내부 상승률 손절 기반 롱숏 모멘텀 돌파 전략

개요

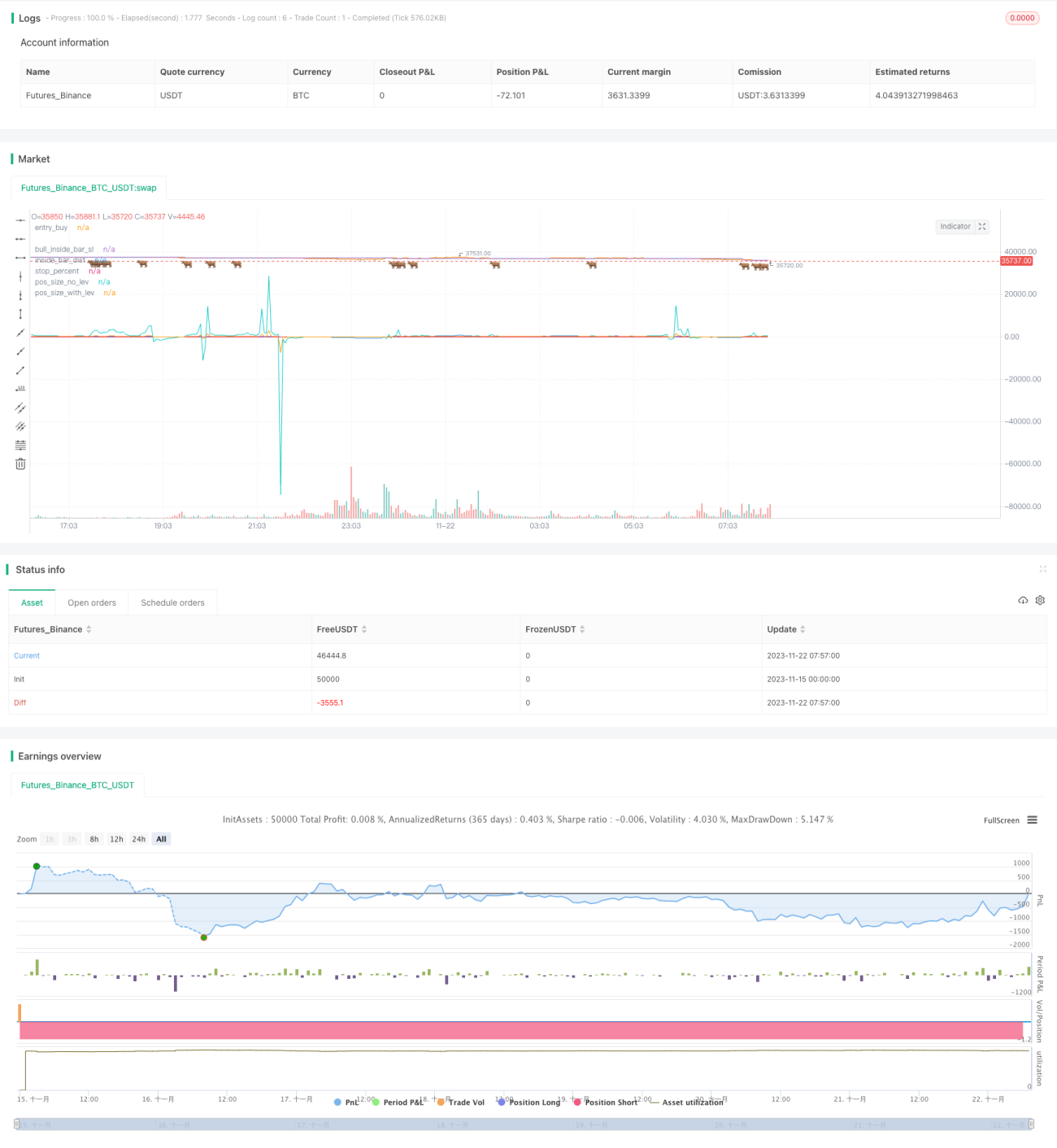

해당 전략은 비정상적인 상승폭을 보이는 캔들을 식별하여 현재 시장에 돌발적인 단방향 흐름이 존재하는지 판단합니다. 비정상적인 상승폭 캔들이 감지되면 해당 캔들의 고점 부근에 매수 지정가 주문을 설정하고, 이전 캔들의 저점 부근에 손절매 주문을 설정하여 높은 레버리지 리스크 관리의 롱 포지션을 형성합니다. 전략은 손절매 라인을 실시간으로 모니터링하며, 가격이 손절매 라인을 하향 돌파하면 즉시 주문을 취소하고 손절매를 실행합니다.

