取引心理のコントロールと均衡戦略

概要

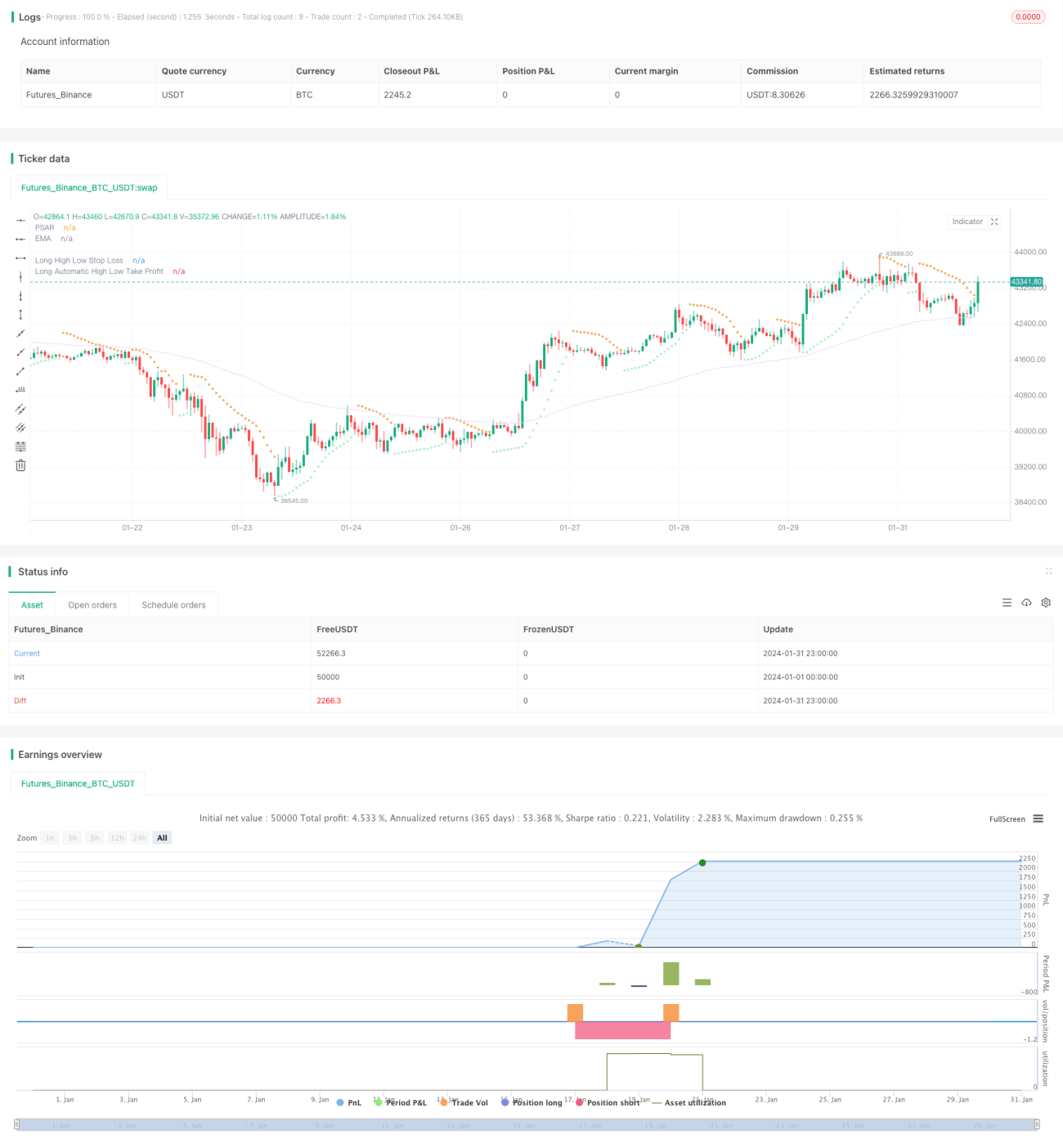

本戦略の目的は、異なるパラメータを設定することでトレーダーの心理と取引パフォーマンスのバランスをとり、より安定したリターンを得ることです。移動平均線、ボリンジャーバンド、ケルトナーチャネルなどの指標を用いて市場のトレンドとボラティリティを判断し、PSAR指標で反転シグナルを、TTMスクイーズ指標でモメンタムを判断します。取引シグナルはこれらの指標の組み合わせによって生成されます。同時に、高値・安値によるストップロスとリスクリワードによる利益確定でリスクを管理します。

