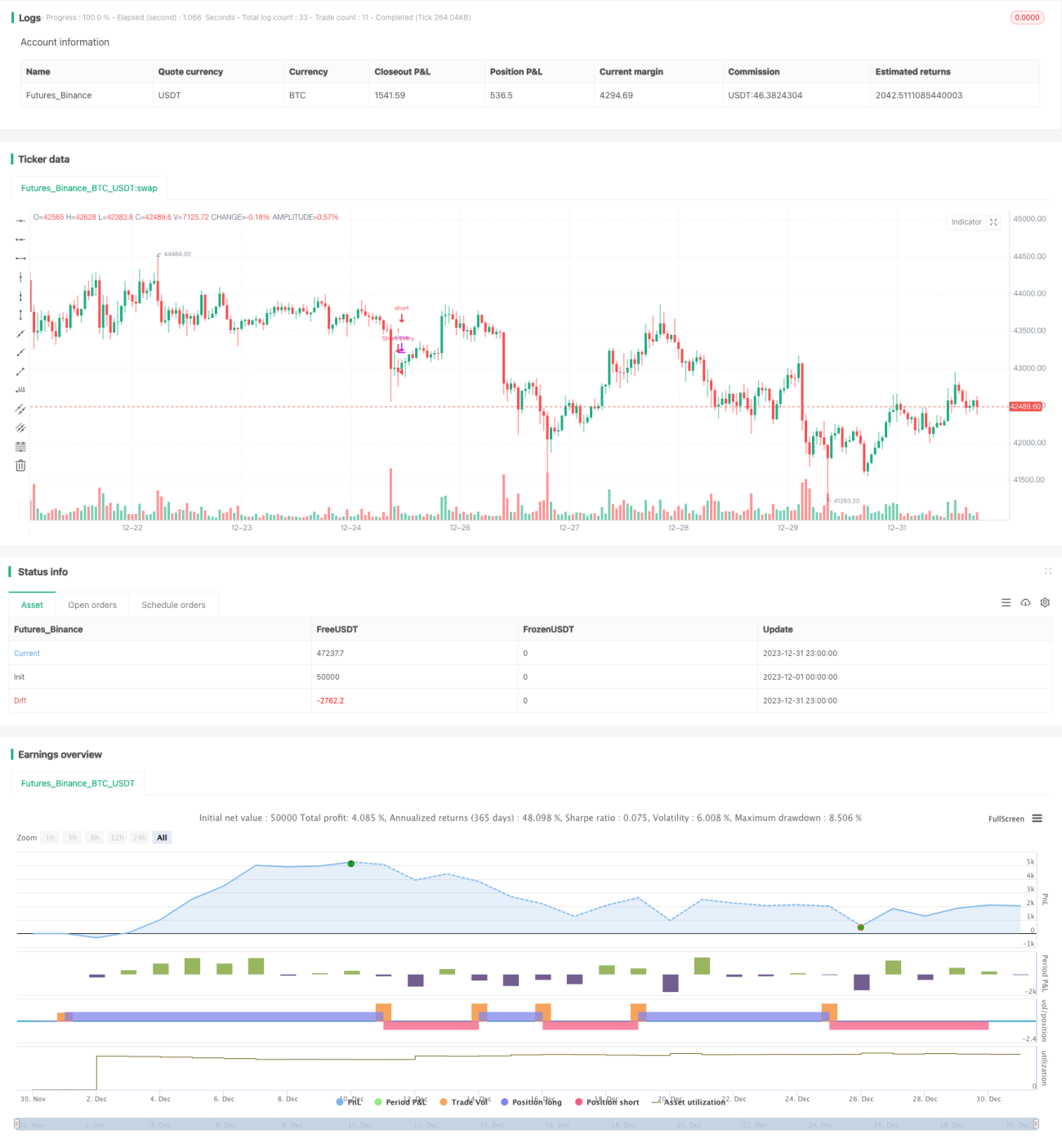

双方向ADXトレーディング戦略は、全体的に非常に実用的な定量戦略です。ADX指標を活用してトレンドを判断し、双方向で取引機会を捉えます。同時に差値判定を適用してシグナルの有効性を確保します。本戦略はロジックが明確でシンプルであり、修正や最適化が容易な双方向トレンドフォロー戦略です。適切なパラメータ最適化、ストップロス戦略の適用、シグナルフィルタリングにより、戦略の安定性と収益性をさらに向上させることができます。

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MAURYA_ALGO_TRADER

//@version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1