전략 원리

이 전략은 주로 비정상적인 상승폭 캔들의 형성을 판단합니다. close > open이고 high < high[1]이며 low > low[1]인 캔들이 발생하면 현재 주기에 비정상적인 상승 흐름이 있다고 간주합니다. 이때 롱 포지션 진입 신호가 설정되며, 진입 가격은 현재 캔들의 최고가 부근입니다. 동시에 손절매 가격은 이전 캔들의 최저가 부근으로 설정되어 높은 레버리지 리스크 관리 모드를 형성합니다. 가격이 손절매 라인을 돌파하는 상황을 지속적으로 모니터링하여 리스크를 관리합니다.

장점 분석

이 전략의 가장 큰 장점은 시장의 단기적인 비정상적인 급등 흐름을 포착하여 초고빈도 매매를 구현할 수 있다는 점입니다. 또한 비교적 넓은 손절매 폭을 설정함으로써 높은 레버리지를 사용한 리스크 관리 거래가 가능하여 더 큰 수익을 얻을 수 있습니다. 추가로 전략은 손절매 라인을 자동으로 모니터링하여 가격이 손절매 라인을 하향 돌파할 때 신속하게 손절매를 실행함으로써 거래 리스크를 효과적으로 통제합니다.

리스크 분석

이 전략의 주요 리스크는 비정상적인 상승폭 판단의 정확성이 낮아 시장의 급등 흐름을 효과적으로 포착하지 못할 경우 거래 신호 오류 가능성이 높아진다는 점입니다. 또한 손절매 위치 설정도 거래 리스크와 수익에 큰 영향을 미칩니다. 손절매가 너무 느슨하면 거래 손실 위험이 커지고, 너무 좁으면 시장 흐름을 효과적으로 따라잡아 수익을 내기 어려울 수 있습니다. 많은 백테스트를 통해 손절매 위치를 최적화해야 합니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

-

비정상적인 상승폭 판단 기준에 더 많은 지표나 딥러닝 모델을 도입하여 보조 판단함으로써 전략 신호 판단의 정확성을 높일 수 있습니다.

-

손절매 위치 설정에 대해 대규모 통계 및 최적화 분석을 수행하여 거래 리스크와 수익 수준을 균형 있게 조정하는 더 나은 손절매 위치를 찾을 수 있습니다.

-

거래량 필터, 구간 돌파 검증 등 더 많은 고빈도 거래 리스크 관리 메커니즘을 도입하여 갇힐 확률을 줄일 수 있습니다.

-

전략 진입 기준을 조정할 수 있습니다. 반드시 비정상적인 상승폭 캔들에 국한되지 않고, 더 많은 지표와 모델을 결합하여 판단함으로써 다중 검증 메커니즘을 형성할 수 있습니다.

요약

이 전략은 전반적으로 전형적인 고빈도 거래 전략으로, 단기 돌파형 전략에 속합니다. 시장의 돌발적인 비정상 변동을 포착하여 초고빈도 매매를 실현합니다. 동시에 손절매 리스크 관리와 높은 레버리지 메커니즘을 사용하여 리스크를 통제합니다. 이 전략은 최적화 여지가 크며, 여러 각도에서 조정 및 최적화가 가능합니다. 최종 목표는 리스크를 통제하는 전제 하에 더 높은 초고빈도 거래 수익을 얻는 것입니다.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 08:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// LOVE JOY PEACE PATIENCE KINDNESS GOODNESS FAITHFULNESS GENTLENESS SELF-CONTROL

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JoshuaMcGowan

// I needed to test/verify the functionality for canceling an open limit order in a strategy and also work thru the pieces needed to set the position sizing so each loss is a set amount. - 1