複数銘柄の動的平均線に基づくクォンツ取引戦略

概要

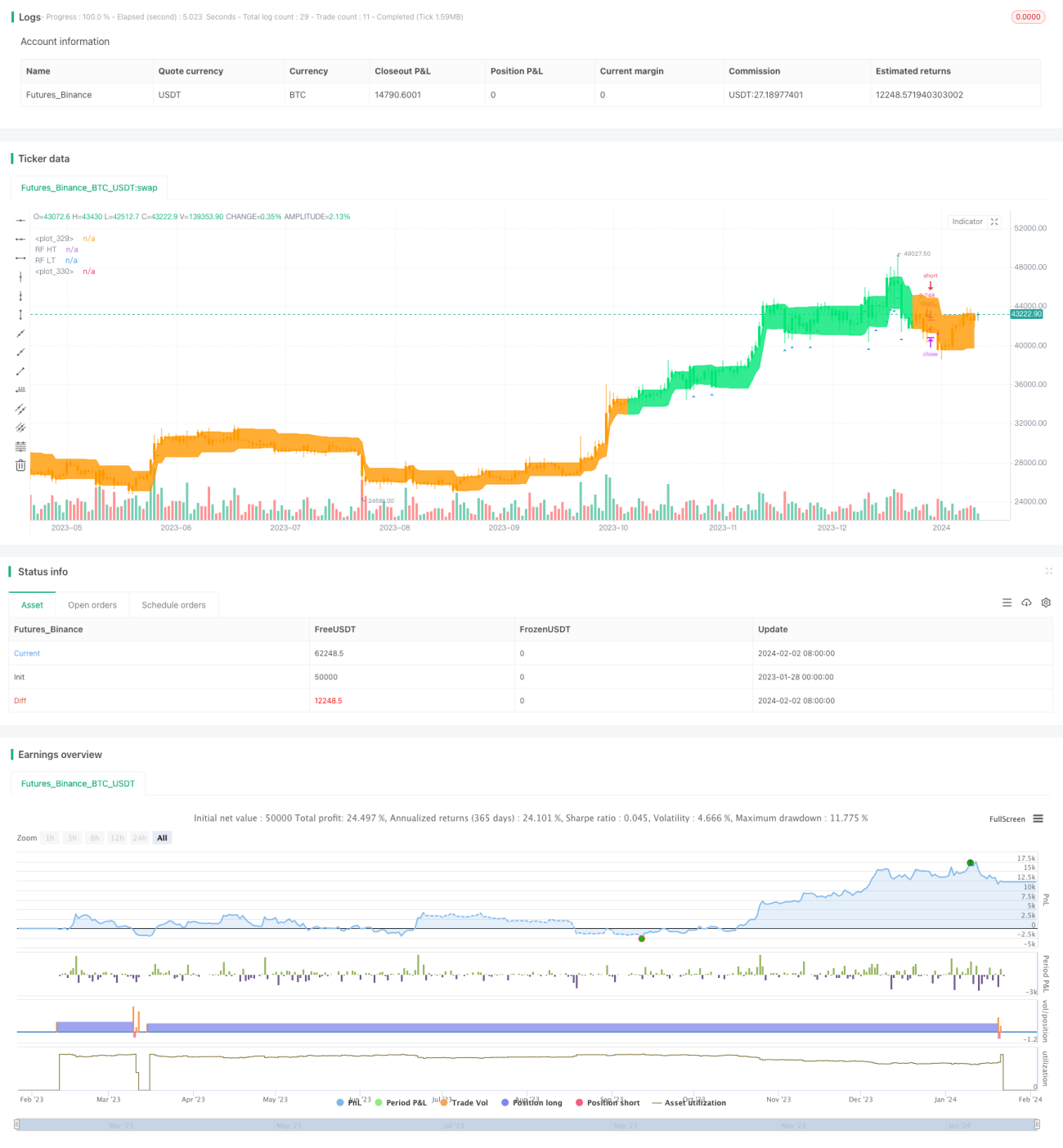

本戦略は、複数のテクニカル指標の組み合わせシグナルを利用して、株式や暗号資産などの対象資産の動的な取引を実現します。戦略は市場のトレンドを自動的に識別し、トレンドフォローを行います。同時に、ストップロス機構を導入してリスクを制御します。

戦略の原理

本戦略は主に移動平均線、相対力指数(RSI)、平均真のレンジ(ATR)、方向性指標(ADX)などの複数の指標を利用し、指標の組み合わせによって取引シグナルを生成します。

具体的には、まず二重移動平均線を用いてゴールデンクロス・デッドクロスのシグナルを形成します。短期線の長さは10日、長期線は50日です。短期線が下から上に長期線を突破したときに買いシグナル、短期線が上から下に長期線を割り込んだときに売りシグナルを生成します。この二重移動平均線システムは、中長期的なトレンドの転換を効果的に識別できます。

