ボリンジャーバンド+RSI+ADX+ATR反転取引戦略

1

Follow

1802

Followers

概要

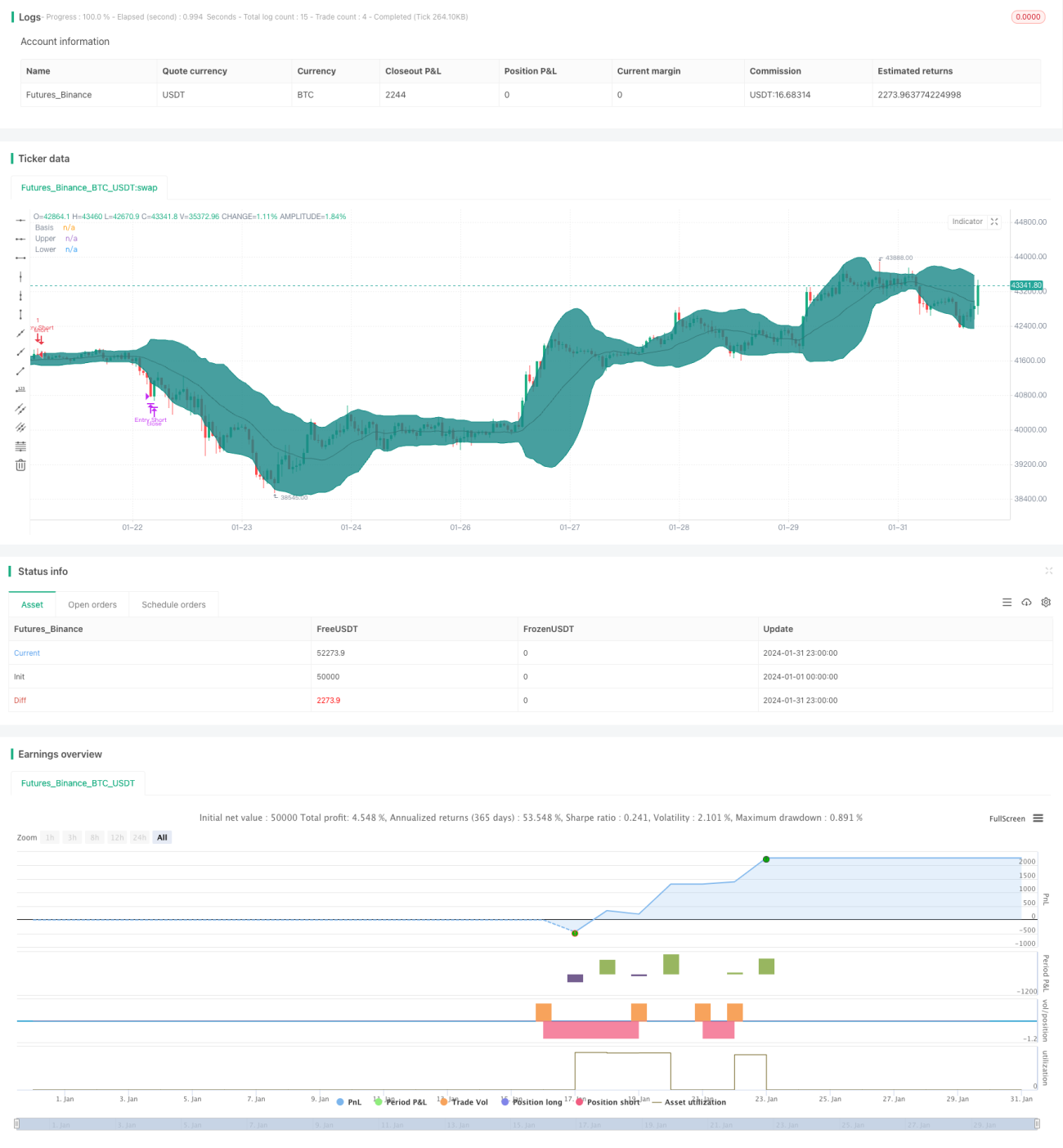

本戦略は複数のテクニカル指標を融合し、ボリンジャーバンドが価格の反転シグナルを発した際に、RSI・ADX・ATR指標を用いて市場構造を判断し、高確率な反転トレード機会を捉えます。

戦略の原理

- 20期間のボリンジャーバンドを使用し、価格が上限・下限バンドに到達した後、反転ローソク足が形成する売買シグナルを待ちます。

- RSI指標で市場がレンジ相場にあるかを判断します。RSIが60以上は強気圏、40以下は弱気圏とします。

- ADXが20未満の場合はレンジ相場、20以上の場合はトレンド相場と判断します。

- ATRによるストップロス設定およびトレーリングストップを適用します。

- EMA移動平均線を組み合わせてシグナルをフィルタリングします。

戦略の優位性分析

- 複数の指標を融合することで、高確率なトレードシグナルを生成します。

- パラメータを調整可能で、様々な市場環境に対応できます。

- ストップロスのルールが厳格で、リスクを効果的に管理できます。

戦略のリスク分析

- パラメータ設定が適切でない場合、取引が過剰になる可能性があります。

- 反転失敗の確率は依然として存在します。

- トレーリングストップが特定の市場では機能しない可能性があります。

戦略の最適化方向性

- より多くの指標の組み合わせをテストし、最適なパラメータ構成を模索します。

- ブレイクアウト失敗後、早期に継続的な反転機会を識別します。

- 異なるストップロス手法をテストし、よりスマートなストップロスを実現します。

まとめ

本戦略はボリンジャーバンドを基本トレードシグナルとしつつ、複数の補助指標による高確率なフィルタリングシステムと、比較的整ったストップロスルールを備えています。パラメータ調整や指標の最適化により、戦略のパフォーマンスをさらに向上させることが可能です。総じて、本戦略は信頼性の高い反転トレードシステムを構築しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1