戦略の原理

本戦略の主なロジックは以下の通りです。

-

トレンド判断:EMA(指数移動平均)線で価格のトレンド方向を判断。価格がEMAより上にあれば上昇トレンド、下にあれば下降トレンド。

-

反転判断:PSARで価格の反転ポイントを判断。PSARの点が価格より上にあれば強気シグナル、下にあれば弱気シグナル。

-

モメンタム判断:TTMスクイーズ指標で市場のボラティリティとモメンタムを判断。TTMスクイーズ指標はボリンジャーバンドとケルトナーチャネルの幅を比較してボラティリティを測定し、スクイーズ(収縮)は極端に低いボラティリティを示します。スクイーズの解除はボラティリティの増加と価格が大きな方向性を持って動き出すシグナルとなります。

-

取引シグナルの生成:価格がEMA線とPSAR点を上抜け、かつTTMスクイーズ指標がスクイーズを解除した場合に強気シグナル。価格がEMA線とPSAR点を下抜け、かつTTMスクイーズ指標がスクイーズに入った場合に弱気シグナル。

-

ストップロス方法:高値・安値ストップロスを採用。直近一定期間の最高値または最安値に設定倍率を乗じた値をストップロスポイントとする。

-

利益確定方法:リスクリワードレシオによる自動利益確定。ストップロスポイントから現在価格までの距離の比率に、設定したリスクリワードレシオパラメータを乗じて利益確定ポイントを算出。

パラメータ設定により、取引頻度、ポジション管理、ストップロス・利益確定ポイントを調整し、トレーダーの心理バランスをとることが可能です。

優位性分析

本戦略には以下の優位性があります。

-

複数指標による判断でシグナルの精度向上。

-

反転を主とし、順張りを従とすることで、反転ポイントを捉え、高値掴みや安値売りの確率を低減。

-

TTMSqueeze指標でトレンド中の調整局面を効果的に判断し、調整期の無駄な取引を回避。

-

高値・安値ストップロスはシンプルで実用的、市場に応じてストップロス距離を調整可能。

-

リスクリワードレシオによる利益確定は損益比率を数値化するため調整が容易。

-

各種パラメータ設定が柔軟で、個人のリスク選好に応じて微調整可能。

リスク分析

本戦略には以下のリスクも存在します。

-

複数指標の組み合わせ判断はシグナル精度を高める一方、エントリーポイントを逃す可能性が増える。

-

反転重視の戦略のため、トレンド相場ではパフォーマンスが低下する可能性がある。

-

高値・安値ストップロスは時に突破されることがあり、リスクを完全には回避できない。

-

リスクリワードレシオによる利益確定も、価格のギャップや調整により機能しない場合がある。

-

パラメータ設定が不適切だと、損失や頻繁なストップロスが発生する可能性がある。

最適化の方向性

本戦略は以下の点で最適化が可能です。

-

指標のウェイトを追加・調整し、シグナル精度を向上。

-

反転およびトレンド判断の指標パラメータを最適化し、獲得確率を向上。

-

高値・安値ストップロスのパラメータを最適化し、より合理的なストップロスを実現。

-

異なるリスクリワードレシオをテストし、最適な結果を得る。

-

ポジション数パラメータを調整し、1回の損失の影響を軽減。

まとめ

本戦略は総合的に見て、指標の組み合わせ判断とパラメータ調整により、トレーダーの心理を効果的にバランスさせ、安定した正のリターンを得ることができます。改善の余地はまだありますが、実運用に耐えうる価値を持っています。市場のフィードバックとパラメータの微調整を通じて、本戦略は取引心理をコントロールし、長期的に安定した利益を得るための有効なツールとなるでしょう。

- 1