이중선 추적 알고리즘 거래 전략

개요

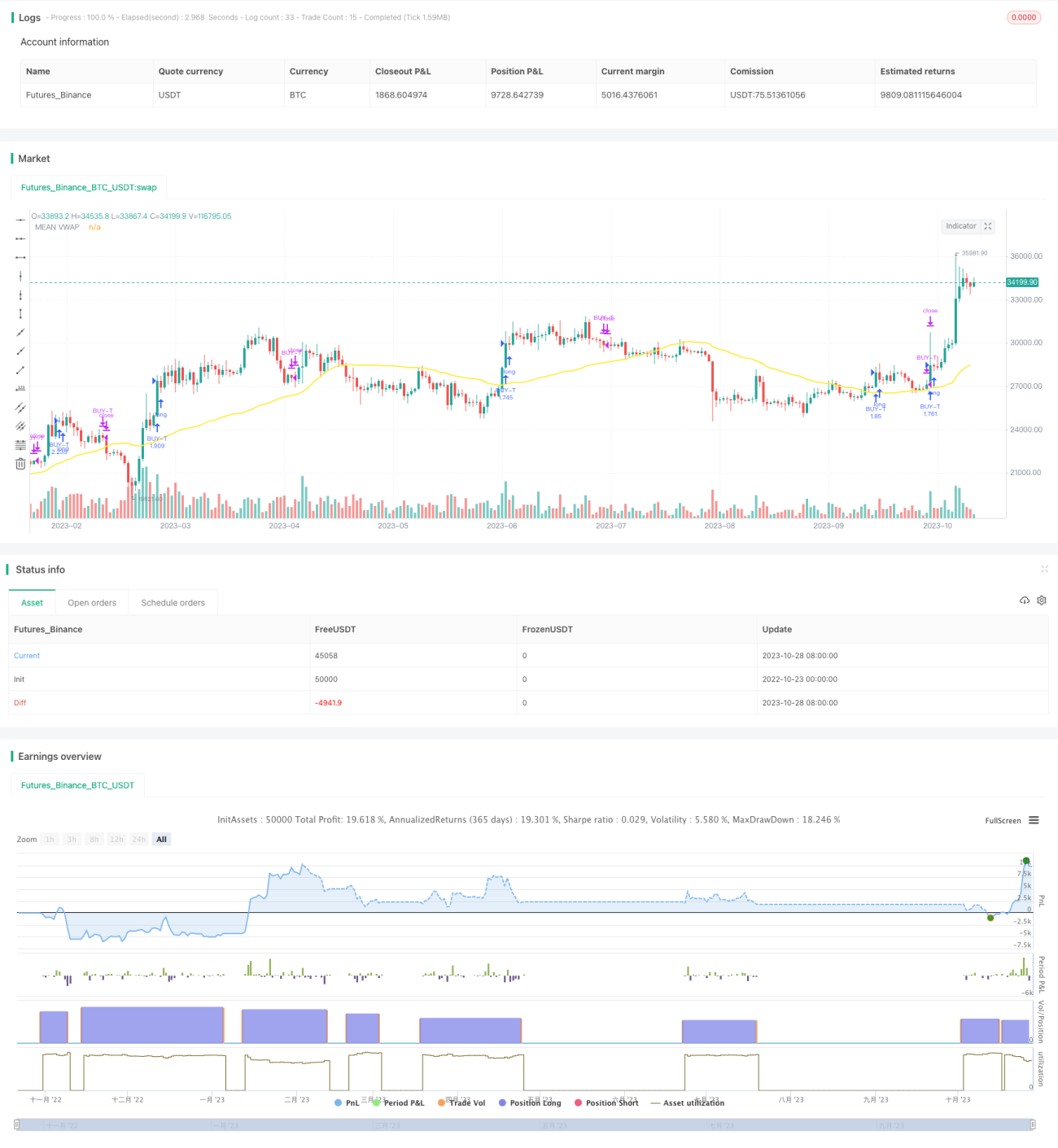

이 전략은 주로 이동평균선 교차 원리를 활용하고, RSI 지표의 반전 신호와 사용자 정의 이중선 추적 알고리즘을 결합하여 이동평균 교차 추적 거래를 수행합니다. 전략은 서로 다른 주기의 두 이동평균선 교차를 추적하며, 하나의 빠른 이동평균선은 단기 추세를, 다른 느린 이동평균선은 장기 추세를 추적합니다. 빠른 이동평균선이 느린 이동평균선을 위로 돌파하면 단기 추세가 상승했음을 의미하여 매수할 수 있고, 빠른 이동평균선이 느린 이동평균선을 아래로 돌파하면 단기 추세가 종료되었음을 의미하여 포지션을 청산해야 합니다.

