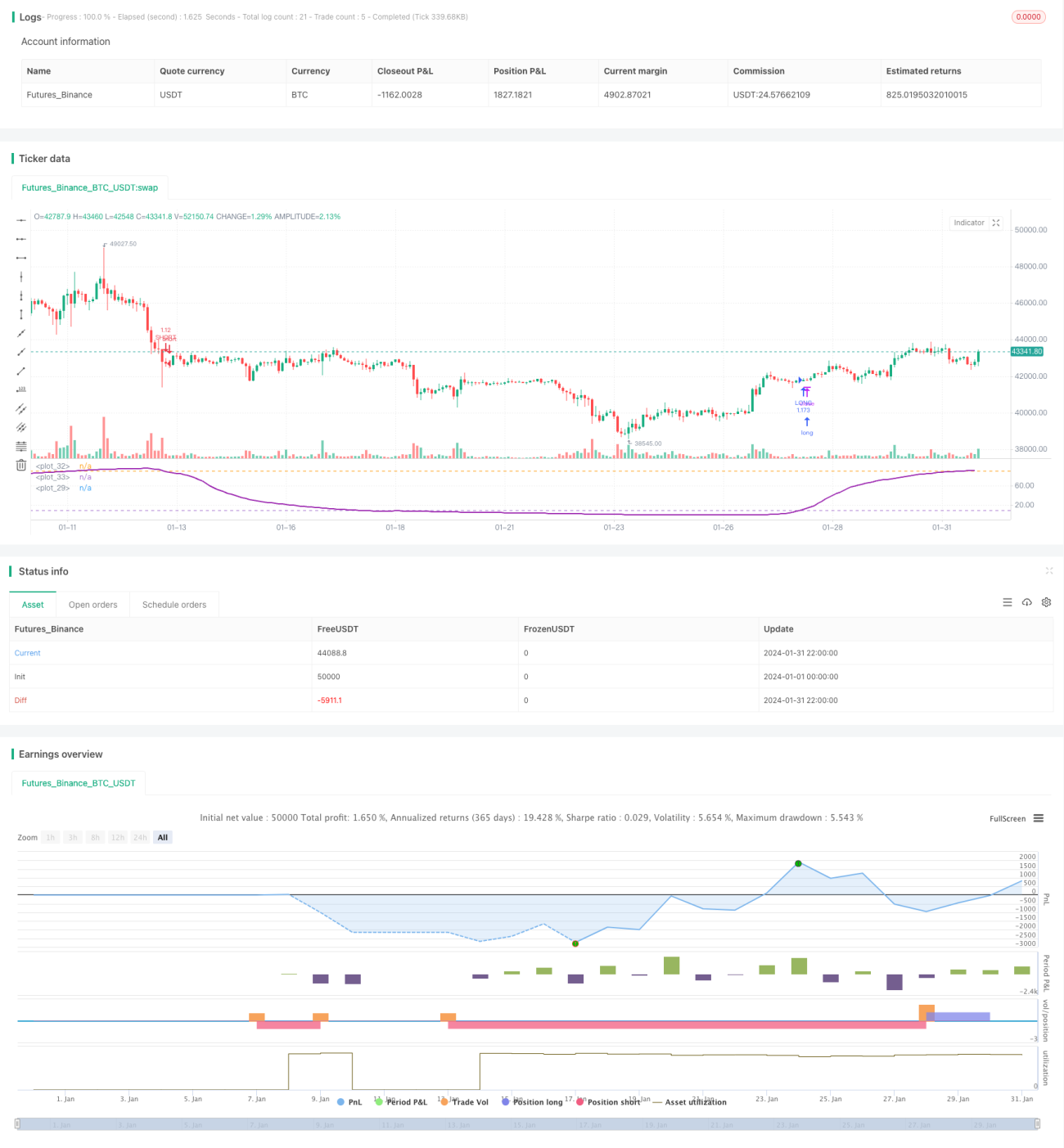

年内調整に基づくRSIオシレーター取引戦略

1

Follow

1802

Followers

概要

本戦略は、年内調整されたRSIオシレーター取引戦略です。RSI指標が設定された上限・下限ライン間で振動する特性を追跡し、RSIがラインにタッチした際に取引シグナルを発出します。

戦略原理

- MA移動平均線の長さ、RSIパラメータ、上限・下限ライン、利食い・損切りパラメータ、取引期間範囲を設定します。

- RSI指標値を計算します。RSI = (上昇平均値) / (上昇平均値 + 下落平均値) × 100

- RSI指標と上限・下限ラインを描画します。

- RSI指標が下限ラインを上抜けたら買いシグナル、上限ラインを下抜けたら売りシグナルです。

- ポジションを開き、OCO注文を設定します。

- 設定された利食い・損切りのロジックに従って損切りと利食いを行います。

戦略のメリット分析

- 年内の取引期間を設定することで、不適切な外部環境を回避できます。

- RSI指標は買われすぎ・売られすぎの状況を効果的に反映し、適切なレンジ内でオシレーター取引を行うことでノイズをある程度除去できます。

- OCO注文と利食い・損切りの設定を組み合わせることで、効率的なリスク管理が可能です。

戦略のリスク分析

- RSIの臨界値判断の正確性は保証できず、誤判定リスクが存在します。

- 年内の取引期間設定が不適切だと、より良い取引機会を逃したり、不適切な取引環境に入る可能性があります。

- 損切りラインが大きすぎると大きな損失が発生し、利食いラインが小さすぎると利益が小さくなる可能性があります。

RSIパラメータ、取引期間の時間範囲、利食い・損切り比率などを調整することで最適化できます。

戦略の最適化方向

- 異なる市場・異なる期間におけるRSIパラメータの最適値をテストする。

- 全体の相場周期の規則性を分析し、最適な年内取引期間を設定する。

- バックテストにより妥当な利食い・損切り比率を決定する。

- 取引銘柄の選択を最適化し、保有ポジション規模を拡大する。

- 他のより優れた取引手法や指標と組み合わせて最適化する。

まとめ

本戦略は、RSI指標が年内指定期間内で振動する特性を利用してトレンドフォロー取引を行い、取引リスクを効果的にコントロールします。パラメータ最適化とルール最適化により、より高い戦略効果を得ることができます。

Source

Pine

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title = "Bitlinc MARSI Study AST",shorttitle="Bitlinc MARSI Study AST",default_qty_type = strategy.percent_of_equity, default_qty_value = 100,commission_type=strategy.commission.percent,commission_value=0.1,initial_capital=1000,currency="USD",pyramiding=0, calc_on_order_fills=false)

// === General Inputs ===Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1