ブレイクアウトプルバック取引戦略に基づく

概要

ブレイクアウト戻り売買戦略は、価格の絶対強度指標とMACD指標を計算することで、特定のトレンド下でのブレイクアウト後の戻り売買を実現する、短期売買戦略です。本戦略は複数の指標を組み合わせて大トレンド、中期トレンド、短期トレンドを判断し、トレンドが同じ方向で指標が補完し合うシグナルを確認することで、トレンドフォロー取引を行います。

戦略の原理

本戦略は主に価格の絶対強度指標とMACD指標に基づいて、ブレイクアウト後の戻り売買を実現します。まず、価格の9期間、21期間、50期間のEMAを計算し、大トレンドの方向を判断します。次に、価格の絶対強度指標を計算し、短期的な調整の強さを反映させます。最後にMACD指標を計算し、短期トレンドの方向を判断します。大トレンドが上昇傾向にあり、短期的に調整が発生した場合に買い、大トレンドが下降傾向にあり、短期的に反発が発生した場合に売ります。

具体的には、銘柄の大トレンドが上昇であるためには、9日EMAが21日EMAより高く、21日EMAが50日EMAより高い必要があります。短期調整の判断基準は、絶対強度指標の差が0未満、かつMACDDIFFが0未満であることです。銘柄の大トレンドが下降であるためには、9日EMAが21日EMAより低く、21日EMAが50日EMAより低い必要があります。短期反発の判断基準は、絶対強度指標の差が0超、かつMACDDIFFが0超であることです。

優位性分析

本戦略には以下のような優位性があります:

- 大トレンドと短期調整を組み合わせることで、偽のブレイクアウトを回避できる。

- 複数の指標を組み合わせて使用するため、信頼性が高い。

- 絶対強度指標が調整の強さを反映し、戻りの質を判断できる。

- MACDで短期トレンドや買われ過ぎ・売られ過ぎゾーンを判断できる。

リスク分析

本戦略には以下のようなリスクもあります:

- 大トレンドの判断を誤ると、取引が失敗する可能性がある。

- 戻りの時間や強さの判断を誤ると、無効な調整となる可能性がある。

- 極端な相場では指標が乖離し、誤ったシグナルが発生する可能性がある。

これらのリスクに対しては、パラメータを最適化して異なる期間の指標を判断する、ポジション保有ルールを調整して1回の損失を抑制する、より多くの指標でシグナルをフィルタリングして精度を高めるなどの方法で改善可能です。

最適化の方向性

本戦略は以下の点から最適化が可能です:

- より多くの指標の組み合わせをテストし、より適合した取引戦略を探す。

- 指標のパラメータを最適化し、指標の感度を高める。

- ストップロスの方法を調整し、1回の損失の最大値を低減する。

- フィルタリング条件を追加し、より効果的な領域でシグナルを発生させる。

- より多くの時間枠の指標を組み合わせて判断し、判断精度を高める。

まとめ

以上を総合すると、ブレイクアウト戻り売買戦略は全体的に安定した短期売買戦略です。大・中・小の複数トレンドを組み合わせて判断することで、レンジ相場での誤取引を回避します。また、指標の組み合わせ使用により判断の精度も高まっています。今後のテストと最適化を通じて、本戦略は長期保有に値する安定した戦略となり得ます。

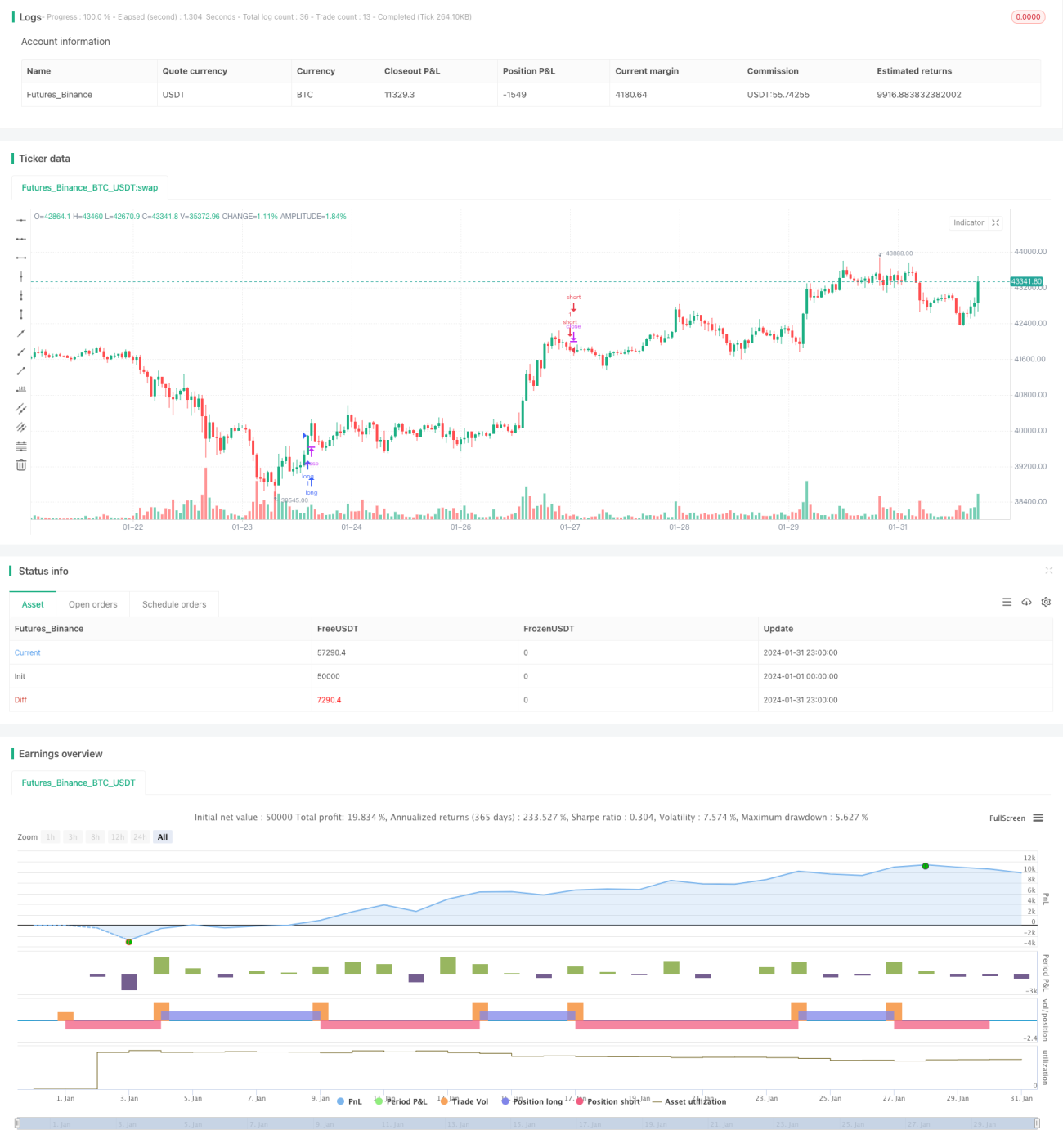

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Divergence Scalper [30MIN]", overlay=true , commission_value=0.04 )

message_long_entry = input("long entry message")

message_long_exit = input("long exit message") - 1