전략 원리

-

서로 다른 매개변수를 가진 두 그룹의 VWAP 이동평균선을 계산하여 각각 장기 추세와 단기 추세를 나타냅니다.

- 느린 천장선과 기준선은 장기 추세를 계산합니다.

- 빠른 천장선과 기준선은 단기 추세를 계산합니다.

-

두 그룹의 천장선과 기준선의 평균값을 각각 느린 이동평균선과 빠른 이동평균선으로 사용합니다.

-

볼린저 밴드 지표를 계산하여 횡보 및 돌파를 판단합니다.

- 중간선은 빠른 이동평균선과 느린 이동평균선의 평균입니다.

- 볼린저 밴드 상하단은 돌파 판단에 사용됩니다.

-

TSV 지표를 계산하여 거래량 에너지를 판단합니다.

- TSV가 0보다 크면 상승력이 하락력보다 크다는 것을 의미합니다.

- TSV가 해당 EMA보다 크면 힘이 강화되었음을 의미합니다.

-

RSI 지표를 계산하여 과매수/과매도를 판단합니다.

- RSI가 30 미만이면 과매도 구간으로 매수 가능합니다.

- RSI가 70 초과이면 과매수 구간으로 매도해야 합니다.

-

진입 조건:

- 빠른 이동평균선이 느린 이동평균선을 상향 돌파

- 종가가 볼린저 밴드 상단을 상향 돌파

- TSV가 0보다 크고 해당 EMA보다 큼

- RSI가 30 미만

-

청산 조건:

- 빠른 이동평균선이 느린 이동평균선을 하향 돌파

- RSI가 70 초과

장점 분석

-

이중 이동평균선 시스템을 사용하여 장단기 추세를 동시에 포착할 수 있습니다.

-

RSI 지표는 과매수 지역에서 매수하고 과매도 지역에서 매도하는 것을 방지합니다.

-

TSV 지표는 추세를 뒷받침할 충분한 거래량을 보장합니다.

-

볼린저 밴드를 활용하여 주요 돌파 지점을 판단합니다.

-

다양한 지표 조합으로 가짜 돌파를 효과적으로 걸러낼 수 있습니다.

위험 분석

-

이동평균선 시스템은 잘못된 신호를 생성하기 쉬우므로 보조 지표로 필터링해야 합니다.

-

RSI 지표 매개변수를 최적화해야 하며, 그렇지 않으면 매매 시점을 놓칠 수 있습니다.

-

TSV 지표도 매개변수에 민감하므로 신중한 테스트가 필요합니다.

-

볼린저 밴드 상단 돌파는 가짜 돌파일 가능성이 있으므로 확인이 필요합니다.

-

여러 지표 조합으로 인해 매개변수 최적화가 어렵고 과최적화되기 쉽습니다.

-

훈련 및 테스트 데이터가 불충분하면 곡선 맞춤이 발생할 수 있습니다.

최적화 방향

-

더 많은 주기 매개변수를 테스트하여 최적의 매개변수 조합을 찾습니다.

-

MACD, KD와 같은 다른 지표를 시도하거나 RSI와 결합합니다.

-

매개변수 최적화는 워크 포워드 분석을 충분히 활용해야 합니다.

-

손절매 전략을 추가하여 개별 손실을 통제합니다.

-

머신러닝 모델을 추가하여 신호 판단을 보조하는 것을 고려합니다.

-

시장별로 매개변수를 조정하고 단일 매개변수 조합에 과도하게 의존하지 않습니다.

요약

본 전략은 이중 이동평균선 시스템을 통해 장단기 추세를 포착하고, 동시에 RSI, TSV, 볼린저 밴드 등 다양한 지표로 신호를 필터링합니다. 전략의 장점은 추세에 따라 거래하여 장기 상승 흐름을 포착할 수 있다는 점입니다. 하지만 일부 가짜 신호 위험이 존재하므로 매개변수를 추가로 최적화하고 손절매를 통해 위험을 낮춰야 합니다. 전반적으로 이 전략은 추세 추종과 반전 지표를 결합하여 장기 상승장에서 효과적이지만, 시장별로 getParameter 조정이 필요합니다.

- 1