二重移動平均線に加えて、RSI指標を導入してトレンドシグナルを確認し、偽のブレイクアウトを回避します。RSIは短期線と長期線の差を用いて市場の強さを判断し、Lengthは14です。RSIが30を上抜けたときに買いシグナル、70を下抜けたときに売りシグナルを生成します。

さらに、ATR指標を利用してストップロス水準を自動調整します。ATR指標は市場の変動性を効果的に反映します。市場の変動が大きくなった場合、ストップロス水準を広く設定し、ストップロスに引っかかる可能性を低減します。

最後に、ADX指標でトレンドの強さを判断します。ADXは正の方向性指標DI+と負の方向性指標DI-の差を用いてトレンドの強さを判断します。ADX値が20を上抜けたときにトレンドが確立したと見なし、実際の取引シグナルを生成します。

複数の指標を組み合わせることで、戦略は取引シグナルを発する際により慎重になり、市場の偽シグナルに騙されるのを防ぎ、勝率を高めることができます。

戦略の優位性

本戦略には以下のような利点があります。

- 複数の指標の組み合わせにより、市場を総合的に判断し、意思決定の正確性を向上

移動平均線、RSI、ATR、ADXなどの複数の指標を組み合わせて利用することで、取引判断の正確性を高め、単一指標による誤判定を回避できます。

- ストップロスの自動調整によるリスク管理

市場の変動性に応じてストップロス水準を自動調整することで、ストップロスが発動する確率を低減し、取引リスクを効果的に制御します。

- トレンドの強さを判断し、逆張りを低減

ADX指標でトレンドの強さを判断してから実際に取引することで、逆張りによる損失を減らせます。

- パラメータ最適化の余地が大きい

本戦略の移動平均線の長さ、RSIの長さ、ATRの期間、ADXの期間などのパラメータは、異なる市場に応じて調整・最適化が可能で、適応性が高いです。

- 長期保有による利益の確保

長期・短期の移動平均線システムで長期トレンドを判断し、RSIなどの指標で短期的ノイズの影響を低減することで、トレンドの中で長期保有を行い、より高い収益を得ることができます。

リスクと対策

本戦略には以下のようなリスクも存在します。

- パラメータ最適化のリスク

多数のパラメータの組み合わせは最適化の難易度を高め、不適切なパラメータの組み合わせにより戦略のパフォーマンスが悪化する可能性があります。このリスクは、十分なバックテストとパラメータ調整によって軽減できます。

- 指標の無効化リスク

テクニカル指標はいずれも適用可能な市場状態があります。市場が特殊な状態に入った場合、戦略で使用する指標が同時に機能しなくなる可能性があります。このようなブラックスワン事象によるリスクには注意が必要です。

- 空売りポジションの損失リスク

戦略では空売り取引を許可しています。空売り取引は元々無限損失のリスクを伴います。このリスクはストップロスの設定によって低減できます。

- トレンド反転のリスク

トレンドが反転した場合、指標のシグナルは迅速に反応できず、逆方向の損失が発生しやすくなります。一部の指標パラメータを短縮し、感度を高めることで対応できます。

最適化のアイデア

本戦略にはさらなる最適化の余地があり、主な最適化のアイデアは以下の通りです。

- 適応型指標ウェイトの追加

異なる指標と市場状態の相関性を分析し、各指標のウェイトを動的に調整するメカニズムを設計することで、市場環境に応じた意思決定効果を向上させます。

- 深層学習モデルの補助的導入

深層学習などのモデルを用いて価格変動方向を予測し、人手による決定ルールを補助することで、戦略の意思決定の正確性を向上させます。

- パラメータの自動適応最適化

スライディングウィンドウの過去データに対して自動パラメータ最適化モジュールを設計し、指標パラメータの動的調整を実現し、戦略が市場変化にうまく適応できるようにします。

- 変動周期分析の導入

エリオット波動理論などの変動周期分析方法を追加し、トレンドの中長期的な動きを補助的に判断し、ポジション保有の利益確率を高めます。

まとめ

本戦略は、移動平均線、RSI、ATR、ADXなどの複数の指標を総合的に活用し、比較的完成度の高い一連の決定ルールを設計しました。移動平均線システムにより長期トレンドを判断しつつ、RSIなどの短期指標でノイズを低減できます。同時に、本戦略には大きな最適化の余地があり、より良いパフォーマンスが期待できます。総じて、本戦略は指標の組み合わせによって決定効果を高め、リスクを制御しており、さらなる研究と応用に値します。

- 1